01.26.2026

Tokenized treasuries have reached more than $10bn, according to data provider RWA.xyz, but this is still only a tiny portion of the trillions of dollars of U.S. treasuries that could be used more efficiently onchain as collateral.

BREAKING: Tokenized Treasuries has surpassed $10B

Circle's USYC deployed on BNB Chain tipped the asset class into next stage of scale pic.twitter.com/sqb6Zo6PPC

— RWA.xyz (@RWA_xyz) January 23, 2026

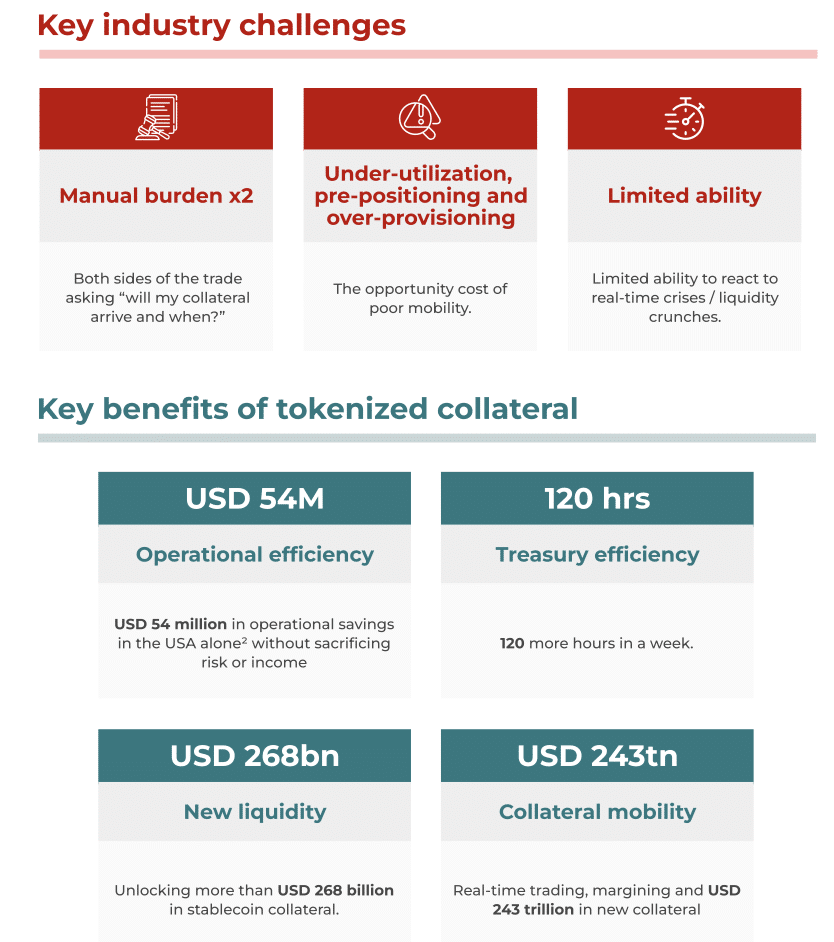

More that half, 58%, of market participants currently face challenges in managing their collateral and margining according to a survey from consultancy The Value Exchange in partnership with Digital Asset, who provide enterprise blockchain infrastructure with built-in privacy.

The study, Treasuries On-Chain: An industry case for change, said collateral flows involve a manual, risk-prone post-trade environment that only operates within standard banking hours. Moving more treasuries onchain, making it faster and easier to move collateral 24/7 could generate $54m in just operational savings in the U.S, without sacrificing risk or income, according to the report.

To highlight the potential of using onchain collateral, financial institutions took part in two sets of short-term onchain repo transactions that involved U.S. Treasury bills versus stablecoins on the Canton Network, Digital Assets’ blockchain for financial institutions which has built-in privacy controls, in 2025.

Source: Value Exchange

In January this year a third set of onchain repo transactions took place on the Canton Network. For the first time, intraday repos were conducted cross-border using multiple currencies and multiple asset classes, including European government bonds, U.S. Treasuries, euro cash, and U.S. Dollar cash. Financial market infrastructures London Stock Exchange Group, Euroclear and Euronext were also involved.

Digital Asset said: “This latest set of transactions marks a major milestone for the industry working group, spanning cross-border intraday repo activity across multiple assets and currencies and leveraging tokenized deposits at LSEG Digital Settlement House (LSEG DiSH) to provide greater liquidity options.”

