06.02.2026

Citi: Tokenized Asset Market to Reach $5.5 trillion by 2030

06.02.2026

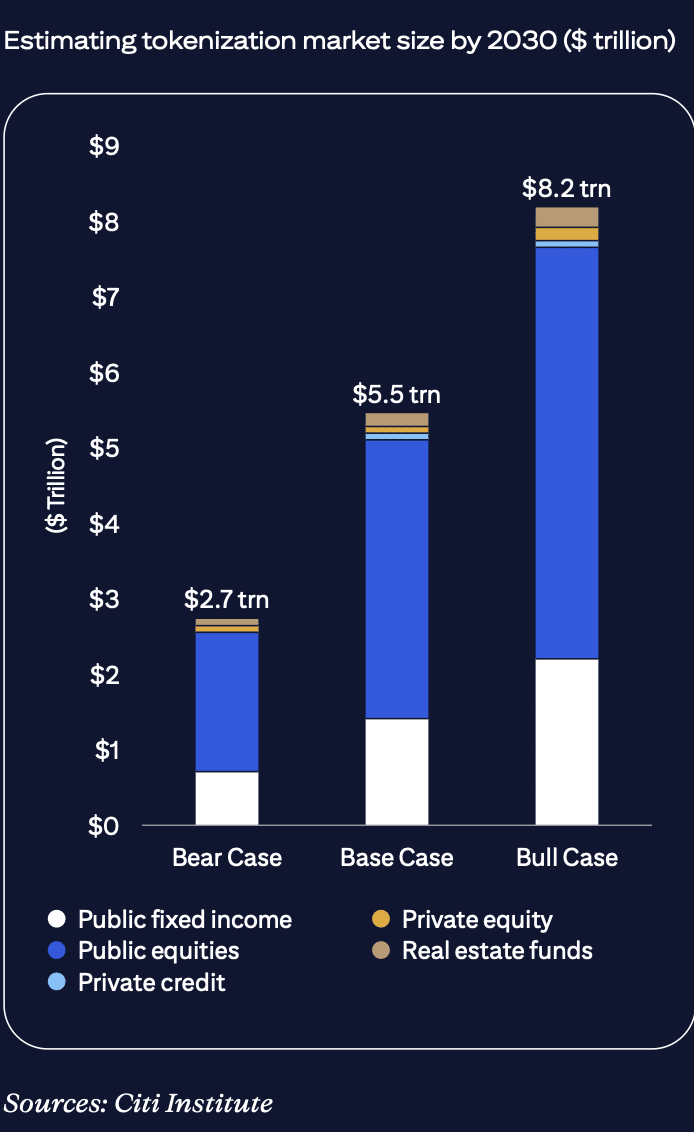

Citi Institute has estimated that the global tokenized asset market will reach $5.5 trillion by 2030, compared to approximately $17bn.

In a report, Tokenization 2030: Wall Street On-Chain, Citi Institute said $5.5 trillion by 2030 is its base case scenario, with a bear case of $2.7 trillion and a bull case of $8.2 trillion.

“Growth is expected to be led by public market securities – particularly U.S. equities and treasuries – rather than private markets, where adoption remains early-stage and structurally constrained,” added Citi.

