Open Platforms Opening New Horizons: How to Bring Innovative Tech to Capital Markets

Open platforms provide opportunities for innovation for technology producers and consumers.

By Arin Ray, Senior Analyst, Celent

Arin Ray, Celent

A trilemma is playing out in the capital markets landscape as banks look to comply with a changing regulatory environment, meet clients’ evolving demands, and improve business economics. The COVID-19 pandemic intensifies the urgency of addressing each of these themes.

Technology—critical for executing business and operating strategies—is at the forefront of the capital markets industry. Trading is becoming increasingly electronified across asset classes. Digital tools are reshaping clients’ preferences and expectations. Yet, technology adoption level varies greatly based on a bank’s current position and future plans.

Explore the Fintech Ecosystem

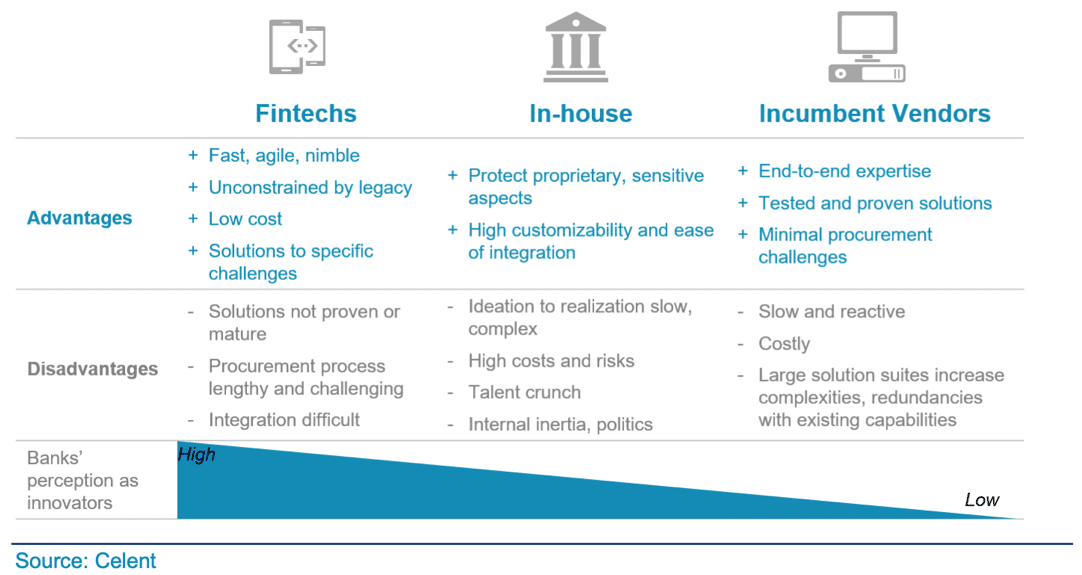

Historically, banks have relied on in-house resources for technology development. Incumbent vendors with proven expertise are still the top picks for running critical pieces front to back, but they aren’t perceived as being highly innovative. Increasingly, fintech providers are viewed as key drivers of innovation. So, banks are exploring various ways to engage with the fintech ecosystem, with some banks serving as clients, co-creators, collaborators, incubators, investors, or partners.

But banks’ ability to easily access and integrate new fintech solutions is constrained by limited budgets, complex and inflexible internal technology, and onerous vendor management needs. Interacting with the emerging fintech ecosystem can be made easier with growing adoption of cloud, application programming interfaces (APIs), and platform-based business and operating models.

Consider the Role of Open Platforms

Open platforms provide a new horizon for technology producers and consumers for accelerating the adoption of innovative technologies. A previous Celent report on platformification provides the basis for a functional definition of open platforms: “Open platforms allow multiple participants (producers and consumers) to connect, interact, create, and exchange value with each other. For example, a vendor can offer a suite of product capabilities that is open to any third party from which new products and services can be built from and consumed.”

A recent study by Celent, commissioned by Finastra and based on detailed discussions with senior executives at banks and technology solutions providers, discusses trends and themes in banks’ technology transformation journeys with a focus on banks’ attitude toward and desire for open platforms.

- All banks in the study were aware of open platforms and a vast majority (89%) are currently using or exploring usage of open platforms.

