04.14.2026

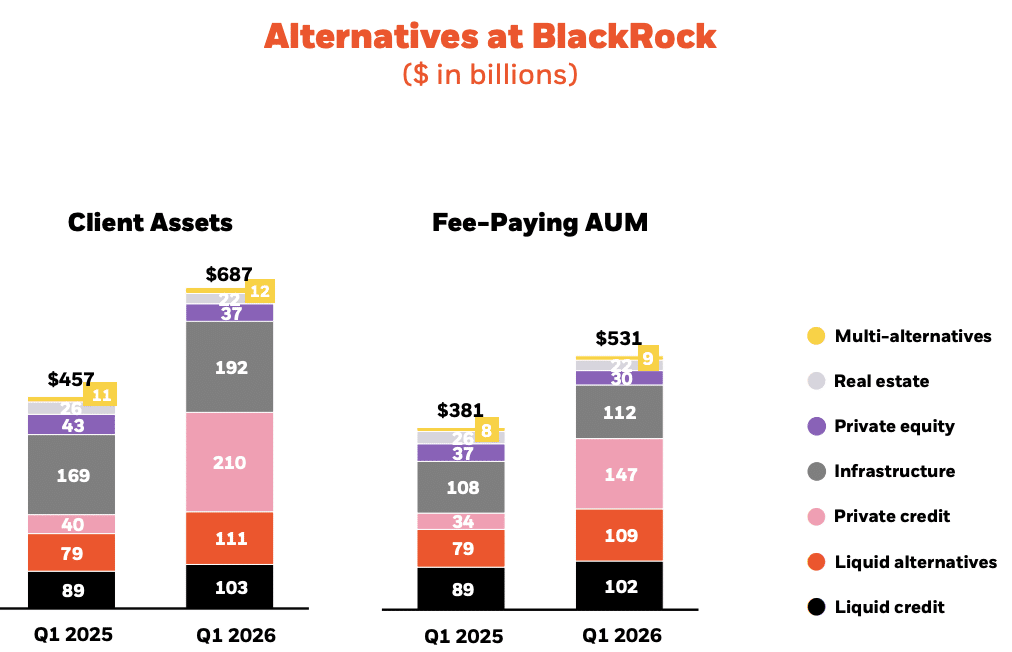

BlackRock reported that it had net inflows of $9bn in private markets in the first quarter of 2026, led by private credit and infrastructure, amid investors across the industry asking to withdraw their capital due to concerns about potential losses in private credit.

Larry Fink, chairman and chief executive of BlackRock, spoke about private credit on the results call for the first quarter of 2026 on 14 April. He said: “There’s been a lot of attention on private credit, but the headlines do not reflect what clients are telling us, what our portfolio data shows, or where we see the market going.”

He argued that the headlines relate to wealth vehicles such as business development companies (BDCs) and interval funds, which make up approximately $550bn in assets under management, or about 25% of the $2.2 trillion private credit industry. In contrast, Fink said institutional demand for private credit is accelerating, particularly from insurance companies. For example, in the quarter BlackRock signed a multi-billion dollar rotation into high-grade private credit from an existing insurance client.

Larry Fink, BlackRock

“Institutions are increasing allocations to private credit as wider spreads are enhancing potential returns and defaults, while normalizing, are still within historical standards,” added Fink.

Fink expects much more dispersion in performance among private credit managers and he said that is an environment where BlackRock likes to compete.

In order to expand its private market capabilities, BlackRock completed its acquisition of private credit manager HPS Investment Partners on 1 July 2025. The asset manager also acquired ElmTree Funds, a leader in the commercial net-lease sector, last year and Global Infrastructure Partners (GIP) in 2024.

“We believe that HPS’s strong underwriting discipline and its proactive risk management will compare favorably, and hopefully result in differentiated returns and share gains,” Fink added.