Source: Citi

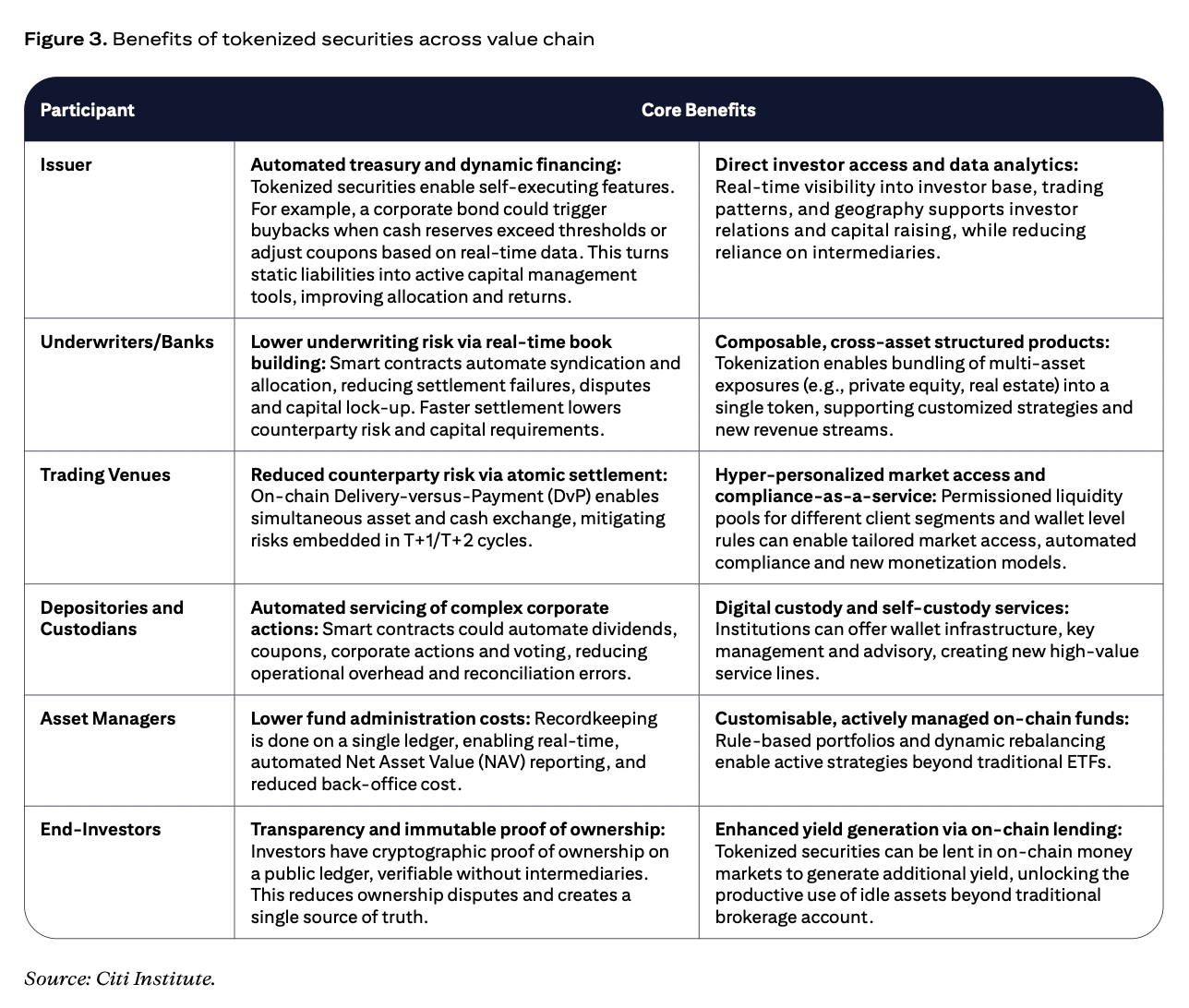

The report highlighted three forces underpinning this shift. The first is that traditional financial market infrastructure providers, including the DTCC, New York Stock Exchange and Nasdaq, are integrating tokenization into core issuance, trading and settlement workflows.

Second, the growth of regulated onchain money, including stablecoins and tokenized deposits, has been a key catalyst by providing onchain settlement. The report said: “This has been a key constraint of earlier tokenization efforts. Digital asset market infrastructure is also evolving, with advances in custody, compliance, and interoperability.”

Finally, regulatory clarity is improving across key jurisdictions. For example, the U.S. Clarity Act for digital asset market structure is moving through its approval process after being passed by the Senate finance committee.

Citi highlighted that it does not expect a sudden flip from traditional markets to fully tokenized ones as institutions will want to integrate issuance, trading and settlement at scale within regulated frameworks and existing client relationships. The value of scaling will depend on interoperability, common standards, regulatory alignment and coordination across a complex ecosystem, which will take time.

