By Chris Monnery, Electronic Execution Business Development, Fidessa

Chris Monnery, Fidessa

Last month, I had the pleasure of moderating a panel on the changing needs of the Buy Side from an OMS/EMS and execution perspective. This led to a lively debate on what the Buy Side is looking for, and how ready the Sell Side is to provide it.

As a vendor that services both the Buy and Sell Sides, Fidessa is uniquely placed to recognize nascent trends in their relationship. Nowhere does this become more in-focus than in electronic trading, where we see the Sell Side is wholly focused on providing a differentiated execution service for their clients. Service means many things, but I sum it up as being able to handle whatever the client is looking for – be that a customized execution strategy, meeting specific order handling terms, or sourcing liquidity better than the next broker.

To kick-off the conversation, we performed an acid test to see if both sides aligned.

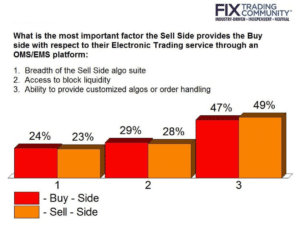

Question: What is the most important factor the Sell Side provides the Buy Side with respect to their Electronic Trading service through an OMS/EMS platform?

Who expected the Buy Side and Sell Side responses to so closely align? Seems the Sell Side knows what the Buy Side needs, but are they delivering?

With almost 50% of the vote pointing to Algo customization and order handling, it’s clear that Buy Sides are upping their demands in terms of how orders are handled, and are consistently getting more involved in how their brokers are executing their orders. From a Sell Side perspective, there is a recognition of this growing need to accommodate this level of service.

To me this opens a new question: Is the current technology within Low Touch Trading able to deliver within this new demanding climate? Traditional setups consist of linear routing from the connectivity platform to the Algo container. While basic customization and tag manipulation can be handled in the FIX layer, anything more complex has to sit in the Algo container, and this setup remains an inflexible configuration. Maybe it’s time for the Low Touch OMS to take a greater role in the management of the order, rather than just being the platform the Low Touch trader uses to watch his orders and manage his exceptions?

The second most important factor is around the holy grail of liquidity. The results indicate that the Buy Side also values seamless access to block liquidity. This is something we see reflected from our Sell Side clients, and is a key differentiation whether it’s on the High Touch or Low Touch channel. The concept of a client “opting-in” to access a broker’s captive liquidity was discussed by the panel. The consensus was that this is becoming increasingly important, however it remains a somewhat clunky process due to coverage models and the use of multiple technology stacks.

Not discussed, but certainly growing in market share both in the US and Europe, are contingent venues. It’s a simple concept – ‘I’ll trade in size if there’s someone on the other side’. The challenge comes from systematically handling both a working benchmark order and the invitation to firm up from a contingent venue. From the Buy Side’s perspective, this may be a simple decision, but the Sell Side carry’s the burden. In order to access this liquidity, the Sell Side must manage the disparate venues, their rules, their terms and apply complex timing decisions to manage the scoring with the venues themselves. And don’t forget, they have to do all this without increasing the overhead on the trader. As more liquidity continues to transact on these venues, Sell Sides will find themselves with no choice but to provide this service. This is already being seen as a major differentiation, and will likely feed back into the customization discussion as well.

In summary, Low Touch order flow is becoming less about Algo routing and more about the Sell Side being able to say ‘Yes” to their Buy Side’s demands. Whether this is from external factors such as MiFID II, or simply the Buy Sides desire to better control their order flow, there is a a clear shift impacting the Sell Sides technology requirements. We see this growing need for ‘execution as a service’ as the major trend driving the evolution of the Low Touch space.

For more information on Fidessa, their High Touch and Low Touch platforms, and services simplifying access to block liquidity, please contact Chris Monnery at: ElectronicExecution@fidessa.com.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Related articles

-

Members can source block liquidity while working algorithmic strategies in the broader marketplace.

-

The integration of dbHedge into LiquidityFX augments smartTrade’s existing tools for internalising FX flow.

-

The briefing touches on emerging technologies and outlines considerations for using AI.

-

There was a 34% improvement in predicting how likely a trade would be filled at a quoted price.

-

Execution algorithms are a growing share of global spot FX, particularly among buy-side firms.