07.07.2026

MarketAxess, the operator of a fixed-income electronic trading platform, is developing an ecosystem to give clients access to primary markets and the ability to trade immediately in the secondary market.

Gareth Coltman, MarketAxess

Gareth Coltman, head of products, EMEA & APAC at MarketAxess, told Markets Media that developing a new issue ecosystem is a big area for the firm is . He stressed that MarketAxess is not building out a primary market, but an ecosystem where clients can access new issues through partners.

In February this year MarketAxess and capital markets platform DirectBooks agreed to provide mutual clients with streamlined access to DirectBooks’ primary issuance information and workflow tools. The integration allows MarketAxess clients to review DirectBooks deal announcements, submit indications of interest, and receive allocation messages from syndicate desks, providing increased speed, accuracy and transparency across the deal lifecycle.

Historically, the new issue workflow for clients has been fragmented and clunky, presenting communication challenges as well as difficulties moving from primary to secondary markets, according to Coltman.

“Clients will be able to use our connectivity to access primary markets and integrate order flow with their own systems,” he added.

Source: MarketAxess

In addition, MarketAxess will provide clients with data and a view of comparable bonds if clients are not able to get the allocation they want in the primary issue.

Block trading

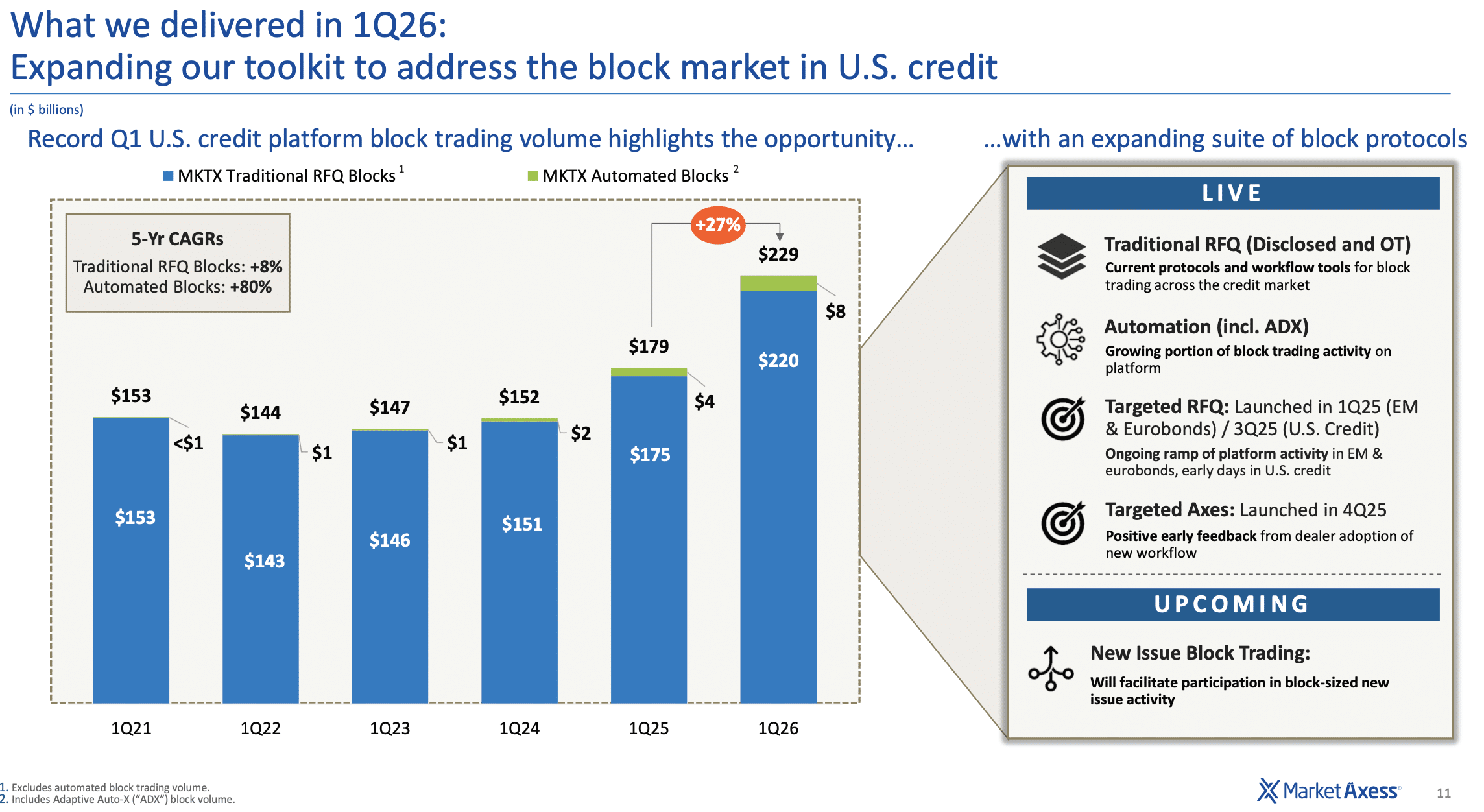

MarketAxess is also focused on block trading as clients are becoming more confident using automation for larger sizes and across the liquidity spectrum according to Coltman.

“They also want technology to help with sensitive, or very large trades, which they currently manage manually,” he added. “This process is becoming more data-driven and electronic.”

For example Targeted Axes, which enables dealers to electronically send firm, disclosed axes to a defined group of buy-side clients, went live in U.S. credit and will shortly be live in Europe to trade both U.S. credit and Eurobonds. Traditionally sell-side traders put a specific axe in front of the clients by either calling or sending individual messages.

Coltman said some very large asset managers are adopting automation to trade large blocks and are using Adaptive Auto-X extensively. Adaptive Auto-X is MarketAxess’ multi-protocol automated execution solution.

He added: “This allows them to respond to opportunities automatically for both price-taking and price-making workflows.”

Source: MarketAxess

Generative AI

MarketAxess is also beginning to explore the potential of generative AI by allowing clients to use a natural language interface to query its data.

