07.09.2026

Nicolas Rivard, global head of cash equity and data services at Euronext, has been with the group for a decade. Rivard told Markets Media that when he joined Euronext in 2016 it was a relatively small company but had a lot of ambition. The company’s turnover was then below €500m, compared to more than €1.8bn in 2025.

“Today Euronext is in the CAC 40, is a much larger company, but is still ambitious,” he added. “Our strategic plan for 2027 is progressing very well and we are always striving to find new ways to grow the company.”

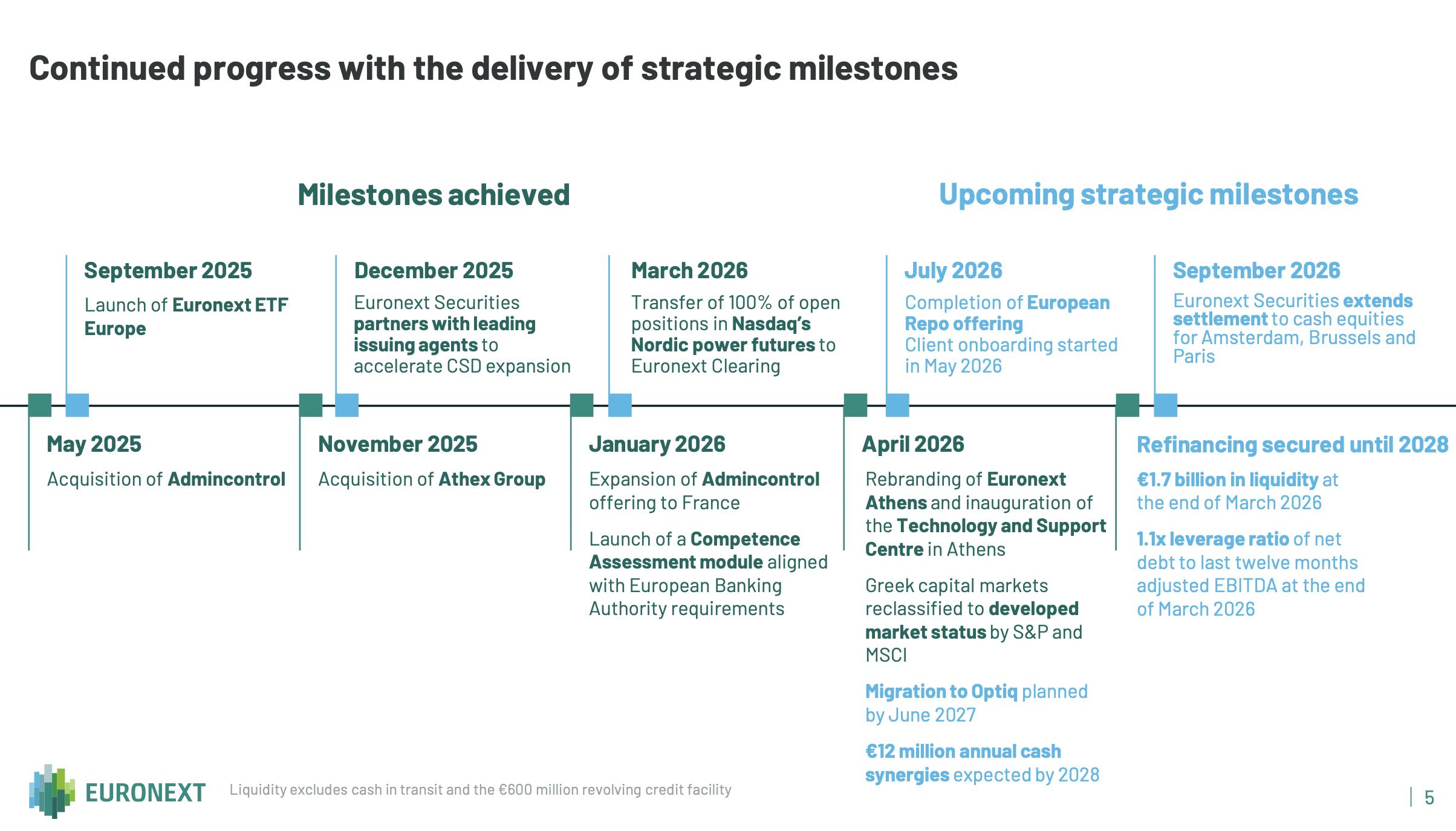

Those ambitions include integrating Euronext Athens, which it acquired last year; becoming the main listing venue for exchange-traded funds in Europe; further boosting retail participation in equity markets in the region; and streamlining the fragmented post-trade financial market infrastructure in the region.

