The following Q&A with Michael McCreesh, President of Battea Class Action Services, originally ran in GlobalTrading.

Describe the transition from working at a global investment bank to Battea? Was your experience at Goldman Sachs transferable to what you are doing now?

When you’ve spent 25 years at one institution, the concept of transitioning to something different is often bigger than the reality of it. Once I got over the sheer size difference of the firms, I quickly realized that how they operate is not that different. At its core, the skill sets required are very much the same. Battea is a growing firm–in a growing market space–that must optimize resources, technology, marketing and client base. Many of the traits that are required to maintain such growth are equivalent to those that were needed in the businesses I ran at Goldman Sachs.

First and foremost, we focus on client relationships. Fortunately, the client base at Battea consists of the buy and sell-side–similar firms that I covered and liaised with at Goldman Sachs–providing the ability to bring long-standing relationships based on trust to a new business value proposition. Early returns are showing that trust transfers, so my goal of raising market awareness to this new revenue opportunity is paying dividends. I believe in the continued opportunity for further growth for the securities class action market and the inherent value to the client base. I look forward to helping Battea continue to grow its business and serve the global financial community.

How important has the recovery process become in today’s trading markets and why?

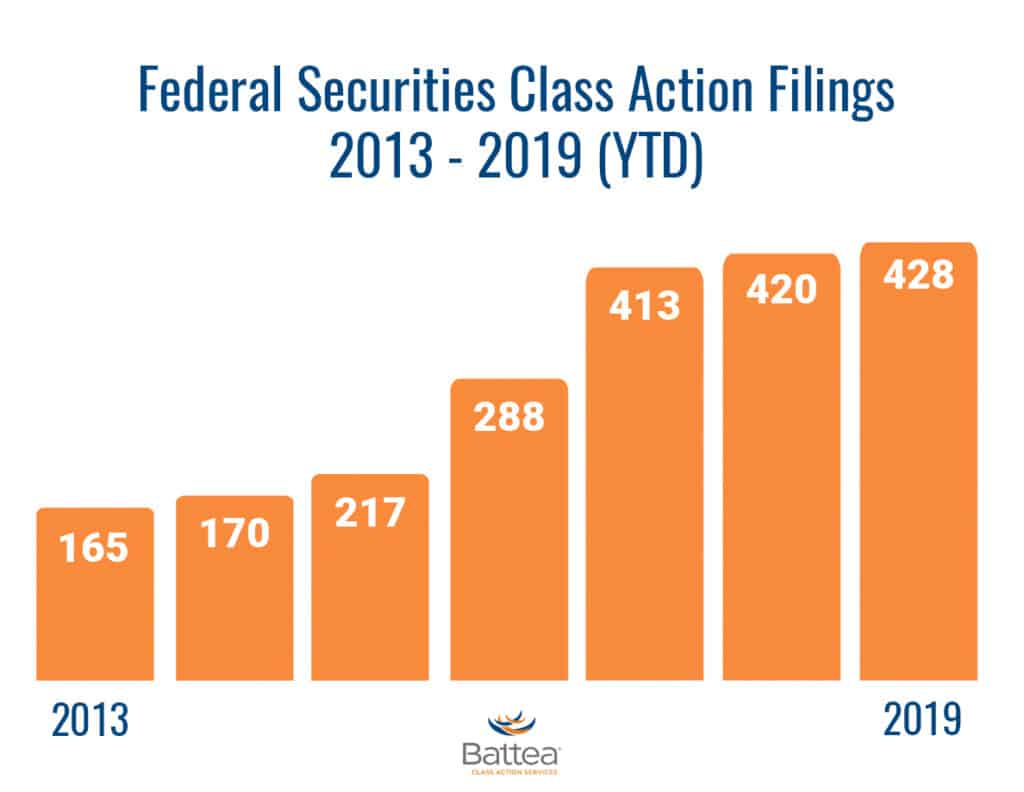

There has been incredible growth in securities and antitrust class action litigations and settlements, particularly as they have unfolded in 2017, 2018 and 2019. The number of new cases and new settlements from traditional securities litigation to antitrust rate rigging, spread inflation and other forms of collusion are at an all-time high and shows no sign of slowing down.

One misconception is that when investors’ holdings are eligible for a claim in a securities or other financial instrument antitrust class action lawsuit, recovery for losses is automatic. It is not. It is necessary that investors take proactive steps to assert their claim in each different case. If a settlement is reached, or investors are required to opt-in to a foreign litigation, investors enlist the services of Battea Class Action Services to review all their transactions and create an analysis and filing compliant with the requirements of each case.