Coltman said: “Clients want to get decision support pre-trade but it’s currently a manual process.”

He argued that the data MarketAxess provides to clients creates an advantage for them in terms of pricing or liquidity signals and workflow analytics. For example, MarketAxess has rolled out a tool which allows clients to use either a rule set or an AI model to suggest specific dealers with whom they could interact.

“Another focus is exploring how we can make generative AI more helpful and useful in client workflows to let them interact with our rich dataset in a user-friendly and creative way in pre-trade, such as asking for suggestions of comparable bonds,” he added.

Coltman sees a future where clients will have the ability to automatically aggress a price level advertised by a dealer based on the rule set within the Auto-X engine.

“We have been a real pioneer in AI-driven signals for pricing and liquidity signals for many years,” he said. “People use CP+ like a top-of-book price feed but in reality we are predicting the next traded price using machine learning.”

CP+ is the firm’s proprietary algorithmic pricing engine for corporate bonds. Coltman said CP+ has been through multiple market crises and is very robust.

“I think our price, scale and liquidity models are seen as a market standard in credit, with a large portion of the market using them directly but also consuming them into their own in-house systems,” he added.

MarketAxess wants to give clients pre-trade data and analytics, including dealer suggestions, that allows them to interact with liquidity using whatever protocol makes the most sense for them such as targeted RFQs or trading bilaterally.

Connectivity

In May this year MarketAxess integrated with Moment, the AI platform for investment management. Moment’s platform seamlessly integrates retail order-driven markets from large wealth managers and registered investment advisors (RIAs)with the traditional institutional RFQ market, enabling access to institutional liquidity.

Chris Concannon, MarketAxess

Chris Concannon, chief executive of MarketAxess, said in a statement that institutional investors in fixed income have historically benefitted from access to deeper liquidity and higher quality pricing. Concannon said: “By partnering with Moment, we are extending that institutional liquidity to retail investors, helping improve execution quality and outcomes for end investors.

In 2024 MarketAxess had connected its liquidity network to ICE Bonds, part of Intercontinental Exchange, to bring greater efficiency and access to deeper liquidity in fixed income markets to the institutional and wealth management spaces.