LSEG DiSH allows users to instantaneously transfer tokenized commercial bank deposits to any member of the DiSH network, which is transferable 24/7 in real time, without requiring users to have relationships with every bank on the DiSH network. The working group will continue to collaborate on more onchain financing initiatives in 2026.

David Leblanche, Euronext

David Leblache, head of innovation & AI products at Euronext, said in a statement: “This initiative reflects the industry’s collective effort to explore how tokenization and on-chain infrastructure can enhance collateral.”

Kelly Mathieson, chief business development officer at Digital Asset, told Markets Media that the model will be different for each jurisdiction, but traditional trusted financial market infrastructures can maintain the register so investors get an onchain version of the same asset. Canton is continuing to have constructive conversations with entities in Japan and Canada for government bonds.

She said: “These are not not pilots or proofs of concept, they are real transactions. They may start with a smaller notional value but we are seeing calculations on increased balance sheet efficiency.”

For example, one active market maker with a balance sheet of between $15bn and $17bn estimated they will gain about $10m to $12m per year from reduced cash buffers and lower collateral haircuts, as they can put financing in place after tradition traditional banking hours. Another hedge fund-type organization with a $50bn balance sheet calculated an impact of $26m per year.

Mathieson added that one of the themes for this year is real use case with real assets, real institutions, and real capital efficiencies at scale.

“About 90% of the benefit comes from freeing trapped cash and immobilized collateral rather than headcount reduction,” she said. “Lower funding costs means higher trading capacity, reduced stress on liquidity and more ability to act.”

DTCC

In December last year the Depository Trust & Clearing Corporation, the U.S. post-trade infrastructure, said in a statement it had partnered with Canton. For the first time, DTCC plans to enable a subset of custodied U.S. Treasury securities to be minted on the blockchain.

Mathieson said: “It is critically important that the solution for U.S. Treasuries held at the DTC. With the DTCC the assets are not a wrapper, a digital twin or a trust certificate.”

Frank La Salla, DTCC

DTCC said they are working towards a minimum viable product in a controlled production environment during the first half of 2026, with plans to increase the size and scope of the project in the months that follow, based on client interest.

Frank LaSalla, chief executive of DTCC, said in statement: “This collaboration creates a roadmap to bring real-world, high-value tokenization use cases to market, starting with U.S. Treasury securities and eventually expanding to a broad spectrum of DTC-eligible assets across network providers.”

JPM Coin

In January this year Digital Asset and Kinexys by J.P. Morgan, the bank’s blockchain business unit, said in a statement that they intend to collaborate on the native issuance the bank’s deposit token product, JPM Coin on the Canton Network.

JPM Coin is the first bank-issued U.S. dollar-denominated deposit token and provides institutional clients with the ability to make payments using a digital representation of J.P. Morgan deposits on a public distributed ledger. Mathieson said this will unlock a host on chain financing and transactions.

Naveen Mallela, global co-Head of Kinexys by J.P. Morgan, said in a statement: “JPM Coin delivers the security of bank-issued deposits and settlement, combined with the speed and innovation of 24/7, near real-time blockchain transactions. In bringing JPM Coin on to Canton, we can further increase efficiency and unlock liquidity.”

Growth

Mathieson said: “I think that there are a number of themes that have new fire underneath them. Aa result there is a level of traction, focus, development, commercial discussions and launches that we have always wanted to happen.”

Kelly Mathieson, Digital Asset

There is demand from traditional finance (tradFi) to bring high-quality, liquid onchain in a usable form to improve collateral mobility and facilitate intra-day financing. In addition, there is a growing demand from the crypto market from newer exchanges and CCPs for onchain assets and infrastructure.

In addition, applications are being created to use onchain assets.

“It’s like one hand clapping to have these assets in the onchain ecosystem without the applications to be able to do something with them,” she added. “By the time we get to the end of the year it will not tradFi or crypto, but something new that is in between.”

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

The combinaton creates a fully integrated front-to-back ecosystem spanning the fixed income market.

-

The global bond market has long been one of finance’s most fragmented and opaque areas.

-

HSBC and LSEG have signed an MoU to develop connectivity to support investor access.

-

This deepens the integration of Chinese assets into the international financial infrastructure.

-

Clients will be able to access primary markets through partners.