05.21.2020

More than three quarters of North American buy-side managers trading foreign exchange for the majority of their time are frustrated with legacy technology and are looking to invest in new platforms.

The Finance Hive, a private network for the senior buy-side community, surveyed 60 North American heads of trading with half working for firms managing more than $100bn (€91bn) of assets in partnership with EBS, the electronic FX platform owned by CME Group. The study found that 77% of respondents want to invest in new platforms.

The head of currency management at Mellon Capital said in the report: “In an ideal world, I would like the opportunity to have more flexibility and seek out the best products for each stage of the investment process, but legacy infrastructure and dealing with all of the integration requirements result in huge projects, where the means often don’t justify the ends.”

EBS said in the report that some market participants believe that delivering one end-to-end monolithic system can solve numerous problems, but the implementation risks involved in switching platforms for the entire trade lifecycle are too great.

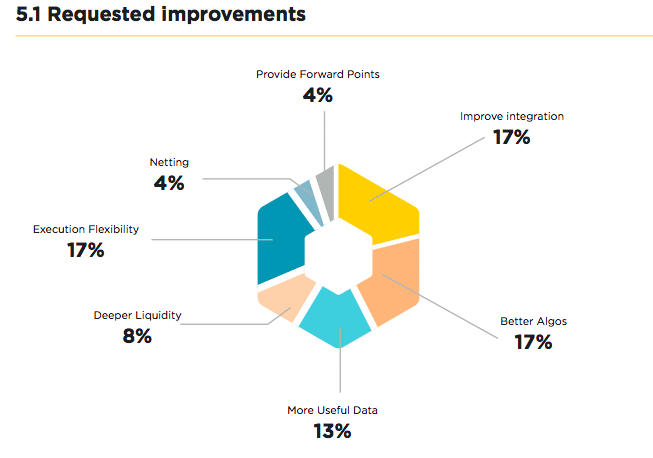

Requested Improvements To FX Platforms. Source: The Finance Hive.

“Our belief is that better solutions can be created through rapid integration of multiple existing and new systems through some form of middleware, picking best of breed where it is needed, and leaving robust operational processes firmly in place where they exist,” added EBS. “These middleware solutions have not yet emerged properly in FX, but it seems that the demand is building, and a growing number of asset managers are more willing to implement.”

Ashish Bhagwanjee, senior portfolio manager at Dimensional Fund Advisors, said in the report that he uses a number of platforms.

“We like to think of them as tools in a tool box, so we use different tools for different purposes,” he added. “The main drawback is this approach makes workflow more complex and we have to be mindful of the operational risk that is introduced.”

Transaction cost analysis

Hugh Whelan, global head of liquidity management at EBS, said in an email to Markets Media that the volatility caused by the Covid-19 pandemic in recent months has highlighted the importance of asset managers having transaction cost analysis built into their trading platforms and the increasing pressure to have real-time insight into trading costs.

Hugh Whelan, EBS

Whelan continued that one asset manager at a recent Hive event said the ‘the drag factor created by manual processes on execution costs has been exposed recently and will lead to a shift away from this on the buy side.’

“This suggests many portfolio managers will begin to adjust their trading styles to better monitor and benchmark their best execution requirements,” added Whelan. “From working out how to reduce execution costs ($ per million) to ensuring their liquidity providers are responding in a timely manner and pricing competitively, these findings show there needs to be more emphasis on the pre and post-trade execution cost analysis component of any trading platform, and what it can offer in terms of harnessing big data, real-time and as efficiently as possible.”

Less than half of FX market participants use benchmarks to measure trade performance, and fewer use sophisticated TCA systems that have developed in other asset classes according to a report from Greenwich Associates in March this year.

The consultancy said in the study, Digitization Delayed: Why Algos Aren’t More Popular in FX, that this is one of the reasons for the relatively low level of uptake of algorithmic trading in the asset class. Just over a third, 37% of FX market participants use algorithmic trading in the US and Europe, and they account for only 22% of their overall volume. In comparison, in equities almost half of all trading volume, 46%, is executed through either direct market access, smart order routing or algorithmic trades.

Ken Monahan, Greenwich Associates

However Greenwich expects algo trading to evolve into a mainstay in global FX due to the size of the potential market.

Ken Monahan, senior analyst for Greenwich Associates market structure and technology, said in the report: “Given the potential stakes, it is only a matter of time before issues of data scarcity and other hurdles are addressed and algorithms take on a central role in FX trading.”

FX market liquidity data

In order to provide more transparency in the foreign exchange market, FXLIQUIDITY was launched this week by Mosaic Smart Data, the real-time capital markets data analytics company, in collaboration with CLS, the FX settlement market infrastructure and MUFG, the Japanese bank.

Mosaic Smart Data will publish weekly analysis of liquidity changes across key currency pairs using natural language generation technology to generate instant written reports from the data.

Leveraging our unparalleled source of FX executed trade data, we have collaborated with MUFG and Mosaic Smart Data to further enhance transparency in the FX market. https://t.co/v21msO5G9d#fx #fxmarket #data pic.twitter.com/kEuVmv4uM4

— CLS Group (@CLSGroup) May 18, 2020

John Winter, chief executive of MUFG Securities EMEA, and head of global markets and corporate and investment banking at MUFG in EMEA, said in a statement that COVID-19 has created many new variables in markets which can be fast-moving and difficult to navigate.

“We wanted to provide a service to our corporate treasury and institutional clients to help them to better understand what is going on and how the situation is developing in as much detail as possible,” Winter added. “Being able to access insights drawn from CLS’s broad view across the markets is a significant part of the solution in rapidly understanding how liquidity flows are evolving.”

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

Members can source block liquidity while working algorithmic strategies in the broader marketplace.

-

The integration of dbHedge into LiquidityFX augments smartTrade’s existing tools for internalising FX flow.

-

The briefing touches on emerging technologies and outlines considerations for using AI.

-

There was a 34% improvement in predicting how likely a trade would be filled at a quoted price.

-

Execution algorithms are a growing share of global spot FX, particularly among buy-side firms.