Due to the vast variety of different types of cases in different jurisdictions, this has become such a comprehensive process that it requires significant expert resources and lends itself to outsourcing to an expert. Once filings have been submitted, there is often an extensive dialog with the Court-approved Claims Administrators to deal with further audit documentation, exception handling or disputes over transaction treatment. We stand out in this area and often provide expert input or constructive advice to class counsels and claims administrators. We fight for our clients’ rights and give due consideration to every transaction that should be honored in a settlement.

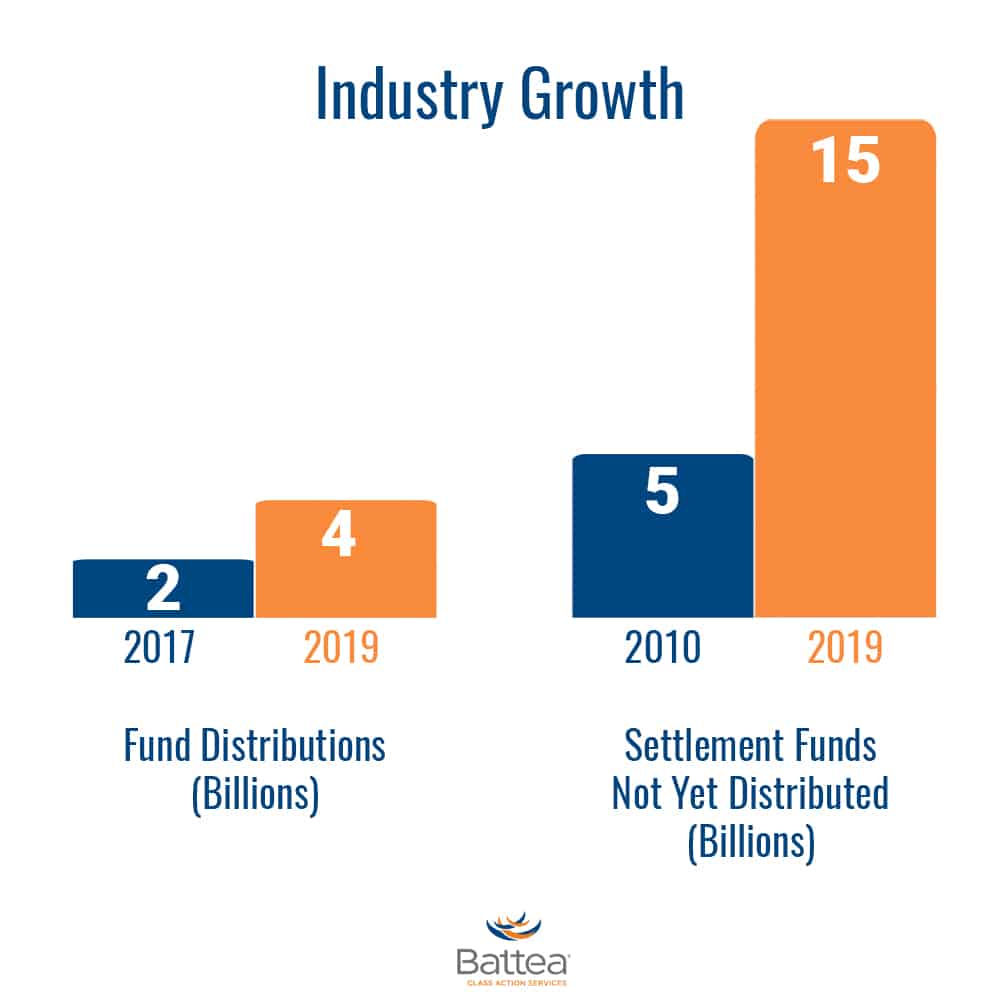

Billions of dollars will be available to eligible investors in the interest rate-rigging, foreign exchange, commodities, and “plain vanilla” equity case settlements. However, industry members will soon learn that the extensive class periods, determination of jurisdictional execution locations, lack of securities identifiers (i.e., CUSIPs, SEDOLs, etc.), a vast array of instruments, and complex loss calculations make this a challenge.

Investors do not want to find themselves scrambling to gather data, deciphering settlement details, including their recovery opportunity, anonymity, and other related issues as the roll outs of the settlements quicken. In previous matters, including the recent CDS case, many claimants missed the boat or got short-changed due to the lack of transparency to loss calculations, insufficient data production, and other various reasons.

What types of cases are most common?