- Lower cost of entry to innovation and access to a trusted set of fintechs are the biggest drivers behind the interest in open platforms, each noted by 61% of participant banks. In their view, open platforms would make the fintech vendor discovery process easier and expedite vendor onboarding.

- Regarding their engagement with open platforms, buying solutions from the platform was the near unanimous choice (94%), and many banks are also interested in building solutions themselves as well as sharing them with others on open platforms.

- Despite being a new concept in capital markets, open platforms are rapidly gaining ground, with 67% of survey respondents indicating that they expect to use open platforms within two years.

Evaluate the Use Cases for Engaging with Open Platforms

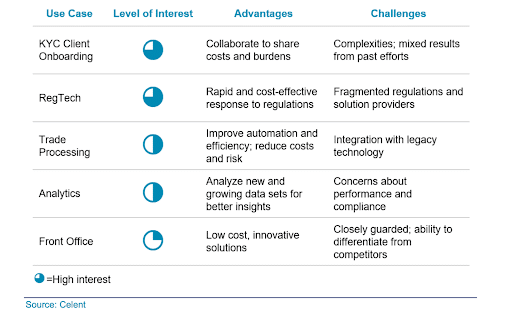

Early interest in open platforms is focused on use cases for solutions that are not core to bank operations, with know your customer (KYC) onboarding taking the lead, as noted by 70% of respondents. Regtech solutions are the second biggest area of interest and solutions that can help banks navigate the complex regulatory environment are in high demand.

The next big area of interest is in trade processing; banks are interested in low-cost solutions for confirmation, settlement, reconciliation, communication, document management, collateral management, and reference and market data. There is also high interest in analytical tools, especially leveraging artificial intelligence (AI) and machine learning, that can help banks analyze risk, price movements, market events or sentiment; optimize use of cash, liquidity, funding, and collateral; or improve operations such as in reconciliation and exception management.

Banks are more conservative about front office technology; here, they are primarily interested in external solutions in analytics, business intelligence, or visualization tools that can be customized to create differentiating propositions. When it comes to technology innovation, many banks are not primarily motivated by specific use cases and are more attracted to the possibilities of discovering new solutions through open platforms, especially ones driven by new technology.

Embark on The Transformation Journey

Over 90% of respondent banks at this point are mainly interested in finding new solutions from open platform. They want innovative solutions to vexing business problems that are credible and vetted by the platform or platform participants and are easy to procure from a vendor risk management perspective. Ease of integration with internal systems is another criterion because not all banks are willing or ready to make significant internal changes for connecting with the open platform ecosystem at this stage.

About half of respondent banks have already undertaken significant internal technology change projects as part of their transformation journey by adopting cloud or open APIs and are seeking to find easier means to connect internal systems with external agents (clients, vendors). These players are open to making internal upgrades or adjustments if they find valuable solutions on open platforms that conform to their internal security and compliance requirements.

Around a quarter of respondent banks are further ahead in the technology adoption curve having already adopted cloud, open APIs, standards, interfaces, and consolidated internal platforms. They are better equipped to deal with the intricacies of the open ecosystem. These banks are not only eager to find new solutions but also to engage with open platforms to develop new solutions and even co-create solutions working with fintechs or peer banks on the open platform.

As banks move to adopt open platforms, concerns will need to be addressed, such as security considerations, integration with existing systems, and data privacy issues. The general view, as indicated by more than 70% of respondents, was that these concerns would not be show-stoppers if the platform has a thriving ecosystem and it solved some of their pressing needs for cost reduction and technology innovation.

Interoperability will be important in driving the adoption of open platforms; the industry will need to continue its work in this aspect. Adopting open innovation principles can foster greater interaction and connectivity within the ecosystem and help close the “innovation gap” between a few large resourceful banks and smaller players struggling to merge new-age technologies with their existing infrastructure.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Related articles

-

The electronic syndicated loan trading platform has also raised $46.5m.

-

Addition of India further expands MarketAxess’ emerging markets offering.

-

This will facilitate the launch of a CLO trading platform and developing data and analytics.

-

Average daily volume for May increased 33.3% year-over-year.

-

The firm launched its targeted block trading solution in U.S. credit in mid-May.