Martin Small, chief financial officer at BlackRock, said on the results call that retail net inflows of $15bn reflected continued strength in the asset manager’s systematic liquid alternatives, active fixed income and evergreen private markets offerings. He said: “Subscriptions for HPS’ flagship non-traded BDC continue with approximately $150m of subscriptions for the April window.”

The HPS Corporate Lending Fund, a $26bn non-traded, semi-liquid BDC is the manager’s primary retail private credit product. Small believes that some of the private credit tumult is an opportunity for Blackrock to take share, particularly in private markets across wealth platforms where clients want a more whole portfolio relationship.

“We actually think some of this shakeout in private credit is good for our organic base fee growth profile,” said Small.

Source: BlackRock

Fink continued that private markets are a large and growing part of capital markets and clients are turning to BlackRock to help them understand what this means for their portfolios and beneficiaries.

“We’re engaged with clients across every channel, geography and asset class,” added Fink. “Many of these conversations would not have been possible five years ago, because the platform we have built did not exist.”

Fink said the the combination of GIP and HPS with Blackrock is surpassing the “highest expectations.” GIP closed its fifth fund above its $25bn target, and the majority is already committed.

“HPS and GIP supercharged our origination capabilities and allowed us to be more selective while still actively deploying capital at scale,” said Fink. “These businesses are accelerating.”

In addition, Fink believes that the growth in private credit is a “meaningful” opportunity for Aladdin, BlackRock’s technology platform, because the asset class has scaled rapidly, but the risk management infrastructure has not kept pace. BlackRock is positioning Aladdin to be the language of private credit portfolios for transparency and risk analytics.

Retirement

Fink said much of BlackRock’s work is focused on making retirement investing more accessible and this is resonating in every conversation that he has with governments.

“Our platform spans defined benefit and defined contribution and brings together public and private markets, active and index, and technology at a global scale,” he said. “That combination differentiates us in the U.S.”

The U.S.Labor Department proposed a rule in March this year that would allow 401(k) plan sponsors to include private credit and other alternative assets in their pensions through reducing the risk of litigation. Fink described the proposed rule as a major development towards a framework to include private assets and target date funds in retirement plans, and he believes Blackrock will be at the forefront of this opportunity. For example, the asset manager has $600bn in assets in LifePath Target Date funds, with the business having $15bn in inflows in the first quarter.

He highlighted that BlackRock’s wealth platform spans over $1 trillion in assets with global distribution across tens of thousands of financial advisors, and solutions from models to separately managed accounts, ETFs and private markets. In addition, Aladdin sits on the desktop of financial advisors.

