CLINTON OR TRUMP? IN A VERY UNCONVENTIONAL ELECTION, THE REPUBLICAN CANDIDATE IS THE ONE FEARED BY WALL STREET

IF IT AIN’T BROKE, DON’T FIX IT.

That’s the view of many trading professionals regarding the upcoming U.S. presidential election, with ‘it’ referring to the economy and markets.

It’s hardly been an economic boom in recent years, but at the same time, stock indices are at or near record highs, and markets are generally functioning well and without undue attention from Washington. So many market participants want to see Democrat Hillary Clinton raise her right hand on January 20, 2017.

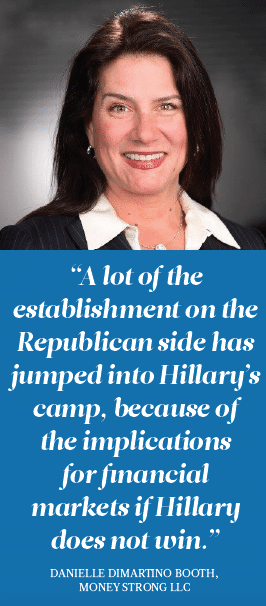

“A lot of the establishment on the Republican side has jumped into Hillary’s camp, because of the implications for financial markets if Hillary does not win,” said Danielle DiMartino Booth, president at Money Strong LLC, a consultancy focused on macroeconomics and the policies of central banks.

“A lot of the establishment on the Republican side has jumped into Hillary’s camp, because of the implications for financial markets if Hillary does not win,” said Danielle DiMartino Booth, president at Money Strong LLC, a consultancy focused on macroeconomics and the policies of central banks.

Donald Trump, the Republican nominee, has said he would probably replace Federal Reserve Chairwoman Janet Yellen when her term ends in February 2018. The prospect of Fedchief turnover, at a delicate time in the economic cycle, is worrisome.

“Very easy monetary policy has greased the wheels of financial markets for a long time, and I think the consensus prefers that that not be upset,” DiMartino Booth told Markets Media in a July 27 interview. “I certainly don’t think the market has priced in a Trump presidency in any way, shape or form. As of today, the market sees Hillary as the most likely president.”

DiMartino Booth noted that the Federal Reserve Board has had five confirmed governors and two vacancies for years, as President Barack Obama has been unable to fill either seat.

“Republicans are adamantly opposed to putting more dovish people of like mind with Janet Yellen, (Federal Reserve Bank of New York President) Bill Dudley, and others. I think that that’s why there’s this laser-like focus on trying to make sure that Hillary prevails.”

Clinton had a bruising primary battle with Bernie Sanders, and some believe that a President Hillary Clinton will be at least a little beholden to the populist wing of the party, which calls for breaking up big banks, implementing a financial transaction tax, and increasing taxes on hedgefund managers.

To that, DiMartino Booth said to look at history.

“There’s certainly the possibility” that Clinton goes after financial services in a meaningful way, she said. “But no matter who the president, no matter what the party — the lobbyists against that have always prevailed. Hillary is perceived as being a friend of Wall Street.”

ATYPICAL MATCHUP

The upcoming presidential election is one of the most intriguing and unconventional matchups in ages:

Clinton, the highly qualified yet highly flawed old-guard Democrat, versus Trump, the bombastic and capricious business mogul whose nomination has exposed deep divisions in the Republican party.

Capital markets professionals will be closely watching, not only for who wins the presidency, but perhaps more importantly, for which party gains or loses clout in the House and Senate.

Conventional wisdom, in its simplest form, holds that a Republican administration is good for business, as the party historically has backed lower taxes, less regulation, and a laissez-faire stance with regard to free markets.

By contrast, Democrats are associated with favoring bigger government, which manifests itself in the forms of more oversight, intervention, taxes and regulation. But to be sure, CW doesn’t always hold true. Democrat Bill Clinton presided over the economic boom of the 1990s, and his wife has indicated he’d have a say in the economic policymaking of her administration.

The current economy isn’t robust, but President Obama oversaw the recovery from the global financial crisis of 2008-2009, and it’s been noted that his presidency has been more business-friendly than commonly perceived.

Also, Clinton’s choice of Virginia Senator Tim Kaine as her vice-presidential nominee signals she’s putting some distance between herself and the populist camp of Sanders, her primary foe who proved much more formidable than most political operatives expected.

