Cboe opposes the SEC’s Transaction Fee Pilot because we want to protect public investors from the harm it will cause.

Bryan Harkins, Executive Vice President, Co-Head Markets at Cboe Global Markets, offers a counterargument to the opinion piece, “The SEC Wants to Give Public Investors a Fair Shot.”

A recent Wall Street Journal opinion piece authored by Professor Larry Harris of the University of Southern California attempts to make the case for the U.S. Securities and Exchange Commission’s proposed Transaction Fee Pilot, a pilot program intended to study how exchanges’ price mechanisms may impact broker routing behavior.

Alarmingly, the author misses the point on the fee pilot. As we’ve publicly stated in the past, we believe the transaction fee pilot will harm the exact people it intends to help—the investing public—in the form of wider spreads and increased transaction costs.

The Truth Is, Investors Today Are Better Off Than They Have Ever Been

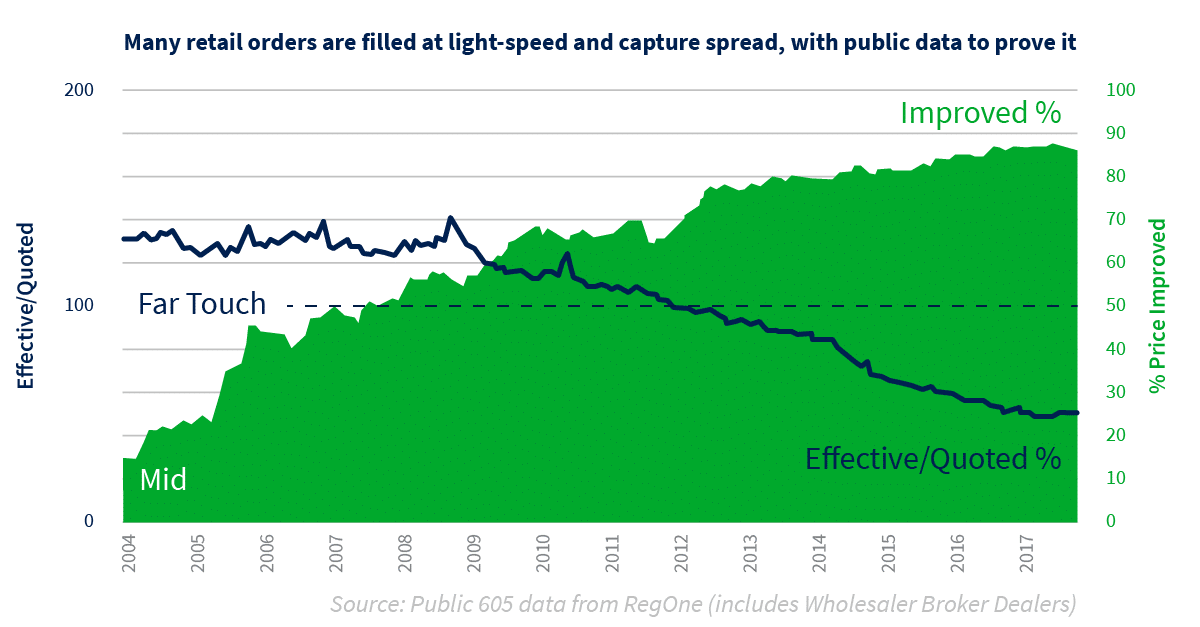

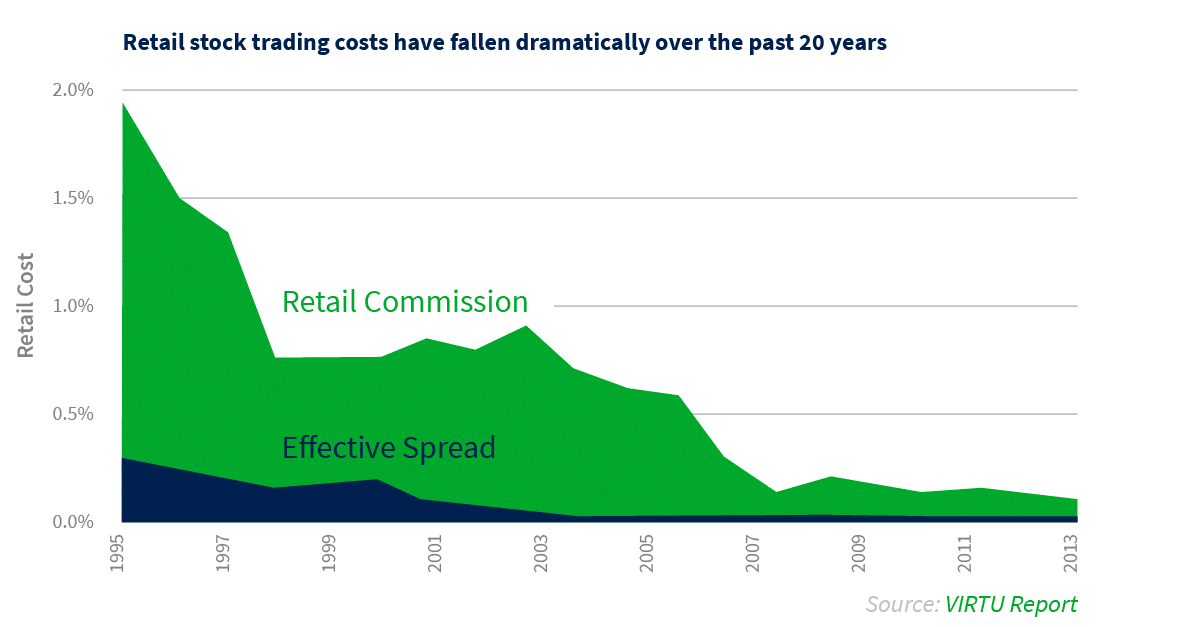

The current system is not “stacked against investors” as the piece claims, the opposite is true. The investor experience today is better than ever with lower costs, significant liquidity, narrower spreads and faster executions.

