2008 started out with some market disarray, as the housing bubble had popped around mid-2007, and the multi-year economic expansion was in jeopardy. But the climate wasn’t excessively tempestuous and the market uncertainty wasn’t necessarily any worse than at any other time; indeed, some prognosticators were still calling for a ‘soft landing’ in housing, echoing Federal Reserve Chairman Ben Bernanke’s now-infamous statement that housing woes would likely be “contained” to the subprime sector.

But bears won the day as markets lost their legs, sentiment cratered, and Wall Street faced a reckoning. Bear Stearns, founded in 1923, was sold in a fire sale to J.P. Morgan Chase in March 2008. Lehman Brothers, founded in 1850, filed for bankruptcy in September, right around the time Merrill Lynch, which had been independent since its founding in 1914, agreed to a purchase by Bank of America.

The consolidation and reshuffling of the largest investment banks, known collectively as the bulge bracket, in one year was more than typically might occur over a decade or more. And tough times didn’t end there, as the ensuing ‘Great Recession’, tightening regulation, and slowdown in market activity have kept firms back on their heels.

One notable impact for the institutional investment managers who rely on sell-side broker dealers for technology and trading products and services has been a scaled-back suite of offerings and fewer humans working the desk. That has been at least partly offset by improvements from a hungrier contingent of Wall Street firms that need to do more with less, amid intense competition for order flow.

“On one hand, utilizing low-touch trading tools, expanding commission sharing arrangements, and having access to more specialized research at lower costs has benefited the asset manager,” said Steve Hedger, managing director of trading and investment operations at Fifth Third Asset Management, which manages about $9 billion. “On the other hand, the disappearance of several bulge-bracket firms and low utilization of high-touch trading desks has only added to the ever-increasing problem of sourcing liquidity.”

(Broker-dealers) have been trying to find creative ways to solve some of the block trading and liquidity impediments to

capture more order flow. Steve Hedger, managing director of trading and investment operations at Fifth Third Asset Management

Equity trading rose during the financial crisis of 2008-2009, but market participants noted the increases were associated with volatility spikes caused by the economic tumult, and as such were neither healthy nor sustainable. Volume averaged almost 11 billion shares per day in early 2009, but then declined steadily to as low as 6 billion shares per day in the third quarter of 2012, and have picked up only modestly since.

Buy Side Less Active

The biggest changes since 2008 are tied to market structure, liquidity providers, and “how it has evolved from a human-driven to a machine-driven process and the role of quantitative and electronic market making,” said Jose Marques, global head of electronic equity trading at Deutsche Bank. “This has had a huge knock-on effect in terms of impact on algo providers and their cost of being in the business, especially on the smaller guys.”

The contraction in trading volume has been driven partly by buy-side asset managers turning to lower-turnover, more passive investment strategies, according to Marques. This trend favors bigger broker-dealers, he said.

“The commission pool has contracted materially,” Marques told Markets Media. “When the buy side looks at their trading counterparties, they’re looking at not only execution quality, but then in a world where you have fewer dollars to pay your good relationships, you’re going to focus those dollars where you can get the most benefit. The buy side is moving away from the smaller, independent broker-dealers, because they need to concentrate on where they can get the most bang for their buck.”

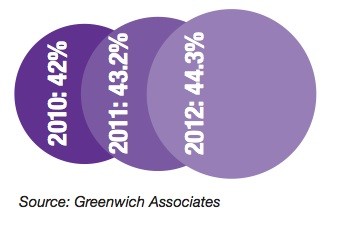

Data show that bulge-bracket banks have gained ground. Credit Suisse increased its market share for U.S. equity trades to 9.5% in 2012, up from 8.9% in 2010, according to Greenwich Associates. Bank of America Merrill Lynch gained from 8.3% to 8.9%, while J.P. Morgan and Goldman Sachs increased their shares from 8.6% and 8.3% to 8.9% and 8.6%, respectively.

“Independent agency firms have been struggling over the last few years,” said Sang Lee, managing partner at Aite Group. Overall, the top five bulge-bracket firms increased market share from 42% in 2010 to 44.3% in 2012.

Regional and boutique broker-dealers “don’t have the resources to compete with the bulge brackets,” said Rod Burns, director in portfolio products at Bank of America Merrill Lynch. “Building and maintaining the trading infrastructure to remain an institutional desk and have institutional offerings has become much more difficult. The bar has been raised significantly.”

The market has been cluttered with 100-to 200-share lots. Investment flow is challenged to find each other in the current market structure. Rod Burns, director in portfolio products at Bank of America Merrill Lynch

The bulge bracket, down one from five years ago, consists of Bank of America Merrill Lynch, Barclays (which bought Lehman’s U.S. assets), Citigroup, Credit Suisse, Deutsche Bank, Goldman Sachs, J.P. Morgan, Morgan Stanley, and UBS. More importantly, the bulge bracket has shed tens of thousands of jobs since 2008, and true high-touch trading service is a scarcer commodity.

