06.11.2020

The fixed income, currencies and commodities markets standards board has published the first of a series of reviews on the transition from Libor which is due to be discontinued at the end of next year.

Martin Pluves, FMSB

Martin Pluves, chief executive of the FMSB, told Markets Media: “There have been some shifts in the interim deadlines for the transition but the end of Libor at the end of 2021 has held. We had no problem gaining attendance at workshops despite the turmoil during the start of the pandemic, showing clearly the industry is very focussed on this issue which remains a high priority.”

The FMSB is not a regulator but a voluntary industry body setting standards for wholesale FICC markets after a review by UK regulators in 2015 raised serious concerns about poor standards of behaviour. Pluves took over as chief executive in November last year from his previous role as chief executive of LCH Ltd, a clearing business at London Stock Exchange Group.

“We were asked by members to help fill a gap and provide practical and pragmatic support on the challenges of the transition,” he added. “The regulators and industry working groups on Libor provide the building blocks and put the bricks in place and the FMSB is seeking to add the mortar.”

Read ‘LIBOR transition: Case studies for navigating conduct risk’ – our Spotlight Review includes good practice observations and practical case studies to support firms as the market moves to risk-free rates https://t.co/83H1O442iR pic.twitter.com/8XnWqnOFrZ

— FMSB (@FMSB_UK) June 11, 2020

After the financial crisis there were a series of scandals regarding banks manipulating their submissions for setting benchmarks across asset classes, which led to a lack of confidence and threatened participation in the related markets. As a result, regulators have increased their supervision of benchmarks and want to move to risk-free reference rates based on transactions, so they are harder to manipulate and more representative of the market.

The UK Financial Conduct Authority said two years ago that it will not compel panel banks to submit to Libor beyond 2021, and this has not changed despite the Covid-19 pandemic.

The FMSB paper highlights challenges, including conduct-related risks, for market participants to address when offering new products to clients or changing performance benchmarks. The study includes four case studies covering cash and derivative products and performance benchmarks.

“We detail the types of issues that firms should be thinking about when communicating with clients and in managing their risks,” said Pluves. “There is no single right answer to Libor and each firm needs to take responsibility for picking its own course.”

He continued that the paper is the first of a series and the feedback has been very good.

“In the future we are likely to broaden the topic set and look at the impact on term products that extend beyond the expected end of Libor and the legacy contracts that are tough to transition,” Pluves added.

Chris Salmon, HSBC

Chris Salmon, FMSB chair of the IBOR transition working group, and chief control officer for global markets at HSBC, said a statement: “With the deadline fast approaching for the discontinuation of the Libor interest rate benchmark, FMSB’s practical guidance and case studies will be, now more than ever, relevant to corporates, insurers, asset managers and banks, who are currently managing their transition to alternative risk-free reference rates.”

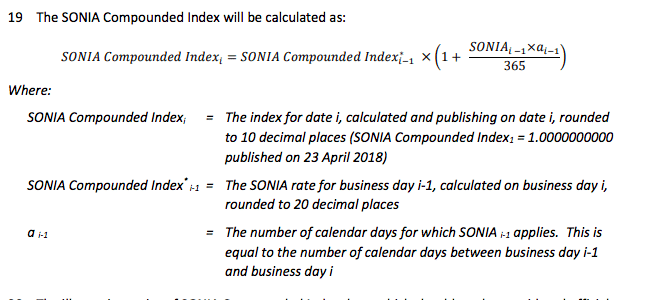

Sonia index

The UK has chosen the sterling overnight index average, Sonia, as its risk-free rate. The Bank of England said today it will start to produce a Sonia compounded index.

The Bank will publish a daily SONIA Compounded Index from early August, find out more here: https://t.co/J20yNIjiTc

— Bank of England Press Office (@BoE_PressOffice) June 11, 2020

The Bank issued a discussion paper in February this year on its intention to publish a daily Sonia compounded index and only one respondent out of 41 was not in favour.

“Respondents saw the introduction of an index by the Bank as a positive step forward, and something that would play a valuable role in risk-free rate transition by helping to provide a standardised way of calculating compounded rates and allowing end-users to validate interest rate calculations produced by financial institutions,” said the Bank.

Sonia compounded index. Source: Bank of England.

Respondents supported the Bank’s proposed methodology and emphasised the benefits of international consistency given the similarities to the SOFR index’s calculation methodology. The US has adopted the secured overnight financing rate, SOFR, as its risk-free rate to replace US dollar Libor.

The Bank of England also set up a sterling risk-free reference rates working group to help co-ordinate the industry’s transition from Libor.

Tushar Morzaria, Barclays

Tushar Morzaria, chair of the working group, said in a statement: “ The transition away from Libor to more reliable and robust rates has long been a regulatory and market imperative and the FMSB work will fill an important role alongside the technical work already completed by the RFRWG and other bodies internationally.”

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

The partnership focuses on quantitative strategies for listed equities.

-

The group becomes a major European fund manager with over €1,500bn in assets.

-

The proposal would modify certain leverage capital standards for the largest systemically important banks.

-

The electronic syndicated loan trading platform has also raised $46.5m.

-

The senior-level forum allows the Monetary Policy Committee to hear directly from market participants.