(The following article first appeared in the 2Q issue of GlobalTrading.)

Behind the Curb: A Closer Look at Trading Curbs in Asia Markets

By Keith Lau, Director, Head of APAC Systematic Client Coverage, AES, Credit Suisse

Keith Lau, Credit Suisse AES

In March 2020, investors grappled with a volatile market rout on the back of the COVID-19 outbreak and oil price wars. The most striking sign of investor fright was witnessed in the market “fear gauge” – VIX, which registered as high as 80, a level not visited since the Global Financial Crisis (GFC) in 2008.

In the wake of such moves, trading rooms and Bloomberg chat rooms were lit red over several days with notices of “Circuit Breakers” – temporary market halts that allow investors to rationalize orders, reassess market conditions and adjust trading decisions until the market resumes again. In some markets, blue chip stocks were pegged at “limit down” for days.

The diverse markets in Asia all have different ways of tackling the shared goal of “maintaining a fair and orderly market,” which poses unique challenges for traders with different objectives. In this article, I will briefly discuss the myriad forms of trading curbs in Asia, and both their intended, and unintended consequences.

SINGLE STOCK LIMIT UP / DOWN LEVELS, AND THE MAGNET EFFECT

In Asia, some of the major stock exchanges employ price limit up and limit down levels for single stocks. For example,Taiwan has a 10% up/down price band versus previous closing price for all listed stocks.

Whilst on face value, forcing stocks to trade inside a 10% band would appear as a palpable measure to limit volatility, the sheer presence of the looming price limit also alters trader behavior in a way that may be counterproductive to its intended objective. Some call this the “magnet effect”, where mounting selling pressure (in a bear market) and negative sentiment may accelerate investors to “flee before the window closes,” therefore becoming self-fulfilling in its nature. To make matters worse, once a stock hits limit down, anyone who is working a sell order may be left with the apprehension of uncertainty in the fulfillment of execution for the day. If the displayed selling pressure continues to mount on the order book, it serves to further drive fear and panic, which may continue to peg the stock at limit down on the next day.

VCM – THE BEST ANSWER TO SINGLE STOCK TRADING CURBS?

The Volatility Control Mechanism, or VCM in short, was introduced in 2016 by the Stock Exchange of Hong Kong (SEHK) with the aim to appease all investors by providing a trading curb with the best compromise: it is not a trading halt, it is not a suspension, and it is not a static price limit – all of which are typically measures cited as disruptive trading curbs. The VCM (in its introductory configuration) works by at looking at a variable reference price (defined as the Last Trade price 5 minutes ago), and if the stock trades at a level 10% away from this reference price, the market will transition into a 5-minute “cooling period”,during which trading continues but is confined to a 10% price band from the reference price.The market resumes back to normal after the cooling period, allowing market forces to continue to dictate price discovery.

The VCM partially solves the problem of the “magnet effect”by referencing a variable price limit instead of a static price limit, and also, because the continuity of trading is preserved during the cooling period, the mechanism allows investors a degree of freedom to liquidate positions in a volatile market. It is interesting to note that, ever since the initial launch of the VCM in 2016, it has never been triggered (as of the time of writing). On May 11th 2020, an enhancement to the HKEX VCM was implemented to cover a wider universe of stocks, and also to apply a tiered structure on the trigger thresholds.

MARKET-WIDE CIRCUIT BREAKERS

Like the New York Stock Exchange (NYSE)’s circuit breaker that is tied to the S&P 500’s moves on the day, various Asia markets have implemented similar curbs based on staggered trigger levels that result in trading halts. Inmost implementations of the circuit breaker, investors were able to continue trading after a short pre-open style auction where price discovery resumes and volumes print on the tape.

However, the benefits of the circuit breakers may be eclipsed if the price thresholds are set too tight, where the accelerative effect of these limits could compound to produce unintended and undesirable consequences. An example can be seen on the introduction of the market-wide circuit breaker in China in 2016: the exchange tripped through two circuit breaker levels, 5% and 7%, and finally induced a full-day trading halt, bringing a close to the shortest trading day in history clocked at just 29 minutes.

DO TRADING CURBS LIMIT VOLATILITY?