On the other side, Trump is a bit of a wildcard as he has no political experience and his conservative credentials are suspect. He’s a businessman himself, but it’s unclear what his positions would be on bedrock Republican principles such as free trade and low taxes. It is said that markets hate uncertainty, so markets could conceivably swoon in the fall if it looks like Trump might win, and/or if he wins the election.

On the other side, Trump is a bit of a wildcard as he has no political experience and his conservative credentials are suspect. He’s a businessman himself, but it’s unclear what his positions would be on bedrock Republican principles such as free trade and low taxes. It is said that markets hate uncertainty, so markets could conceivably swoon in the fall if it looks like Trump might win, and/or if he wins the election.

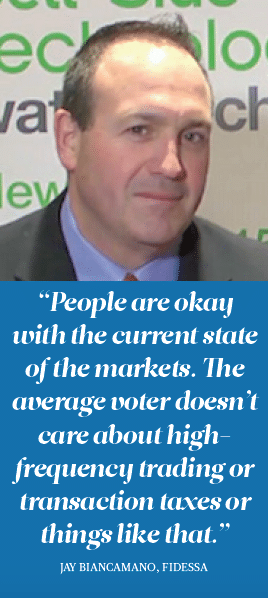

One key as to how friendly or unfriendly a new administration will be towards financial services is how markets function ahead of the election, especially in October, said Jay Biancamano, head of equities product marketing for the America at trading-technology provider Fidessa.

If markets continue operating for the most part smoothly and quietly in the background, the incoming president will be inclined to leave things be.

If there’s anything like the financial crisis of 2008-2009 — the nadir of which took place just ahead of Obama beating John McCain in November 2008 — or the ‘flash crash’ of May 2010, then market participants can expect some unwanted attention.

“We’ve become a very reactionary type of voter constituency,” Biancamano told Markets Media. “I wouldn’t put much into any of the platform issues at this point…You could make the argument that both Trump and Clinton are friendly to Wall Street, and you could make the argument that they’re not, because of what their platforms say.”

“In 2008, obviously markets affected the platform very much. We had just begun the Great Recession and voters were looking for change,” Biancamano continued. “But that’s not the case now. The market’s up. I think people are okay with the current state of the markets. The average voter doesn’t care about high-frequency trading or transaction taxes or things like that. Unless there’s some major market break in October, I think it’ll be a very benign type of banking agenda from whoever gets elected.”

DODD-FRANK… STILL A WIP

For markets, the biggest political-regulatory issue in recent years has been the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was signed into law by President Obama in 2010.

The sweeping ruleset is broadly aimed at reducing systemic risk, by making markets more transparent and curbing behavior that’s considered risky.

Specifically, Dodd-Frank has barred banks from engaging in proprietary trading and implemented more conservative capital and leverage ratios, while mandating more disclosure from hedge funds and stronger standards for clearinghouses. By way of brass tacks, more than six years— that’s 72 months, or 312 weeks — later, Dodd-Frank is still a work in progress.

According to law firm Davis Polk, as of July 19, 2016, 271 rule-making deadlines had passed; deadlines were met with finalized rules for 210 (77.5%), and rules had been proposed that would meet 29 (10.7%) more. Rules had not yet been proposed to meet 32 (11.8%) passed rule-making requirements.

Of 390 total rule-making requirements, 274 (70.3%) were met with finalized rules, and rules were proposed that would meet 36 (9.2%) more. Rules were not yet proposed to meet 80 (20.5%) rulemaking requirements, according to Davis Polk.

Not surprisingly, Clinton and Trump don’t see eye-to-eye on Dodd-Frank.

Clinton has praised the reform, and added that she would push for rules, enforcement and accountability that go further, into more lightly regulated areas of finance. She did, however, say this during the heat of a highly contentious primary campaign, when the Democratic base needed to be won over.

Trump has said he would dismantle Dodd-Frank. But it’s dubious whether he’d be able to push such a dramatic rollback through Congress. And paradoxically, the GOP standard-bearer’s platform includes a reinstatement of the 1933 Glass- Steagall Act, which would separate commercial banking and investment banking and thus effectively break up many of the largest institutions on Wall Street.

Clinton has not called for the return of Glass-Steagall. Probably the most-feared regulatory idea out there is the financial transaction tax. Clinton backs a tax specifically on high-speed traders, while the Democratic party platform calls for a broader transaction tax more along the line of what Sanders wanted.

Trump wants hedge-fund managers to pay more in taxes, and he has proposed getting rid of the ‘carried interest’ loophole in the tax code that benefits some investment managers. But he has not embraced a financial transaction tax.