Coltman argued that key piece of value for clients is connectivity with thousands of fixed income market participants as buy-side clients can access a broader range of workflows and liquidity through a single access point.

“We continue to look for opportunities to create connectivity, such as our partnerships with Moment, ICE and DirectBooks,” he added. “Moment has a retail client base and a really interesting business model around fractional order flow, which we bring into our ecosystem as meaningful additional liquidity.”

Automation

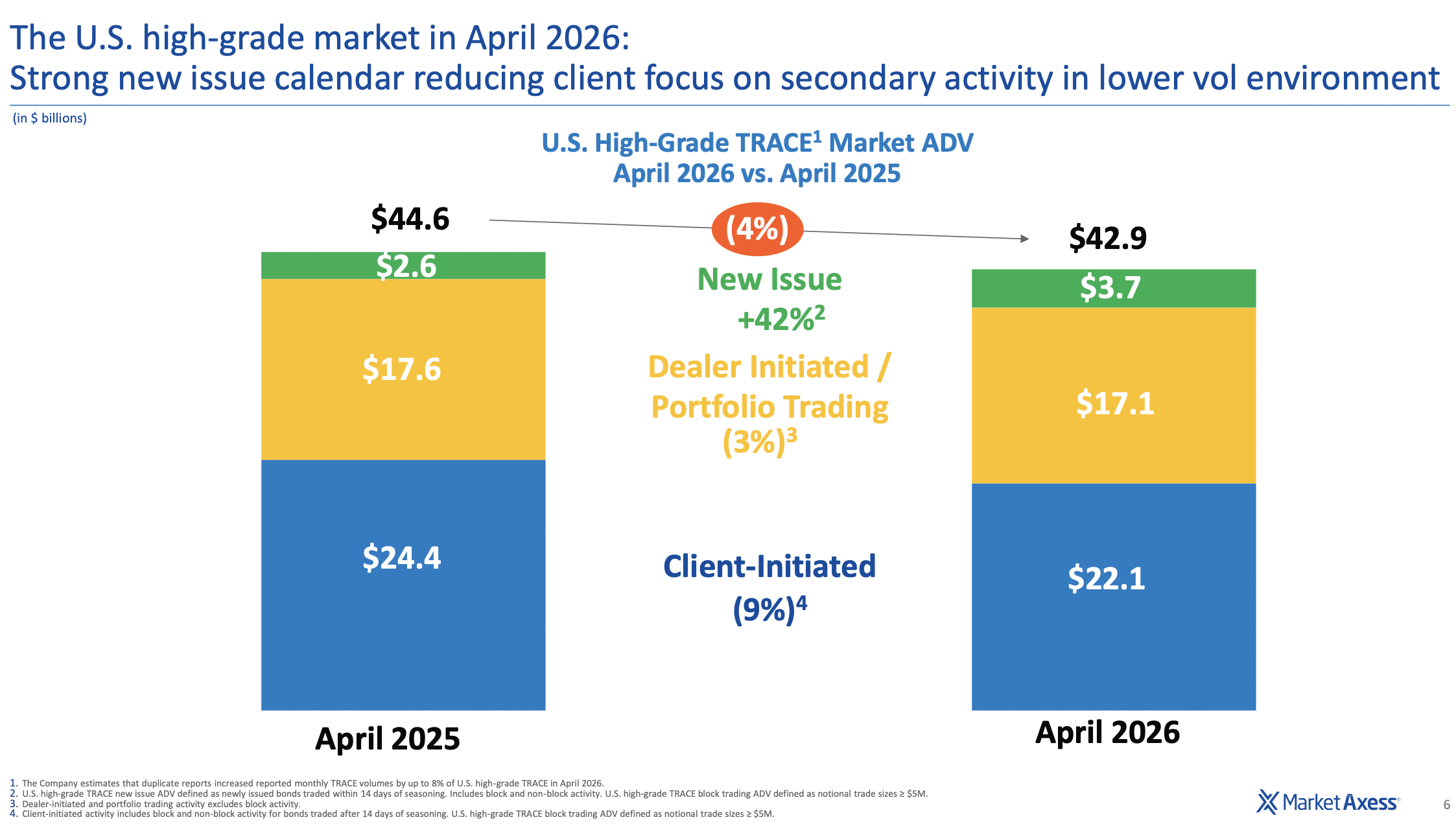

For the first quarter of this year, MarketAxess reported record levels of trading average daily volume across most credit products with strong growth in total rates average daily volume.

