Electronic Portfolio Trading Rewrites the Corporate Bond Liquidity Playbook

By Ted Husveth, Director, Credit Product Manager, Tradeweb

Ted Husveth, Tradeweb

Tradeweb was the first trading platform to offer portfolio trading for corporate bonds, launching in early 2019. The platform facilitated a total $43 billion of portfolio trades in 2019, with single trades as large as $1bn in notional value.

While major swaths of the fixed income marketplace, such as government bonds, mortgage-backed securities and interest rate swaps have increasingly moved to electronic marketplaces, the corporate bond market has been a little slower to make the transition, particularly for the largest trades. This is changing though, with the introduction of electronic portfolio trading capabilities for corporate bonds.

Efficiency Gains

Suddenly, the ability to package multiple bonds into a single basket of buys and sells, negotiate a portfolio level price, and execute the trade in a single electronic transaction, makes the allure of electronic workflows too hard to ignore. Previously, market participants exchanging baskets of multiple bonds would assemble spreadsheets of bonds and prices, which were then emailed backward and forth to liquidity providers. It was a painstaking process of iteration that can take more than a day to complete.

Electronic portfolio trading advances this process, by integrating powerful electronic tools with a common interface. On top of that, traders can use Ai-Price, real-time reference pricing from Tradeweb, to inform where each bond – and the basket itself should price; use net-spotting to reduce hedging costs after execution; and iterate with their liquidity provider on price through a seamless, instant interface, which removes the need to email spreadsheets back and forth.

The Rise of the ETF

Another factor setting the stage for widespread adoption of electronic portfolio trading is the growth of the ETF. Credit ETFs now account for more than $214 billion in assets under management.* As a result, the create-redeem process – in which baskets of cash bonds are exchanged for ETF shares – is now a significant contributor to trading activity in the underlying cash credit market.

This has prompted a change behavior from liquidity providers, including algorithmic market makers have emerged, now geared up to support ETF ecosystems. In each instance, these liquidity providers are capable of pricing trades for baskets, rather than individual line items.

This creates a perfect storm of liquidity, participants, and pricing power, which can be harnessed for the benefit of institutional investors more broadly as a new liquidity outlet.

Portfolio Trading in the Real World

The first and most obvious real-world benefit of portfolio trading is efficiency. Electronically executing a portfolio trade removes several layers of manual busywork from the trading workflow compared to list trading where each individual CUSIP is looked at one by one, the right counterparty is sought for each and in many cases are manually traded over the phone.

But there also more subtle advantages. For one, Tradeweb’s portfolio trading functionality allows institutional clients to submit a portfolio trade to multiple liquidity providers simultaneously, or to a single liquidity provider. By controlling the number of counterparties exposed to the trade, market participants are able to balance the potential for price improvement against the risk of disclosing potentially market-moving information to multiple parties.

Another benefit of the portfolio trading approach is the ability to spread risk by packaging illiquid bonds alongside highly liquid securities in a single portfolio.

- Specific trading scenarios in which these advantages come into play include the following: Large outflow in a fund(s), must raise a certain amount of cash quickly

- Large inflow in a fund(s), must buy a certain amount of bonds quickly

- Portfolio Manager/Research Analyst has specific views on tickers/sectors that has created a list of buys and/or sells

- Transition Management agenda (ie. Selling IG and buying HY)

- Large portfolio including illiquid bonds are being asked to sell or buy

The Impact of Portfolio Trading

As demonstrated by the growing volume of portfolio trading, it is clearly growing in its importance to institutional investors. We see there being two long-term impacts on the marketplace in terms of risk transfer and illiquid bonds.

Risk transfer: Portfolio trades are exchanged on the basis of a single price for the basket, regardless of the size of that basket or the line items it includes. In that respect, a participant is deciding less on prices for each underlying CUSIP, and more the consolidated risk. A market more acclimated to, and more robust for, risk transfer is an important development for investment grade and high yield markets.

Illiquid securities: As more and more participants exchange on the basis of risk, and therefore broaden their horizons on what to buy and sell, so prices are established for less liquid securities that might not have normally been executed in an all-to-all market. By establishing a more regular pattern of prices for certain illiquid securities, so it becomes obviously easier to understand where those securities may trade again. In time, it is feasible that portfolio trading may help to ameliorate price formation in thinly traded securities, and so expand the investible universe of corporate bond securities.

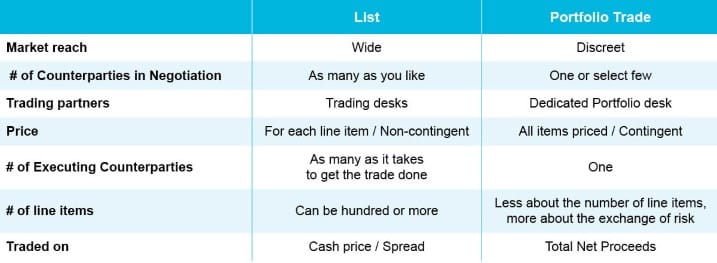

How Does Portfolio Trading Differ from List Trading?

Portfolio trading is often confused with list trading. A common misconception about portfolio trading is that its simply large, multi-line item trades and lists are just significantly smaller. That’s not really the case. At Tradeweb, we have seen portfolios trade with fewer than 10 lines and more than 300. The concrete difference between the two is the “all at once” execution with one dealer that defines portfolio trading. It’s the way the transaction is structured and the specific benefits a trader desires around exchanging risk that determines which protocol to use. Following is a quick break-out of key differences between a list trade and a portfolio trade.

*Bloomberg

*BloombergLearn more about our Portfolio Trading offering here.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Related articles

-

Collaboration aims to empower traders to anticipate market trends and mitigate credit risk.

-

The more stressed the market, the less information anyone wants to give away.

-

Technology, Street relationships can differentiate a product offering in a fast-growing space.

-

LTX focuses on innovating electronic trading for the benefit of the credit market.

-

Bond traders are adjusting to what could become the new volatile normal.