It’s far from clear that Clinton will win and push on with a financial transaction tax; if she does, she faces an uphill climb in getting it passed. But the threat to trading activity — and the ultimate cost to the enduser, mom-and-pop investor — is substantial, so despite the apparent low likelihood of happening, the issue is very much on market participants’ radar.

Some of the candidates’ more dramatic proposals, such as scrapping Dodd-Frank or taxing every trade, are more about garnering applause from the base than they are realistic policy measures.

“Dodd-Frank hasn’t been fully implemented yet, so I don’t think either candidate can make a good argument about it prior to the election,” Biancamano said. “Post-election, I think nothing happens.” Regarding a financial transaction tax: “Never going to happen,” he said.

HOUSE/SENATE

The current U.S. Senate has 54 Republicans, 45 Democrats and one independent.

There are 34 seats that can potentially turn over in November, of which 24 are held by Republicans. Democrats would need to win at least four seats to take control.

Republicans control the U.S. House, with 247 seats, or 29 more than the 218 needed for control of the 435-member body.

Prognosticators say the Democrats have a reasonable chance of taking the Senate, but the House will most likely stay under GOP control.

“I would think if Clinton does get the majority in the House, you could see some movement in the banking sector, but I honestly don’t think it’s going to be at the top of her agenda,” said Biancamano of Fidessa. “If we’re talking about control of the Senate changing hands, then we’re talking about the ease with which any candidate she puts up for anything can get Senate confirmation,” said DiMartino Booth of Money Strong.

“It’s the ultimate Shangri-La if she could actually get the White House and the Senate, just in terms of the ease with which anybody she put up could be confirmed.”

Wall Street institutions take a long-term, largely neutral view, at least in public comments.

“This cycle will have its unique aspects to it versus other presidential cycles, but historically there’s always been some element which may have ultimately deferred a decision that a client might make to a later period,” Goldman Sachs Chief Financial Officer Harvey Schwartz said on a July 19 earnings conference call. “But these are short-term in nature.”

In a broad sense, the outcome of the presidential election will matter for markets and investors, but not in the way that some expect. That’s according to Russ Koesterich, head of asset allocation for BlackRock’s Global Allocation Fund, who busted a couple longstanding myths in a January 2016 report.

In a broad sense, the outcome of the presidential election will matter for markets and investors, but not in the way that some expect. That’s according to Russ Koesterich, head of asset allocation for BlackRock’s Global Allocation Fund, who busted a couple longstanding myths in a January 2016 report.

For one, over 114 years of data, whether a Republican or Democrat occupies the White House has had no statistically significant impact on U.S. equity market returns. So a GOP administration is not an automatic tailwind for markets.

Two, there is no long-term statistical evidence to support the notion that markets do better with a divided government.

Writing when Hillary Clinton appeared the most likely Democratic nominee but the Republican nomination was up for grabs, Koesterich highlighted a few areas for market participants to pay attention to.

“A Republican administration is likely to result in a Fed whose members are more sympathetic to a marginally more systematic approach to monetary policy,” he wrote. “The election will also have an important impact on the leadership at key financial regulatory agencies, especially the U.S. Securities and Exchange Commission (SEC) and the U.S. Commodity Futures Trading Commission (CFTC).”

TABLE OF CONTENTS

Editor’s Note

When was the last time the functioning of equity markets made news?

Dear Fellow STA Member

A note from outgoing Chairman Jon Schneider.

Shining Light on Dark Pools

Venue operators face scrutiny into how they conduct business.

November 8 Looms Large

Clinton or Trump? In a very unconventional election, the Republican candidate is the one feared by Wall Street.

EMSAC Comes of Age

Market structure advisory group ramps up activity, keeps SEC busy with recommendations.

CAT Moves Forward Slowly

The industry is on board with the concept but troubled by some details.

Equity Exchanges Evolve

Competition, fragmentation, and technology are among primary themes for listed-trading venues.

Market Structure Insights

Assessing the Disclose-and-Review approach to best execution. By Andrew Upward, Weeden

Spotlight on HFT Dims

High-frequency trading may not have quite gained acceptance — but at least the pitchforks have been put aside.

T+2 Draws Closer to Reality

But will new technologies complicate the migration?

Maker-Taker Under the Microscope

Has the nearly 20-year-old exchange pricing model outlived its usefulness?

Re-Imagining Reg NMS

Landmark equity-market ruleset is showing its age; how to update?

Options Auctions Vex Market Makers

Sidelines transactions diminish already-challenged displayed liquidity.

The Market Data Battleground

Data fees are ridiculously expensive… at least that’s what the brokers say.