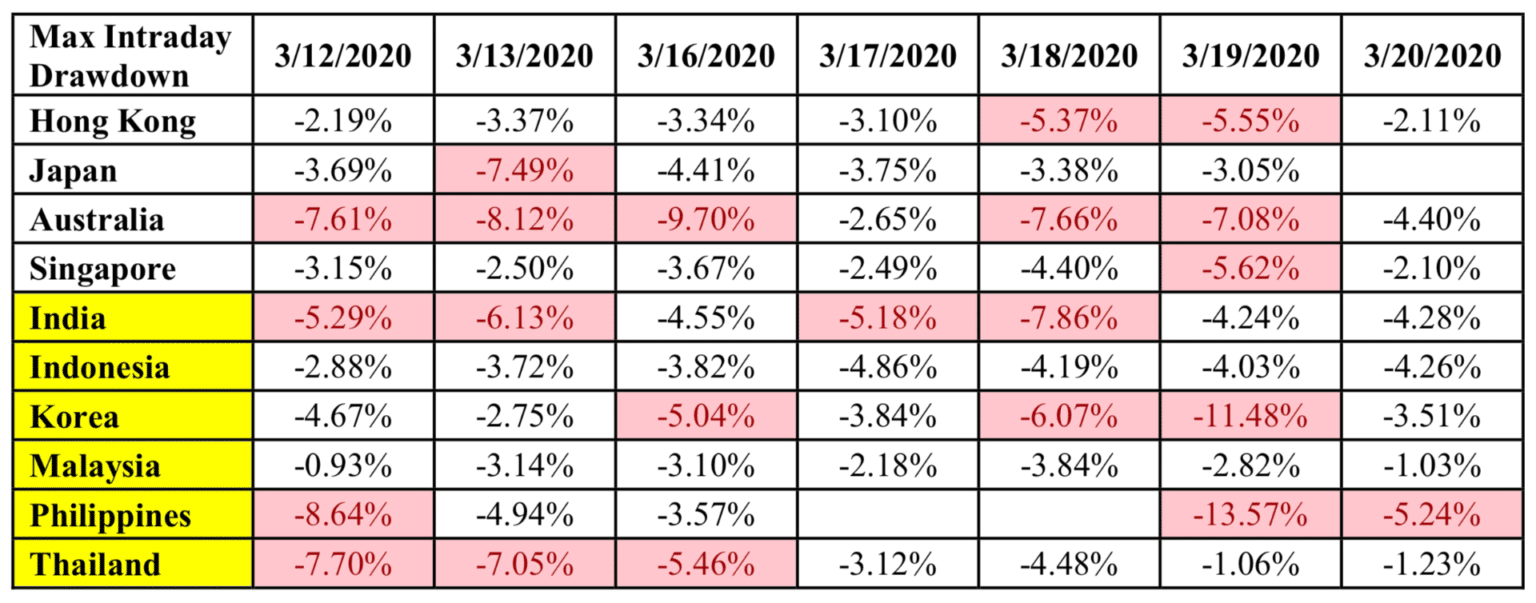

Although this is not the intended function of trading curbs, for the average investor, it would be tempting to draw on the belief that their assets would be more insulated from negative price moves if trading curbs were present. Taking a look at the maximum intraday drawdown of Asia markets during the most tumultuous weeks of March, we see that markets with market-wide circuit breakers (in yellow) do not exhibit significantly fewer drawdowns than those without (Hong Kong, Japan, Australia,and Singapore). Although we should not assume that these markets are perfectly correlated,the variance in outcomes does not appear to be significant.

Therefore, it is important to understand the true spirit of price-based trading curbs: it is meant to solve for problems caused by erroneous trading, and/or to facilitate genuine price discovery by providing a ‘time-out’ to pause, evaluate, inhibit panic, and publicize order imbalances. What it does not aim to solve for, is to reduce “volatility” – which may be a misnomer for some.

SHORT SELL BANS –FRIEND OR FOE?

A number of exchanges across Asia have adopted Short Sell bans – either by restricting these orders outright (Korea, Malaysia,and Indonesia), tightening uptick rules (Thailand and Taiwan market), or by limiting outstanding short interest (Taiwan). Short sellers have, at times, been identified as the culprits for market moves on the downside. However, several empirical studies have shown the contrary, as short selling activity paves the preconditions for market makers and stat-arb funds to continue the provision of liquidity, absorb shocks and price dislocations, and maintain the facilitation of effective price discovery. One of the papers published by Helmes, Henker and Henker (2011) addressed the question. Titled “How the Australian ban on short selling during the GFC affected market quality and volatility”, the empirical evidence shown in the study highlighted the effects of the Short Sell Ban as follows:

1. Significantly reduced the trading activity of Australian financial stocks.

- a. Specifically, the average turnover of Australian financial stocks during the period of the ban declined by more than 40% compared with the pre ban period.

- b. When the short selling ban ended on 25 May 2009, the turnover of Australian financial stocks rose sharply and remained significantly higher over the following two months.

2. Increased bid and ask spreads.

3. Increased intraday volatility.

4. No evidence for lasting price support from the restrictions.

The Australia Securities Investments Commission, (ASIC) also issued a report (2012) on the impact of the short selling ban post the GFC and have concluded that:

- The data suggested short selling lagged rather than led price falls,

- The short selling ban may have intensified stock price declines (as this would not be possible post-ban), and

- There was no statistical or economic evidence that short selling was driving stock price declines before the introduction of the ban in Australia.

While these findings are solely based on the Australia equity market, there are observations that could hold true for other markets, and therefore warrant careful consideration.

IN CONCLUSION

With the growing sophistication of financial markets, exchange market structure now plays an ever-important role in preserving the integrity of the markets, especially during periods of turmoil. The key to implementing successful trading curbs, is to set rules and threshold levels that strike a balance between the intended and unintended consequences, factoring in the unique investor base and market structure of the exchange. Asia markets must continue the pursuit of the most optimal set of trading curbs and controls, for the benefit of the investment community worldwide.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Related articles

-

Options are 65% of derivatives volumes in traditional finance, but less than 5% in crypto.

-

Average daily volume grew 15% with record volume in interest rate, agricultural & metals contracts.

-

The exchange hit records across asset classes in the second quarter.

-

The platform is based on CONNEQTOR, developed by the Tokyo Stock Exchange and Fujitsu.

-

Minneapolis Hard Red Spring Wheat Futures are trading on the new platform.