Continuous innovation by, and competition among exchanges has led to new technologies, and increased choice, quality and access to the markets that benefit the entire investing public. All-in trading costs have continued to come down for retail investors, who can access market information and analytical tools at little to no cost, and buy and sell stocks instantly. This is particularly relevant in the face of the fee pilot, which seeks to drastically alter the maker-taker exchange landscape.

In our view, the U.S. equity market has never been fairer, more cost-effective or more liquid.

Maker-Taker Exchanges Incentivize Liquidity

A key driver behind the deep liquidity in the U.S. equity market is the “maker-taker” exchange. Maker-taker exchanges incentivize liquidity, narrowing spreads and thereby benefitting investors. Maker-taker pricing was fully established by the mid-2000s, and since then, spreads and trading fees have plummeted. In fact, since the introduction of Regulation NMS, investors are far better off across a multitude of factors.

Conversely, if you remove maker-taker exchanges from the NBBO, spreads are necessarily wider. This means investors get worse prices on their trades. To put things into perspective, we had looked at one of most heavily-traded ETFs, the SPDR S&P 500 ETF (SPY), as an example. For SPY, the average time-weighted spread aggregated across exchanges (the NBBO) was $0.010; however, the NBBO was 50% wider ($0.015) when maker-taker exchanges are removed from the NBBO.

Taking a look at inverted, or “taker-maker” exchanges. The author of the Journal piece assumes that high frequency traders (HFTs) are driving all the inverted volume in the equities markets. Sadly, he offers no data or facts to back up his claims. Cboe, which runs two inverted exchanges, is more than willing to work with academics on their research, and we think the author would have arrived at a different conclusion based on our data.

On our EDGA Equities Exchange – one of the industry’s leading inverted markets – two-thirds of volume on the make side is attributed to agency brokers. By definition, agency brokers are executing those orders on behalf of clients. This means that market professionals, who have a fiduciary duty to their clients, have found value and utility in inverted markets. From our vantage point, that’s a far cry from the opinion that inverted markets are only for HFTs to jump the intermarket queue.

There is value to both maker-taker and inverted models. There are different types of market participants and we believe those participants should be able to choose which pricing model best suits their trading and investment objectives. That is why Cboe itself operates two maker-taker exchanges (BZX, EDGX), and two inverted exchanges (BYX, EDGA). If market participants did not find utility in each of these market models, Cboe would not provide them.

Exchanges are Home to Transparency and Price Discovery

Exchanges are where buyers and sellers gather. Investors of all stripes rely on the transparency and price discovery that exchanges provide. From the moment an investor order is submitted to a broker, to the moment a trade confirmation is returned to the investor, the exchange portion of this process is far and away the most transparent part of the cycle. Every charge and order-handling action an exchange takes must be filed with the SEC for review and be made publicly available in the exchange’s rulebook.

Transaction Fee Pilot – A Solution in Search of a Problem

Unless the Transaction Fee Pilot is the start of a broader examination of how our markets function today – the system of exchange medallions, order protection, locked and crossed markets, latency concerns – the results will not be conclusive. And we believe the burden will fall on the public investors the SEC is trying to protect.

We’ve seen this before. The SEC’s Tick Size Pilot, which sunset earlier this year, cost investors $700 million on an annualized basis and involved countless man-hours to implement.

As we’ve stated before, the fee pilot is a solution in search of a problem. Large-scale experiments, like this fee pilot, are not appropriate especially when costs are down, spreads are narrow, executions are fast, and the overall investor experience in trading U.S. equities is better than it’s ever been. And the exchanges are the ones working to protect that each day.

Based in New York, Bryan Harkins is defining markets as he co-runs the sales, product development and competitive strategy for Cboe’s U.S. equities, futures, options and global foreign exchange businesses, its suite of market data and access services products, as well as the firm’s growing ETP listings business. Learn more about Bryan, here.

Based in New York, Bryan Harkins is defining markets as he co-runs the sales, product development and competitive strategy for Cboe’s U.S. equities, futures, options and global foreign exchange businesses, its suite of market data and access services products, as well as the firm’s growing ETP listings business. Learn more about Bryan, here.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Related articles

-

Robinhood will also launch a blockchain to power the tokenization of real world assets.

-

The investment will support tech upgrades, market expansion, team growth & enhanced platform features.

-

Lazard Asset Management says the continent’s 8.5 hour trading day is outdated.

-

Entities are encouraged to submit their requests to participate by 25 July 2025.

-

This will be the first SEC approved exchange to offer 23-hour weekday trading of U.S. equities.