“There are fewer sales traders,” said Michael Wszolek, chief trading officer at the New Jersey Division of Investment, which manages about $75 billion. “Looking at it from the perspective of the buy side, they get way overloaded at times. Generally speaking, we don’t have the confidence we once did, because sales traders can get so overloaded.”

These days, a Wall Street broker is by necessity more inclined to place a trade order in an algo — in trading vernacular, ‘set it and forget it’ — and less inclined to ‘work’ an order. The situation is akin to an overwhelmed babysitter who resorts to plopping a three-year-old charge in front of the television.

“It’s a battle every day” to monitor how brokers are handling orders, Wszolek told Markets Media. “They put the tools on our desks for us to manage algos and watch for ourselves. But it comes full circle, as our desk has gotten very lean, and we’re leaning more on algo providers to be higher-touch for us.”

Tougher Business

Broker-dealers of all sizes, ranging from Wall Street titans to two people in a garage, have been squeezed since 2008. There were 4,428 broker-dealers registered with Financial Industry Regulatory Authority as of March 2012, down 11% from about 5,000 in 2007.

Trade handlers below the rarefied air of the bulge bracket aren’t going to be better one-stop shops than the biggest firms, so they need a distinct value proposition, especially given the recent caution of end users. For so-called agency broker-dealers such as WallachBeth Capital, that value proposition is pure execution.

“The post-2008 landscape is dominated by a focus on sell-side fiduciary obligations and potential conflicts of interest, particularly with respect to trade execution and trading relationships,” said David Beth, president and chief operating officer at WallachBeth. “The downsizing of the traditional investment banks has certainly created opportunity for tech-savvy, independent broker-dealers, specifically those who serve in an agency capacity and can deliver what many buy-side customers seem to want most of all: conflict-free relationships that don’t raise red flags when challenged to document how, where, and why trades were executed.”

There should certainly be enough flow to go around to those who can add true value. David Beth, president and chief operating officer at WallachBeth

New York-based WallachBeth trades options and exchange-traded funds as well as equities. The firm has tripled its staff to 55 from less than 20 when it opened in 2008, while launching desks dedicated to health-care research, sales and trading, closed-end funds, and electronic trading. Overall volume handled has increased “exponentially” since 2008, according to Beth.

Agency brokers’ tradition of execution-only focus represents a potential advantage over bulge-bracket firms that typically offer trading as part of a bundled service. “Agency-model brokers have always had to work for their orders and commissions,” New Jersey’s Wszolek said. “They were trained to pay attention that every order is an important order.”

Dislocations at some bulge-bracket firms and downsizing at others have created additional competition, as displaced traders and operations personnel planted flags elsewhere. Several agency brokers that launched in recent years didn’t last, noted Fifth Third’s Hedger, himself a 25-year trading veteran.

In a world where you have fewer dollars to pay your good relationships, you’re going to focus those dollars where you can get

the most benefit. Jose Marques, global head of electronic equity trading at Deutsche Bank

Additionally, “several small research-driven brokerage firms set up shop mostly from analysts that were once employed by bulge-bracket firms,” he said. “They have been attempting to re-establish their buy-side relationships and capture some of the limited commission dollars. This seems promising, as new commission sharing arrangements have been widely adopted to pay for research from boutique research firms that do not have well-established sell-side trading operations.”

Existing brokerage firms “have begun to adapt to the new landscape and have adjusted their business model to deal with lower volumes and lower commissions,” Hedger continued. “They have been trying to find creative ways to solve some of the block trading and liquidity impediments to capture more order flow.”

For some market participants, liquidity impediments embody themselves in the form of high-frequency traders, whose ubiquity on certain trading venues can result in more friction and smaller transaction sizes. The pervasiveness of HFT has given rise to an offshoot business of sorts on Wall Street, i.e. trading against high-frequency practitioners.

“In a world where you’re competing head-to-head against the high-frequency traders, it requires a big investment in technology, including co-location and low-latency market data and market access,” said Marques of Deutsche Bank. “It requires an even bigger investment for quantitative trading, as our models have to be every bit as competitive as the high-frequency guys. That kind of investment has made it really difficult for the smaller providers to have relevant products.”

Deutsche Bank’s Autobahn trading platform offers Stealth, a ‘next-generation’ algorithm that deploys high-frequency return-seeking models to source liquidity on both dark and lit venues, while identifying short-term market signals and adapting to intraday market conditions.

Algos Prevalent

Some institutional market participants say that trading algorithms are largely commodity products, and brokers’ opportunities to differentiate themselves lie in the areas of managing often-unwieldy collections of algos, and measuring algo performance. Broker-dealers argue that algos themselves make a difference.