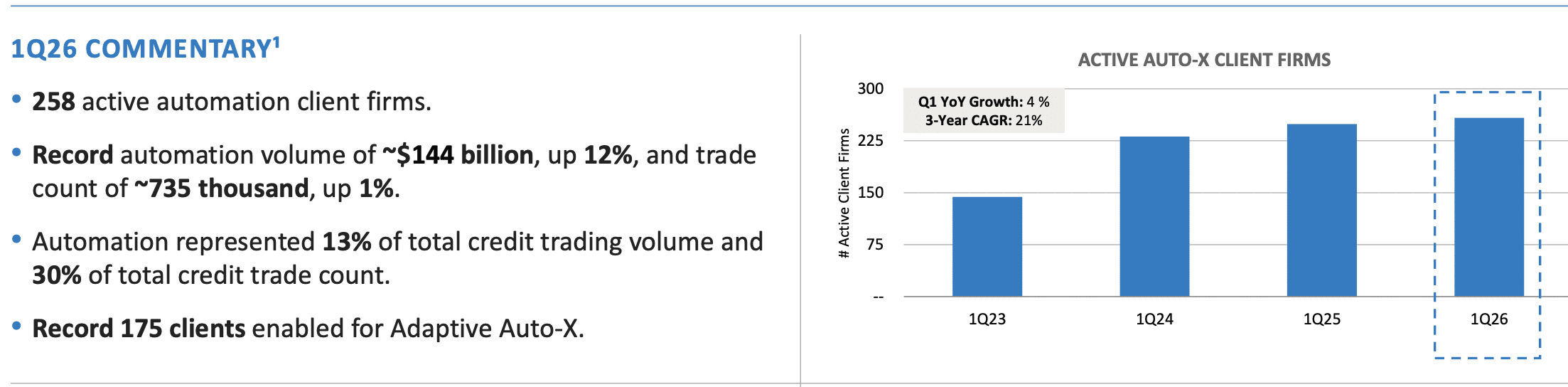

During that period MarketAxess had 258 active automation client firms and a record 175 clients enabled for Adaptive Auto-X. Automation volume was a record $144bn, which represented 13% of total credit trading volume.

Source: MarketAxess

Coltman said automation can be applied to any protocol and any workflow where there is good data and that both sides of the street have an appetite to extend automation and create efficiency across the board.

“We help clients maximize efficiency, regardless of how they want to trade or which protocol they use,” he added. “Clients can use automation to automate their regular price-taking RFQ workflow, rest an order in the system, or use algos to decide how an order interacts with the market.”

Traditionally automation has been used for RFQ price taking, but Coltman said clients can now add smart order routing logic to take advantage of opportunities in the market and decrease execution costs.

MarketAxess has also rolled out algos that clients can use to trade U.S. Treasuries.

Coltman said: “Clients are willing to rest a large block on the platform and have an algo interact with the order book and trade that over time, which has worked well in markets such as FX or equities where there is continuous liquidity.”

There have also been discussions with clients around automating portfolio trading to create more efficiency. Portfolio trading has been quite a manual and time-consuming process and typically takes from minutes to hours for pre-trade analysis prior to final execution, according to Coltman.

“I think we have a secret sauce and can offer clients an automation toolkit that creates more value for clients than they can get anywhere else through access to a broad set of liquidity, including outside MarketAxess, and the right data to enable good decision making,” he added.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

This is the most significant update to Climate Bonds' taxonomy in years.

-

New launches extend the range to short term & global corporate bond strategies.

-

They will look for additional opportunities to collaborate on behalf of shared clients.