By Chenhao Qian, Vice President, APAC AES Systematic Coverage, Credit Suisse

The global investment and trading landscape has seen an evolutionary shift — advanced machine learning and data mining techniques have taken centre stage, as investors demand systematic approaches to alpha generation and risk management. As the top managers scour global markets for opportunities and liquidity, they are increasingly looking to China as an exciting place to deploy capital.

The past few years have witnessed a rapid rise of domestic and international quantitative management in China. A recent report from a Chinese financial data provider shows that onshore quantitative fund managers managed assets in excess of 600 billion yuan (USD 93 billion) as of December 2020, a figure that nearly doubled from a year prior. In the offshore international fund management space, we have not only seen an increased level of trading activity from global hedge funds into China equities, but also an increasing number of global managers raising onshore capital via WFOE (wholly-foreign-owned-enterprise) and PFM (private fund management)structures that enable them to tap into new pools of capital while leveraging their global expertise and branding to expand their local footprint and market share.

This meteoric growth is fuelled by the changing market structure, evolving regulation, and accelerated market reforms — factors that present both opportunities and challenges for quant investors trading in China.

Market liberalization – Leading the Charge for Quant Growth

Continued economic liberalization, market reform and technological advancement in China have made the onshore equity market more accessible and transparent than ever before. With the progressive upweighting of A-shares in regional and global benchmark indices, exchanges and regulators are responding to foreign investment appetite by relaxing QFII rules and enhancing market access options.

Foreign investors have long been constrained by the lack of hedging options available to them. Onshore domestic funds are able to efficiently manage market-neutral portfolios by utilizing liquid CSI300 and CSI500 futures contracts, but offshore investors face various regulatory hurdles and cannot enter into positions with ease. A key development of the QFII reform effective from Nov 2020 may potentially allow QFII holders to trade onshore listed derivatives with greater flexibility than previously possible. Although full regulatory approval is pending, the proposed rules lay the foundation for a new era in more effective cross-border portfolio management.

Another highly anticipated market structure development is the expansion of the onshore Securities Borrowing and Lending (SBL) market for QFII investors. Single-stock hedging is a key element of many market neutral strategies, including statistical arbitrage. Successful deployment of such strategies has historically been met with heavy obstacles due to restrictions and constraints on inventory access. However, as part of the announcement made in Sep 2020, proposed rules create the start of a framework for QFII investors and brokers to tap into the SBL market, and a few foreign institutions have already executed inaugural stock borrow transactions in late 2020.

Over the years, onshore SBL capacity has gradually expanded especially after the 2019 inclusion of local mutual funds into the pool of eligible participants. There are now more than 1,600 stocks eligible for SBL. Nevertheless, on a relative basis, the volume of SBL activities is still dwarfed by the vast $10 trillion China stock market (market capitalization). In the future, it is expected that the introduction of major ETF providers and QFII to the SBL supply base will spur further diversification and stability of inventory, which will ultimately lead to an increase in trading, more abundance of liquidity, and more efficient markets.

Technology Evolution

The implementation of successful quantitative strategies would not be complete without effective market connectivity. As rapidly evolving trading technology continues to benefit and challenge quant strategies, access to low latency market data and Direct Market Access (DMA) has become a necessity.

One of the regulatory measures that followed the 2015 China stock market crash was to restrict DMA (for private investment funds) to the local exchanges. Since that time, quants have had to seek an alternative by partnering with local brokers to get a share of their limited network bandwidth, which inevitably placed significant pressure on brokers due to their resource constraints. This situation led to large discrepancies in the quality of market access made available to quant investors of varying sizes and operating tenure. In early 2019 the landscape began to change when local regulators engaged the industry in a consultation to assess the re-launch of DMA connectivity. It is widely believed that, once the reforms are announced and ratified, true DMA connectivity will usher in a period of rapid trading technology development, innovation, and a diversification of A-share quant strategies operating onshore.