“Given that buy-side managers are only increasing their use of computer-driven algorithms, we’re arguably in the ‘Wild West’ phase,” said Beth of WallachBeth. “Algos have become as popular and ubiquitous as the generic apps so many of us download to our mobile devices. There are tens of dozens of mainstream algos created by an increasing number of providers, not to mention the assortment of proprietary algos created internally at various prop-trading firms.”

Beth cited a reduced risk tolerance on the part of the largest investment banks, whose proprietary trading desks have historically been the dominant source of liquidity for institutional equity managers. “Computer-based trading algorithms now drive as much as 65% of reported equities volume, more than double pre-2008,” he said.

“We’re finding that no algo is created equally, including the most basic VWAP or TWAP,” Beth continued, referring to volume-weighted and time-weighted average price mechanisms. “The most important thing today is to be able to objectively discern between the variety of algos and continuously determine performance — this is a task that inspired a cottage industry of folks who can provide an objective, independent, granular assessment.”

A market-wide reduction in average order size has afforded a competitive advantage to large broker-dealers that can coagulate internal liquidity, according to Burns at Bank of America Merrill Lynch.

“The market has been cluttered with 100- to 200-share lots; average fill size has continued to shrink,” Burns said. “Investment flow is challenged to find each other in the current market structure. Firms that have focused on their technology and have natural investment flow across their floor will continue to grab share.”

“Where I see the biggest difference is the investment in the trading infrastructure across floors, I definitely see a disparity in terms of people’s commitment towards these businesses relative to other issues,” Burns continued. “There has been some downsizing and change on the execution side. The banks that have made a commitment towards electronic execution, developing tools and venues, and furthering (indications of interest) are best positioned for growth.”

Heightened competition among sell-side providers has benefited the buy side, as the past five years have been sellers’ markets when it comes to trades, i.e. the asset managers offering their order flow are in the catbird seat. “There has been an embarrassment of riches from the buy-side perspective in terms of technology and innovation,” said Jay Fraser, managing director and head of Autobahn Americas for Deutsche Bank. “For the buy side, it has never been better, as all of us are tripping over ourselves to be the best provider. It is an arms race.”

Equity trading market share of five largest bulge-bracket broker-dealers

For a sell-side provider, “you have to be a ‘flow monster’ — you have to internalize, maximize and run a very efficient business,” Fraser said. Historically, we have focused on the top line, but now the focus is way more on the bottom line. What is the cost of doing business? Where are the operational efficiencies? How can we combine efforts to still benefit the client, while managing our business in a cost-effective way?”

The outlook for the next five years and beyond is unclear, but there is a general consensus regarding one projection: there will not be a return to pre-2008 trading levels anytime soon.

A Look Ahead

Earlier this year, McKinsey said the bulge bracket may shrink to as few as five or six as more brokers exit businesses in which they don’t have a competitive advantage. “There are more aspiring flow monsters than projected levels of flow can support,” McKinsey analysts said in a report.

Another consultancy, Woodbine Associates, recently noted that broker-dealers need to optimize internal processes and efficiency, as they can no longer rely on a rising tide to lift the boat.

“In the good times, with year-over-year volume growth, it was easy to succeed,” said Matt Samelson, principal and director of equities at Woodbine, in a statement. But “in this environment managers need to rely more heavily on business intelligence, strategic planning, personnel, and training. Many individuals who run these businesses come from specialized sales and trading backgrounds and never developed these skills.”

Regulation is expected to be a key influence on broker-dealers’ business, especially after some rules that are still developing are made final and implemented. One area in focus is what rules the U.S. Securities and Exchange Commission may apply toward stock exchanges, which increasingly compete with broker-dealers, and which under current rules are partly self-regulating.

“Regulation is going to have a big bearing on the next five years,” said Burns of BoAML. “There is certainly increased regulation and oversight on the exchanges. The question is how do we better regulate the exchanges — how do we control order types and deal with their (self-regulatory organization) status? I think that dark books will be continually evaluated by regulators.”

More broadly, competition is expected to remain keen at the very least, if not intensify. Whether the bulge bracket or agency model gains the upper hand, there will always be order flow for individual broker-dealers who excel at the business.

“There should certainly be enough flow to go around to those who can add true value, whether via algos exclusively or using algos with high-touch oversight courtesy of humans who understand how to measure performance,” said Beth of WallachBeth.

Added Marques of Deutsche Bank, “I think you’re going to see the complexity and cost of trading continue to increase. You will also see the true scale players continue to invest and keep products current, and the buy side will naturally gravitate towards the better providers.”

“There is plenty of order flow around for brokers who have differentiated product and who are relevant to their clients,” Marques concluded. “If you are good at what you do and relevant to your client by creating value, you are going to be just fine.”

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.