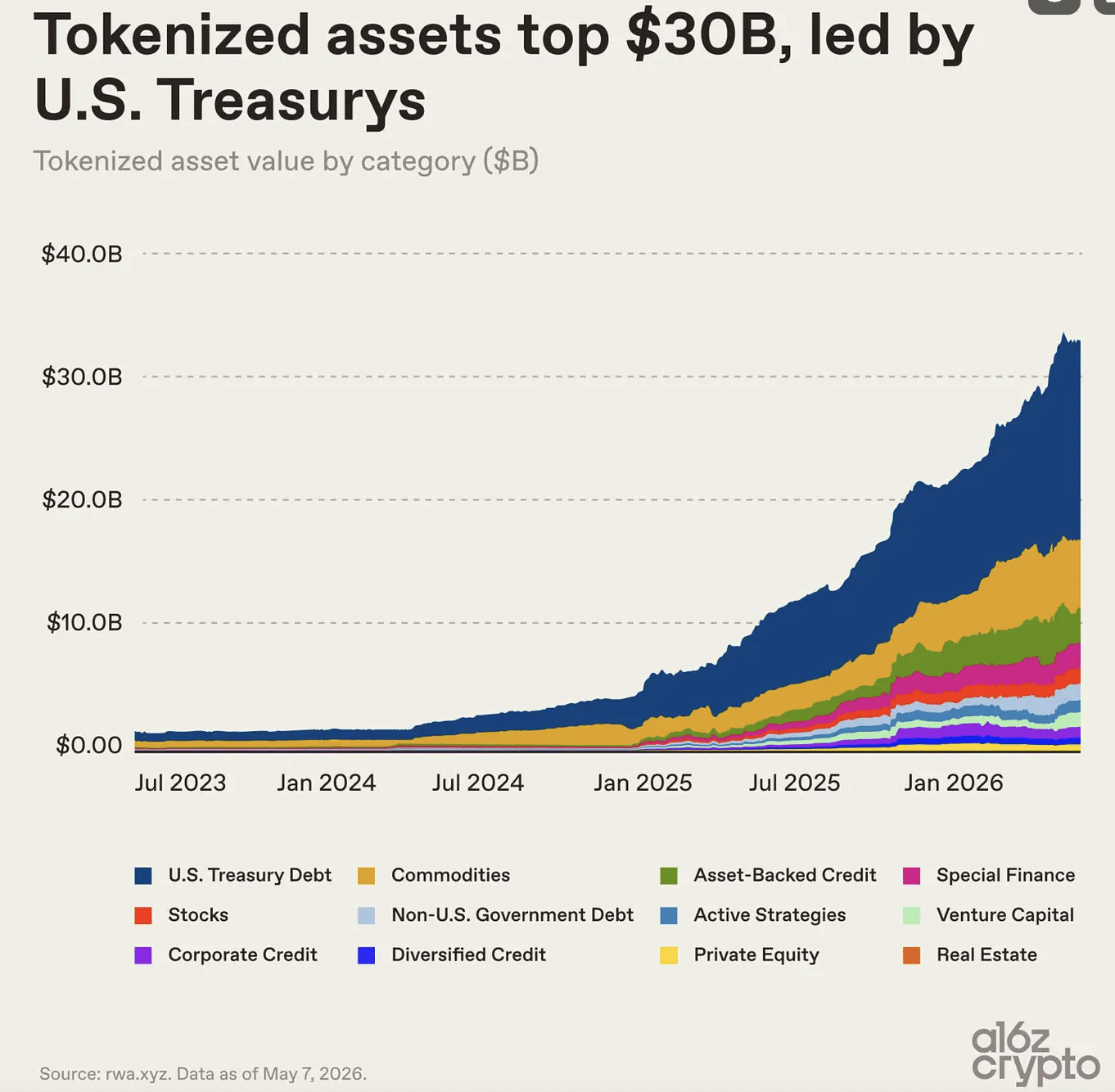

Venture capital firm, a16z crypto, said in a blog that tokenized assets crossed $30bn in April this year. They have since stayed above that level at nearly $34bn, compared to less than $3bn in the middle of 2024.

a16z crypto highlighted that not all tokenized assets are equally onchain. The firm said the largest tokenized categories, Treasurys and gold, were primarily designed to make familiar assets easier to hold and transfer onchain without fundamentally changing how they behave.

Source: a16z

“Much of what gets called “tokenization” today is actually closer to digitization: moving records onto blockchains without unlocking composability,” said the blog. “Many of these tokenized assets function as little more than digital receipts representing claims on assets that are still primarily managed through offchain ledgers and intermediaries.”

Composability enables permissionless innovation and fluid coordination across decentralized finance (DeFI) protocols. a16z crypto argued that the infrastructure for composability exists but the deeper integrations are just beginning.

Source: Citi

Asset managers

In the Citi report Blue Macellari, head of digital assets strategy at asset manager T. Rowe Price compared the transition to tokenization with the E-ZPass tollbooth technology, which did not move to full automation overnight.

“Parallel systems run first, the road got wider with lanes for automated and legacy flows, adding cost and complexity before convergence,” said Macellari. “The key question is how quickly can we reach the automated end state?”

Blue Macellari, T Rowe Price

Macallari continued that one of the most interesting use cases of tokenization for a large, diversified asset manager is the automation of multi-asset and target-date funds, as the “onerous” workflow of rebalancing and creating these complex products can be streamlined.

Half of asset managers have introduced some form of tokenization, according to a survey from Apex Group, the fund and asset servicer, in partnership with Mergermarket. The survey found that 17% of asset managers have broadly deployed tokenization and 33% are deploying it with limited use. The survey covered 100 senior executives across asset and fund managers globally.

Among firms with more than $5bn in assets under management, 55% described tokenization as very important to their business strategy, with a further 9% identifying it as a top priority. Tom Bennett, global head of fintech at Apex Group, said in a statement that firms must treat tokenization as a business transformation exercise, not just another tech-integration project.

“Almost all respondents rely on third-party providers to some degree, reflecting the complexity of integrating tokenization across custody, compliance, and operational processes,” added Bennett.

The dominant driver is access with nearly half, 42%, of respondents citing broadening the investor base as their primary objective. Private markets are the clearest entry point with almost half, 45%, of firms tokenizing private market assets.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

Project Pangea brings together dozens of global financial institutions from across Europe and South Korea.

-

Establishment of the branch is part of Northern Trust’s broader European expansion strategy

-

The digital depositary receipts use blockchain infrastructure operated by SIX to tokenize private shares.

-

2026 is expected to be a pivotal year amongst competing models for global money movement.

-

Institutions will connect onchain activity with traditional payment rails.