Securities class actions cases generally challenge allegedly materially false, misleading statements, and/or the personal actions made by the board, management, officers, directors, and various employees, from primarily publicly traded companies. While each will most certainly be different, here are a few of the more common types of cases:

Fraud, Deceit or Collusion: Fraud, deceit or collusion cases argue that a defendant engaged maliciously during the pricing, purchase, and/or sales of various types of securities, currencies, or interest rates. These claims are referred to as Rule 10b-5 claims, after the Securities and Exchange Commission rule, which prohibits such types of fraud, deceit or collusion.

False Forward-Looking Statements: False forward-looking statement cases involve an issuer’s predictions and projections regarding future corporate actions and performance of the company.

Other Common Securities Class Action Claims: Other common securities class action cases include allegations of insider trading, poor or improper corporate governance, and deceitful accounting practices.

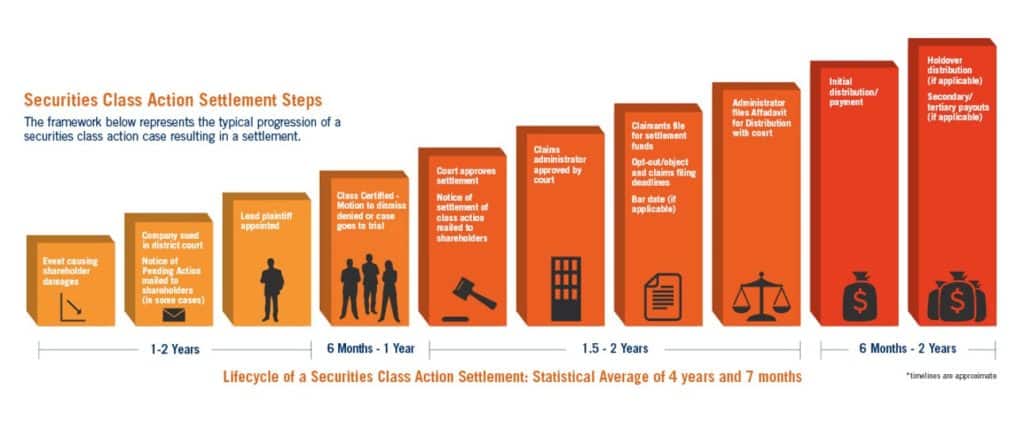

Describe the recovery process? How long does it take from claim to actual settlement?

Battea’s proven method of recovery follows the ability to track the complete cycle of a class action suit from the initial news alert through the distribution of funds:

- Data Collection

- Data Normalization

- Eligibility Analysis

- Document Verification

- Recognized Loss (“RL”) Calculation

- Claim Filing

- Claim Monitoring

- Claims Administrator Managed Communication

- Payment Processing

- Client Reporting and Transparency

- Continuous Information Flow

Complete and accurate data files result in the recovery of full awards. A client may have access to transactional records in-house, but other times, it will be necessary to contact prime brokers or other clearing agents for data files.

Due to our longstanding working relationships with prime brokers, fund administrators, custodians and other clearing agents, we can retrieve data files efficiently and in a timely manner. Therefore, our contacts in these firms are familiar with the fields and formats sought in the data request, we can overcome obstacles such as recovering data from former prime brokers.

Battea streamlines the payout tracking and payment process and provides its clients with management and accounting reports via its Portal®, either for simple review or in downloadable data formats, which enables clients to incorporate this information into their own spreadsheets or internal management reports.

Describe the state of the recovery market? What’s on the horizon?

While billions of dollars have already settled in the Foreign Exchange Benchmark Antitrust manipulation case, and have been distributed in the Petrobras U.S. ADR settlement, there are still several billions expected to settle in cases currently in litigation. We are actively monitoring the Interest Rate Swaps Antitrust Litigation (Spread Manipulation), GSE Bonds Antitrust Litigation, and on the equity side of the horizon, American Realty Capital Properties and Valeant Pharmaceuticals International (which include settlement funds of $1.025 billion and $1.210 billion, respectively).

As there are such significant sums available to damaged investors, it is crucial to act to establish a claim. Eligible investors must file claims to collect their portion of the settlement dollars. International filings require an unparalleled understanding of the filing process, the specifics of each case and the various recovery options available.

To maximize recovery potential, it is highly recommended to seek an expert firm who specializes in this area and who can provide the transparency required to validate their performance. Without having that trust there is a risk of leaving large sums of money behind.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Related articles

-

T. Rowe Price is the anchor client for ICE Compass.

-

Rantum will help build out Janus Henderson’s pan‑European private credit platform.

-

The ability to pursue two share classes in one fund creates additional options for asset managers.

-

They will receive ETP shares with exposure to spot crypto.

-

The result will be a stronger, strategically aligned U.S. wealth platform.