Euronext Athens

In April this year Euronext rebranded the Athens Exchange Group to Euronext Athens. Camille Beudin, member of the executive committee of Euronext and chairman of the board of Euronext Athens, said in a statement that the rebranding is a key step integrating the Greek capital market into Euronext’s pan-European model.

The Greek markets are due to migrate to Optiq, Euronext’s proprietary technology platform, in June 2027 with clearing and the central securities depository (CSD) moving in 2029. Rivard said: “It is a playbook that we know well as we have done it three times already in Ireland, Norway and Italy.”

Euronext also integrated a technology and support centre in Athens, which it said positions Athens as a financial and technology hub in Europe and creates more opportunities for group-level cost management efficiency.

Nicolas Rivard, Euronext. Copyright: Euronext_Charlène Yves

In the first quarter of this year Euronext reported average daily cash trading volumes of €16.6bn, an 18.8% year-on-year increase on a pro forma basis, which it said was supported by a strong contribution from Athens. On 20 March 2026 Euronext set a new record of over €38bn traded in a single day on the cash equity markets.

Rivard said trading volumes in Athens since the beginning of 2026 have been very strong and equities average daily volume has doubled compared to last year. He expects that the integration into Euronext is will drive additional volume, as happened in Dublin, Oslo and Milan.

In addition, volumes are likely to be boosted by index providers announcing that they will upgrade the Greek capital market to developed market status.

ETF consolidation

In May this year Euronext said in a statement it had launched testing for its European Central Securities Depository (CSD) expansion. Euronext Securities is scheduled to launch in September this year and offer an integrated CSD service for equities and ETFs in Belgium, France and the Netherlands, complementing its existing markets in Denmark, Greece, Italy, Portugal and Norway.

“The European expansion of Euronext Securities is super important in tackling friction as we will manage the complexity so clients can trade equities and ETFs in other countries with the same simplicity and same cost as in their home market,” added Rivard. “The large banks and major custodians are very supportive of the project as they want increased efficiency.”

Rivard highlighted that ETF liquidity in Europe is fragmented as the same fund is listed and traded across multiple exchanges. Last September the group launched Euronext ETF Europe in order to provide a single, consolidated order book that aggregates liquidity in each ETF, which Rivard said is delivering better execution quality and tighter spreads.

He described the expansion of Euronext Securities as complementary to the ETF platform on the post-trade side, by consolidating settlement and custody across all its markets into a single CSD framework, removing cost and complexity for issuers and investors.

“ETF issuers are very supportive of consolidating listings on one market and we have commitments from issuers that represent 90% of assets under management,” said Rivard. “We want to be the main listing venue for ETFs in Europe, offering access to Euronext markets, a huge distribution network and great liquidity.”

Euronext has migrated its own shares to Euronext Securities, and completed the first IPO in Euronext Amsterdam for which an issuer directly appointed Euronext Securities as the issuer CSD.

Retail activity

Another ambition is to continue to increase retail participation in Euronext markets. Rivard said volumes from retail investors were up more than 40% from a year ago and that a record nine million retail investors are subscribing to Euronext data, which has more than doubled in two years.

In response to retail demand, Euronext has expanded the universe of stocks that are available to trade. Euronext’s Global Equity Market (GEM) allows investors to trade European and U.S. stocks on its Optiq technology. Rivard said: “For example, SpaceX has been trading on GEM since the IPO.”

SpaceX, Elon Musk’s artificial intelligence and space company, raised a record $85.7bn in its initial public offering in June this year on Nasdaq in the U.S.

In addition, Euronext has expanded Best of Book to all countries where it operates a regulated exchange, except Greece, which may be added in the future. Best of Book offers best execution on Euronext stocks for retail brokers and allows the exchange to be very competitive with regard to fees. It was also initially focused on the most liquid stocks, but now covers all stocks traded on Euronext according to Rivard.

“We launched Best of Book in Italy last November and it has been a huge success,” he added. “Best of Book is trading €500m a day and volume has doubled year-on-year.”

