On September 24, 2021, ISDA submitted a response to HM Treasury on the Wholesale Markets Review (WMR).

The WMR is a welcome opportunity to tailor the UK’s revised Markets in Financial Instruments Directive (MIFID II)/Markets in Financial Instruments Regulation (MIFIR) framework to the UK market, and ISDA members support a large majority of the proposals.

However, ISDA has proposed several key changes, including recalibrating the transparency regime for derivatives markets, with the aim of achieving greater, more meaningful transparency in the UK.

ISDA welcomes HM Treasury’s proposals that all post-trade risk reduction services should be exempt from the derivatives trading obligation and the scope of the derivatives trading obligation and clearing obligation should be realigned. ISDA also welcomes HM Treasury’s proposals to simplify and improve the systematic internalizer regime.

Source: ISDA

UK Finance

While capital markets may seem a distant, remote concept, they play a central role in the functioning of the UK economy and are central to our lives. Capital markets facilitate the connection between those who have and those who need capital, which in turn leads to investment and the creation of jobs and growth. They contribute to the diversity of funding and financing options alongside traditional bank lending which helps manage economic risk.

UK Finance welcomes the HM Treasury Wholesale Markets Review and you can read our response here. This Review presents an opportunity to contribute to an innovative, sustainable and technologically driven marketplace. It also provides the industry with an opportunity to tailor the UK’s regime to its unique characteristics and supports our wider aims of a proportionate rulebook, competitiveness and market efficiency.

The Wholesale Markets Review itself primarily focuses on changes that sit within the UK’s recently onshored MiFID/R regime. It therefore also presents an opportune moment to recalibrate post-Brexit and make targeted changes, where perhaps MiFID II did not in practice achieve the policy objectives it sought to attain.Some of the key changes we recommend include:

1 – Preserving a choice of trading and execution structures to contribute to maintaining deep and liquid capital markets. Competition plays an essential role in fostering innovation, ensuring competitive pricing and ultimately providing the best choices and outcomes to end investors and markets. A diverse market structure is the backbone of healthy, resilient and competitive financial markets.

2 – Welcoming HM Treasury’s proposals to remove the Share Trading Obligation and the Double Volume Cap. These changes would reduce market structure complexity and help to ensure that the best outcome is delivered for investors.

3 – Recalibrating the transparency regime for fixed income and derivatives markets, recognising that not all asset classes operate in the same way. The right transparency rules should be applied to the right products, based on the liquidity and risk profile, helping to deliver a proportionate regime.

However, given the credentials of the UK’s capital markets, its diversity of trading modalities and depth of liquidity, we are starting from a position of strength.

One which we hope with the right policy changes via the Wholesale Markets Review and future government and regulatory consultations, will help to enhance the UK’s capital markets offering, maintaining its position as a global financial hub.

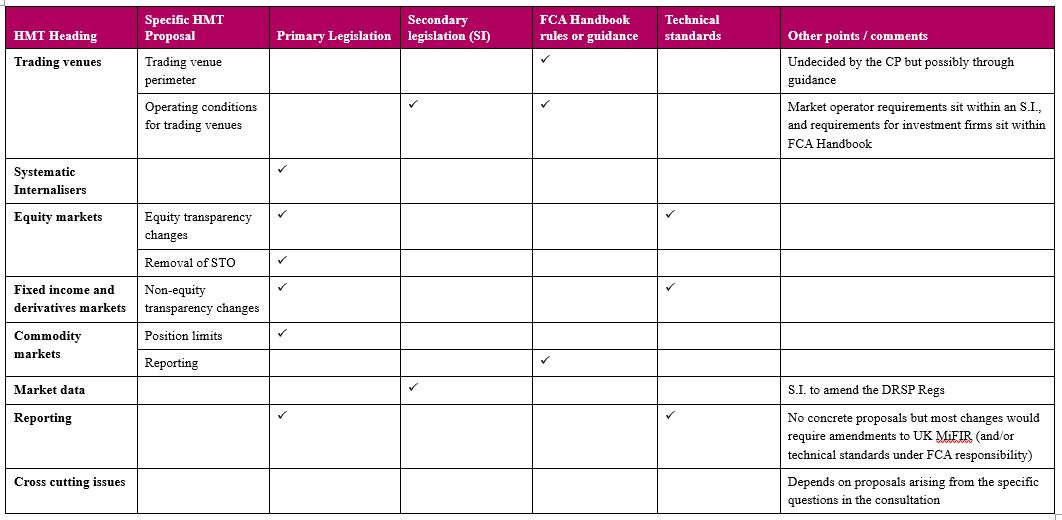

As our members begin to work through the swathe of expected changes, we are mindful of the fact that there will be changes to both primary legislation as well as secondary regulatory guidance. As such, we hope the table below will provide useful guidance in helping members to navigate the complexity of change.

It’s an exciting time for UK capital markets as we continue to engage our members to support the evolution of a dynamic and effective UK capital markets regime. For more information on UK Finance’s work in this space, please contact ayesha.ghafoor@ukfinance.org.uk

The table below provides a high-level indication of whether HM Treasury’s proposals in the Wholesale Markets Review (to the extent pursued following the consultation) are likely to be made through legislative amendments, amendments to rules/guidance in the Financial Conduct Authority (FCA) Handbook or via technical standards now within the FCA’s remit.

Source: UK Finance

ICMA

ICMA has now published its response to the HM Treasury Wholesale Markets Review Consultation Paper. The response was drafted primarily by ICMA’s MiFID II transparency taskforce but a few responses also take into account the views of ICMA’s other working groups and committees, such as repo and primary markets.

The ICMA MiFID II transparency taskforce member response is based on consensus view from a varied group of buy- side and sell-side investment firm bond trading participants, representing EU 27 countries, the UK and the US. There is a unique value in conveying a broad view from across buy-side and sell-side communities and we hope this response is informative and useful. Taskforce members welcome the efforts of HMT to seek out stakeholder views concerning a review of wholesale markets. However, this response is related solely to cash bonds.

Source: ICMA

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Related articles

-

The agreement will establish an ongoing forum to discuss voluntary regulatory cooperation.

-

The Amsterdam-based clearing house is the first non-UK CCP to achieve permanent recognition.

-

Review of trading desks found that incoming banks did not yet retain full control of their balance sheets.

-

UK has a greater market share than pre-Brexit for on-venue execution of GBP interest rate swaps.

-

Recognition has been temporarily extended until 30 June 2025.