The market data distribution mechanisms in China are very different to those used by other major global exchanges. While most major exchanges publish market data (quote and tick data) in real-time streams, China disseminates its market data in three-second snapshots. This delay, in addition to the staggered distribution of snapshots, results in asynchronous market data feeds which pose challenges for both investors who are using trading algorithms, as well as brokers who are implementing trading risk controls. Moreover, offshore investors experience additional market data feed latency that results from geographic distance and intermediate network hops. However, in 2019, Shenzhen Stock Exchange upgraded the market data interface to stream high speed tick-by-tick quotes, making it possible for data vendors to construct and distribute a real-time continuous order book feed to consumers. In the same year, Shanghai Stock Exchange followed its southern counterpart’s lead and included real-time trades in its feed, paving the way for low latency quote distribution. This development is welcomed by all investors, especially quants, as decision making and trade execution significantly improve with access to real-time accurate price and liquidity information.

The changing face of the investor base – Institutionalization of A-shares

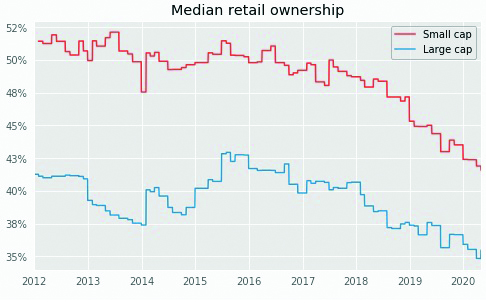

The A-share market is one of the most liquid markets in the world, thanks to the active participation of retail investors. More than 1,000 stocks in China had an average daily traded value of 30M USD or more at the end of 2020, creating a favorable environment for quant strategies that thrive when an abundance of liquidity can minimize market impact and reduce trading costs.

Interestingly, contrary to the global retail trading boom that was spawned by the coronavirus pandemic, the liquidity composition and equity ownership in China have seen a gradual diversification and maturation. Over the past few years, we have seen the investor base shift towards institutions, indicating that the historically retail-dominated market is transforming into one where individual investors are increasingly transferring their wealth management needs to the hands of professionals.

A recent interview conducted by the Credit Suisse Quantitative Insight (CQi) team on 200 A-share investors showed that respondents’ moods were far from overheated despite the frenzied local market rally in July. With a healthy push from the government to encourage retail participants to direct family savings to institutional investors, rather than trading single stocks, the China onshore market saw a record breaking 3 trillion RMB in new mutual fund issuance in 2020. The combination of growing foreign investor ownership and an increasing number of institutional participants engaged in large block trades is establishing disciplined investment approaches and improving the market’s efficiency. This shift in the market composition may pose both challenges and opportunities that quant investors must be aware of and prepare to navigate.

Ready to Grow

While quant investing in China is still at an early stage of development, it is already grabbing headlines by delivering superior outperformance to market benchmarks. The introduction of favorable regulatory policies and structural reforms will usher in a more efficient and mature market. As advanced technology and robust datasets become increasingly available, the next stage in this evolution will likely see quant investors not only harness a plethora of AI techniques but also develop novel insights and unique approaches at scale, thereby fostering greater liquidity growth, spurring innovation, and further advancing China’s prominence within the global asset management industry. •

Sources:

Bloomberg, CBIRC, CIIS, Credit Suisse Plus, CSFC, CSRC, FactSet, HKEX, PwC, SIMUWANG.COM, SSEINFO, STCN.COM, SZSE, ZQRB.CN

China: The Meteoric Growth of Quant Investing first appeared in the Q1 2021 issue of GlobalTrading

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Related articles

-

This enables transfers amongst Schroders’ clients and unlocks use cases such as collateralisation.

-

BlackRock, BNY, DTCC, Standard Chartered are exploring integrations before the launch in September.

-

The two funds mark the debut of ETFs from an Austrian investment manager.

-

Clients get automated access to real-time banking data and payment capabilities.

-

The alternative asset manager has also created more than 2,000 ICE IDs for private market assets.