Stéphane Boujnah, Euronext

Stéphane Boujnah, chief executive and chairman of the managing board of Euronext, said on the group’s first quarter results call that it is clear there is unprecedented momentum to deliver the European Union’s Savings and Investment Union initiative and accelerate the transition of retail investment towards lit markets.

“I think the most profound transformation for a company like us is that there is now a commitment to create tools to make sure that the €13 trillion of savings that exist in Europe that are underinvested in long-term, in the financing of risk is going to find ways to be channelled towards equity markets and towards lit public markets,” added Boujnah. “It may not be spectacular immediately, but it’s a profound evolution that will make, over time, the E.U. market closer in terms of allocation of household savings to what we can observe in the U.S.”

ESMA review

Boujnah stressed the importance of lit markets and ESMA, the European Union’s financial regulator, has been consulting on market structure in the region .

Verena Ross, Esma

The Federation of European Securities Exchanges, FESE, said its response to the consultation that a key trend identified in the ESMA analysis is the gradual shift of trading activity away from continuous lit trading towards less transparent and/or accessible execution mechanisms, with the largest proportional increase recorded in systematic internalisers’ activity.

FESE said: “As a growing share of trading relies on prices formed on RMs and MTFs without directly contributing to price discovery, preserving robust price formation should remain a central objective of EU market structure policy.”

Euronext is pushing for a level playing field for trading mechanisms between multilateral and bilateral trading, so that liquidity remains accessible to all market participants in a fair and transparent manner according to Rivard.

“There are some auction mechanisms which have grown over the last few years that are called transparent, but in reality most execution is pegged to the midpoint of lit continuous pricing, so they do not contribute to price formation,” he added.

In March 2024 the group launched Mid-Point Match, its suite of dark, mid-point and sweep functionalities embedded within Euronext’s central order book in Brussels. In April 2024 Mid-Point Match was launched across all Euronext markets.

Rivard said Euronext launched its dark book in response to client demand.

“It’s embedded in our own order book and executes with no latency; the liquidity it attracts ultimately feeds back into the lit book,” he said. “Lit markets remain the backbone of price formation, and finding the right balance between the two is the responsibility of both the market and regulators.”

Last December the group also launched Auction Volume Discovery as a mechanism to trade the imbalance at the opening or closing auctions and benefit from the opening or closing price, after other exchanges launched similar mechanisms. Rivard said: “My conviction is that it will become a standard part of the auctions.”

Source: Euronext

Data

FESE also said in its response that one of the clearest messages emerging from the ESMA call for evidence is the need to improve data quality and transparency in the off-exchange space. Existing shortcomings in transaction reporting and trade flagging limit the ability of regulators, market participants and policymakers to accurately assess market activity, execution quality and market structure developments.

“Strengthening data quality should therefore be regarded as a priority and a prerequisite for effective supervision, informed policymaking and a sound understanding of how European equity markets are evolving,” added FESE.

Rivard also leads the data services business and said one of the key pillars of Euronext’s strategy is to monetise the group’s datasets. He added: “I’m very happy with the result.”

In the first quarter of this year, revenue in Advanced Data Solutions grew to €69.3m, up 6.5% compared to the first three months of 2025. Euronext said this highlights strong retail demand, the ongoing monetisation of the diversified data set, and the contribution of Euronext Athens.

Other exchanges have made acquisitions other to boost their data businesses. Rivard said Euronext has looked at acquisitions many times in the data business , but they did not fit the group’s financial discipline.

He argued that Euronext has been “very rigorous and successful” in creating, launching and distributing data products, and in building analytics, such as quantitative products.

In addition, he said Euronext’s data center in Bergamo is a “unique value proposition.” In 2022 Euronext relocated its data centre from Basildon in the U.K. to Bergamo in Italy. Rivard said there is a strong latency advantage in having the dark book close to the lit book, and the largest equity pool in Europe alongside MTS, Euronext’s fixed income platform.

“Our data business is based on the proprietary real-time data created by our order book across asset classes, which is very valuable,” he added.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

The tape will support better price discovery and facilitate more informed investment decisions.

-

A new intelligence layer allows instant contextualisation of live market flow against historical benchmarks.

-

The index only includes tokens and companies that show real-world use and generate revenue.

-

Private credit has never had a benchmark built from real deal data.

-

Fenics Market Data, OpenYield, and Tradeweb are joining Pyth as data providers.