ETFs

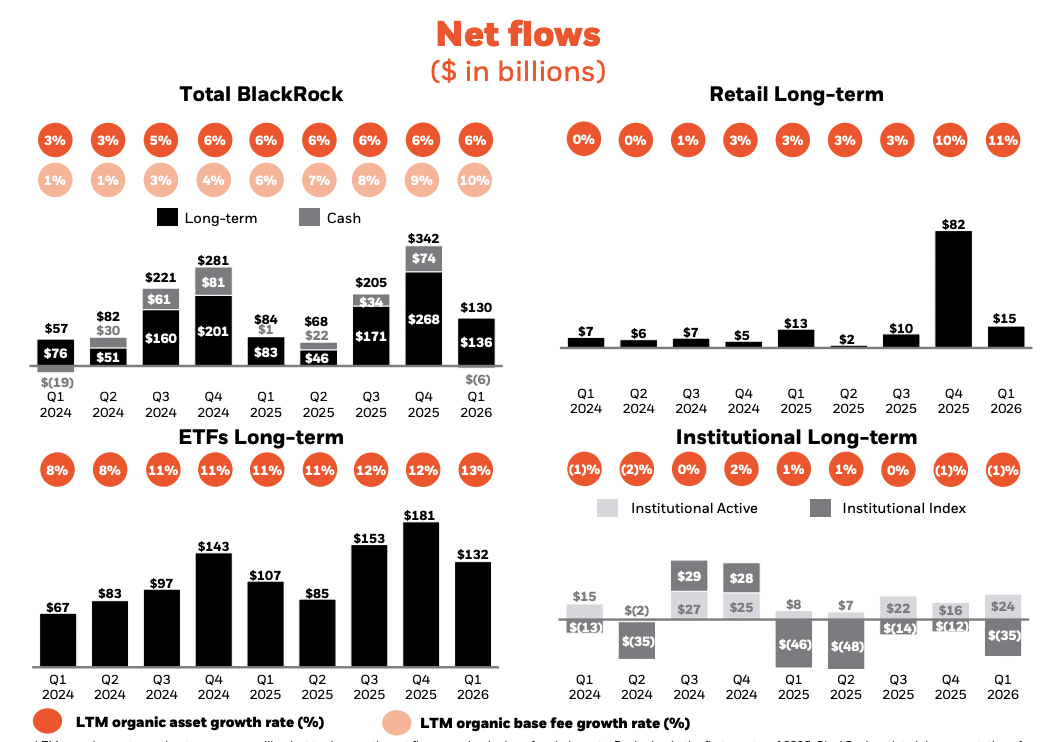

iShares, the ETF franchise, reported record first quarter net inflows of $132bn. Fink said iShares doubled net new base fees compared to a year ago, as clients rotated to international and precision exposures.

Source: BlackRock

Small added that the record net inflows were led by $41bn into bond index ETFs, $39bn into precision exposures, $32bn into core equity ETFs and $19bn into active ETFs.

“Client demand for international diversification presents a meaningful upside for BlackRock, particularly in areas like emerging markets and precision reallocations,” said Small.

Fink argued that iShares is differentiated because it indexes “virtually every slice” of global equities and bond markets, from broad benchmarks to emerging markets and single country precision exposures, which drove record inflows.

“Our active ETF platform has grown four times in the last two years to more than $110bn,” Fink added. “We believe that active ETFs can generate revenue of $500m, or greater, by 2030 and we are already more than halfway there.”

Management confirmed that BlackRock has filed a registration statement with the U.S. Securities and Exchange Commission to launch an ETF on the Nasdaq 100 index, the IQQ, which would be rival to Invesco’s QQQ ETF on the same index. Small said the firm could not discuss the fund due to regulatory filing restrictions, but highlighted that BlackRock is already the largest manager of Nasdaq 100 ETFs outside the U.S. with $25bn across Europe, Canada and Hong Kong.

Martin Small, BlackRock

“We also have the Nasdaq top 30 and next 70 index ETFs, as well as the Nasdaq premium income ETF, and IQQ is similarly trying to facilitate access to one of the most widely tracked indexes,” he added. “We are differentiated at BlackRock because we have two distinct global ETF ranges in the U.S. and Europe.”

Net inflows at iShares contributed to total net inflows for BlackRock of $130bn in the first quarter of 2026 , which was also boosted by net inflows into active equities and private markets.

This was highest first quarter in five years and drove 8% organic base fee growth, according to Fink. Over the last twelve months, net new assets were $744bn which BlackRock said was broad-based and driven by private markets, ETFs, and systematic active strategies.

Fink said the asset manager delivered one of the strongest starts to a year in its history. Small added that revenue, operating income and earnings per share grew double digits in the first quarter.

First quarter revenue of $6.7bn increased 27% year-over-year, which BlackRock said was due to the positive impact of markets, organic base fee growth, fees related to the HPS acquisition, and higher technology services and subscription revenue.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

Snyder had an unconventional route to founding and selling the crypto ETP issuer.

-

The transaction with Trian and General Catalyst is expected to close on 30 June 2026.

-

ETF product innovation has collapsed the time taken to incorporate IPOs.

-

The business is working with Apollo, Franklin Templeton and J.P. Morgan Asset Management.

-

Mirae Asset is the first manager in Asia to bring its existing ETF exposure onchain.