On July 10, STA held an Open Call on FINRA’s surveillance priorities that now include patterns of activity across two related products, typically a stock and its option derivative. Gene DeMaio, SVP of FINRA Market Regulation presented and described scenarios of “mini-manipulation” which broadly speaking, are situations whereby the underlying price of an equity security is manipulated to affect the price of a corresponding listed option on that equity security to either put on or take off a position at advantageous prices.

In this issue of Lighthouse, we highlight some of FINRA’s capabilities in carrying out this critical function and what firms should be thinking about from a compliance perspective.

To help us do that, we enlisted the help of Trillium’s Chief Compliance Officer Michael Friedman to share his thoughts on FINRA’s cross product surveillance capabilities and how firms should be setting themselves up to detect cross product manipulation.

Cross-Product Surveillance

As discussed on the call, FINRA’s cross product surveillances are focused on two areas: (a) mini-manipulation, where a trader aggressively trades a stock in order to obtain a more favorable option price, and (b) anticipatory hedging, where a broker attempts to hedge a customer order by trading in a different but related product that nonetheless influences the price of the customer’s trade. Mini-manipulation had actually been flagged by regulators as long ago as the SEC’s 1978 Special Study of the Options Markets, but actual violations had been few and far between until FINRA recently expanded its surveillance parameters.

FINRA had previously only looked for aggressive stock trading when an option position had already been established; however, updated surveillance now also looks for traders entering into option positions after their aggressive trading in the underlying equity. This pattern is the subject of some cases that are now public (pending SEC and FINRA enforcement actions against Lek Securities, and Cboe’s 2014 enforcement action against HAP Trading).

FINRA also reviews other variants of mini-manipulation, including mini-manipulation with spoofing or layering of the option, where the trader attempts to improve his option price beyond its already-improved level by also entering bids or offers on the opposite side of his option trade, and equity layering option trading, where the trader uses aggressive unfilled orders (not actual trades) in the underlying to obtain a favorable price in the option.

FINRA’s cross product surveillance also includes anticipatory hedging. This surveillance began with a customer complaint that a broker was negatively impacting the customer’s execution price by trading ahead of the customer not in the instrument the customer ordered but in an economically correlated instrument. It is important to note that instruments must be directly correlated, like SPX and SPY, not merely related or in the same industry. While the harm of this type of behavior is usually framed in terms of an injury to the broker’s customer, there are also problematic scenarios where market makers are harmed.

Finally, alerts on mini-manipulation are often found in high volume products during times of day when there is less trading activity. The occurrence of manipulation in high volume, or liquid securities is somewhat of a new phenomenon. But when you think about how the popularity of passive investing has shifted the percentage of overall trading volumes occurring at the close, it is reasonable to believe that the prices of large cap securities can be manipulated intra-day. Coupled with the fact that the options market is highly competitive and electronically quote driven off the prices of the underlying security you can understand how these two markets collide at times. Firms should not assume that high volume products cannot be manipulated.

Cross-Product Detection Platforms

Some trade surveillance platforms have added cross product detection into their offerings. To avoid the pitfall that limited FINRA’s detection of these events, Friedman recommends that firms not limit their inquiry by whether the trader is exiting or entering his option position; all that matters is that a single option trade is priced more favorably than where it was priced prior to the trader’s aggressive activity in the underlying. To test for this, a surveillance platform cannot simply analyze order logs; market data must also be supplied to the detection engine.

Trillium added cross product detection to its Surveyor trade surveillance platform shortly after the Lek cases were filed in March 2017. SEC and FINRA included unusually granular details of the cross product manipulation at issue in their complaints, and this served as a guide for Trillium’s design team.

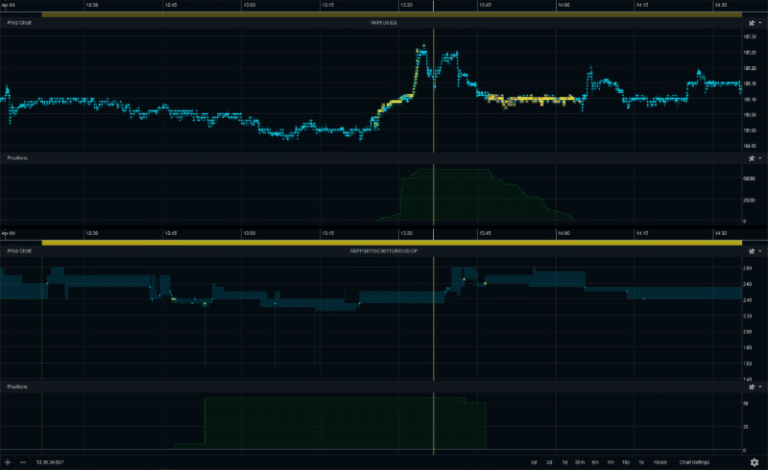

To assist reviewers in analyzing cross product alerts, Trillium devised a split-screen market viewer with a horizontal split, so that time scaling can be maintained in both instruments simultaneously. This enables reviewers to clearly see how trading in a stock can lead to improved pricing in an option. In the example below, the vertical yellow stripe links time in the stock chart (above) with the option chart (below), so it is clear that the account exited its call option position after having first driven prices higher by aggressively buying the underlying.

Conclusion

Given how technology has enabled capital and trading to efficiently flow across the options, equities and futures markets, cross product surveillance is important to the overall integrity of our markets. Manipulation, mini or otherwise, if left unchecked leads to fewer providers of liquidity and undermines investor confidence. Firms should be aware that our industry’s regulators understand this, and are developing the means and ability to identify and weed it out.

About Michael Friedman

Michael Friedman supervises Trillium’s regulatory compliance, and designs Trillium’s compliance technology. Michael received a BA cum laude from Princeton University and a JD from Northwestern University.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Related articles

-

Aim is to develop a complete, accurate, timely and cost-effective transaction reporting mechanism.

-

The European Union will implement Unique Product Identifier reporting effective April 29.

-

There are a large number of legal petitions for review of the final rules.

-

FX is the biggest concern for the buy side when the US shortens its settlement cycle.

-

The UK Accelerated Settlement Taskforce has set a target date of 2027.