02.09.2026

Apollo Global Management, the alternative asset manager, is going to expand origination in Europe and Asia Pacific and is also focused on growing ecosystem strategies, such as its new sports financing business.

Jim Zelter, president of Apollo Global Management, said on the results call on 9 February 2026 that the manager originated more than $305bn of assets in 2025, up nearly 40% from the prior year. Approximately $280bn of the origination was debt, with about 80% in investment grade. He highlighted that Apollo identified sponsors as an opportunity in 2022 and origination volume in this segment was nearly 80bn in 2025, quadrupling in four years. Zelter stressed that Apollo is focused on quality, as Apollo has already shown an ability to originate in scale.

Jim Zelter, Apollo

Out of the total origination, $245bn was from North America, $40bn in Europe and the remainder in Asia. Zelter said: “We are taking this strategy global and we are going to make sure that Europe and Asia Pacific have the same tools, the same partnerships and the same platforms.”

Apollo said in statement that Diego De Giorgi, group chief financial officer of Standard Chartered, will join the firm as a partner and head of EMEA. De Giorgi will succeed Rob Seminara, who will remain in the region to support a transition before assuming a new, global role later this year.

Another part of the growth strategy involves ecosystem activities such as Apollo Sports Capital. In September 2025 Apollo said it was launching a new investment business to provide capital solutions across global sports and live events. Apollo Sports Capital invests predominantly in credit and hybrid opportunities in sports, spanning franchises, leagues, venues, media and events.

“I suspect we will see a handful more of those ecosystem strategies where we can be completely relevant in terms of cost of capital and the toolbox for companies in that ecosystem,” said Zelter.

He continued that many institutions are having conversations about Apollo Sports Capital, as they try to find opportunities outside the traditional asset classes.

Marc Rowan, chairman and chief executive of Apollo Global Management, said on the call that the sports capital business is a good example of Apollo preferring to build, rather than buy, a new business. He said: “In addition to deploying about $6bn in the Sports Capital fund, I believe this ecosystem will generate $30 to $50bn of origination opportunities.”

Rowan continued that the firm is changing from serving one market of institutional alternatives portfolios to serving six markets. The other markets include individuals, insurance, debt and equity buckets for institutional clients, traditional asset managers and the 401(k) market for U.S pension schemes. He expected each of these markets to be roughly the same size as Apollo’s original market but warned that they require different products, structures, access points and investments in technology.

Apollo had more than $80bn of inflows in 2025 and Rowan expects approximately $85bn of inflows in 2026, with more than $5bn of inflows from markets that the firm was not in 18 months ago.

Zelter said: “If you think about where our business is going it’s all about origination, having the product and then building the capabilities to serve five markets that we have never served before as an industry.”

Retirement

“The global retirement crisis is coming much more into view,” added Rowan. “The demand for retirement income has never been higher.”

Marc Rowan, Apollo

Rowan believes that the next leg of the retirement business is not the product set that exists today, so the industry needs to create products for retirees that are simpler and easier to deliver.

On 9 February 2026 Apollo said in a statement that it had formed a partnership with Schroders, the UK assets manager, to develop wealth and retirement investment solutions. The partnership combines Schroders’ active management in public markets and specialist capabilities across private markets, through Schroders Capital, with Apollo’s private markets platform. Rowan added that he expects this to grow into a multi-billion dollar partnership.

The firm said key initiatives include accelerating and deepening the firms’ offering in the UK wealth market, with the first product expected to launch this year. In addition, Schroders will have the opportunity to allocate to Apollo from certain existing client portfolios.

In the US, a Collective Investment Trust for the defined contribution pension market is being prepared for launch in the second quarter of this year. Zelter said the global retiree wave continues to build, and argued that Apollo has a competitive advantage.

Source: Apollo

“We did not get here by accident,” added Zelter. “Years of hard work have established us as the industry leader with multiple competitive advantages allowing us to serve retirees at an increasing scale overall.”

Rowan said Apollo is open architecture, so the firm can form a number of partnerships, and also supplies products to a number of traditional asset managers. He added: “I think we are going to continue to see partnerships blossom.”

He believes traditional asset managers could be the largest opportunity in the retirement space but the big volumes will not come though until there is more regulatory clarity in the U.S.

Fund performance

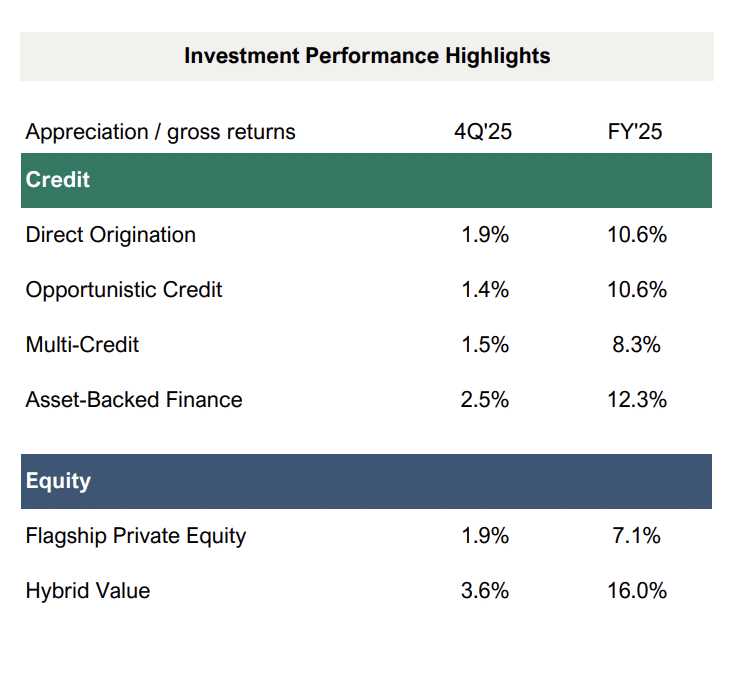

There have been concerns that there are problems in the private credit market and Rowan highlighted Apollo’s “strong” investment performance. He added that all buckets of credit are up between 8% to 12% and fund 10, Apollo’s most recent vintage fund was up between 23% and 22%.

The share price of many software companies has also recently fallen. Apollo’s private equity firm business has zero software exposure, according to Rowan, and half the exposure of peers in the Apollo Debt Solutions BCD (ADS) fund. He described the market overreaction to software as “extreme.” He added that ADS, Apollo’s largest private markets direct lending vehicle has more than $25bn in assets and returned approximately 8% in 2025 with low leverage and being at the top of the capital structure.

“I assure you we are on offense, and software will be a very attractive sector, albeit not at the valuation levels and with the underwriting that has been done previously,” said Rowan.

Source: Apollo

Rowan continued that Apollo has built a $4bn position in cash treasuries and agencies which gives the firm significant firepower to deploy with plenty of flexibility.

Financials

Rowan described the business as “firing on all cylinders” on the results call on 9 February 2026.

“2025 highlights include record origination activity exceeding $300 billion and inflows of more than $225 billion, driving record fee and spread related earnings,” he added.

For the full year 2025 , Apollo generated record combined fee-related earnings and spread-related earnings of $5.9bn which drove adjusted debt income of $5.2bn, up 14% year-over-year.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

The PMAX fund platform has removed the accredited investor requirement & cut minimum investment amounts.

-

The alternatives manager has also launched market making for private markets.

-

The U.S. Department of Labor’s Employee Benefits Security Administration issued the proposed regulation.

-

The joint venture will develop India-focused alternatives capabilities.

-

The alternatives manager said only Leon Black, who left in 2021, had a relationship with Epstein.