06.08.2026

U.S. Banks Fight Stablecoin Growth with Tokenized Deposits

06.08.2026

S&P Global Ratings said significant growth in the use of stablecoins could impact for the U.S. banking sector, as a bank consortium said it is launching a tokenized deposit platform.

On 4 June 2026 the ratings agency said in a report that significant growth in the use of stablecoins following the passage of the GENIUS Act by the U.S administration could have implications for the U.S. banking sector. The GENIUS Act was passed in July last year and provided the first federal framework for stablecoins. Industry participants are still waiting for finalized regulations related to the GENIUS Act, and for the Clarity Act for digital asset market structure to be passed.

Most demand for U.S. dollar-pegged stablecoins originates outside the U.S, so they pose limited immediate risk to domestic U.S. bank deposits or national payment rails, while generating demand for U.S. Treasury bills according to S&P. However Michal Selbka, credit analyst at S&P Global Ratings, warned in a statement that this dynamic could shift if stablecoins expand beyond their current use as primarily settlement assets for crypto trading or as a hedge against local currency volatility abroad.

Growing stablecoin use could pose a competitive threat to banks’ payment income; have ramifications for reliance on deposit funding in the banking sector and for deposit pricing; weaken banks’ capacity to lend if deposits shifted significantly toward wholesale from retail, while loans could become more expensive if deposit yields rise, according to S&P.

Stuart Plesser, credit analyst at S&P Global Ratings, said in a statement: “In our view, banks that embrace innovation in developing tokenized products will be more resilient to potential competitive threats from nonbanks.”

Bank innovation

On 5 June 2026 a group of banks said they will combine onchain activity with traditional payment rails and enable clearing and settlement of tokenized commercial bank money at scale. The solution will combine the existing regulatory, operational, and settlement frameworks of established payment market infrastructure with the programmability and interoperability of blockchain-enabled financial activity. The initiative will be operated by The Clearing House, a U.S.-based payments company owned by 25 financial institutions.

Shahmir Khaliq, head of services at Citi, said in a statement: “With solutions like Citi Token Services now live and at scale, and with tokenized securities rapidly gaining momentum, there is a critical need for The Clearing House to establish clearing infrastructure across member banks for both traditional and tokenized deposits facilitating industry-wide 24/7 and interoperable movement of cash and securities in the future.”

Fernando Castellanos, global head of digital currency & sponsor banks at Prove, which provides software for digital trust, said in an email that this signals that traditional financial institutions are no longer viewing blockchain-based finance as something happening on the sidelines.

“Banks recognize the same benefits that have driven stablecoin adoption – real-time settlement, greater efficiency and 24/7 money movement – while also positioning themselves for the broader shift toward tokenized financial assets,” Castellanos added. “The goal isn’t simply to control crypto and the world of stablecoins; it’s to play a leading role in how tokenized assets are issued, transferred and managed as adoption accelerates.”

S&P highlighted that US Bancorp has also started a pilot program for a stablecoin on the Stellar network, while the Bank of North Dakota and Fiserv have partnered to develop a stablecoin for the state, the Roughrider coin. The ratings agency does not currently include the impact of stablecoins in its view of bank ratings but will monitor the implications as their use expands.

“For example, were a bank to experience a large deposit outflow because of its customer base opting to use stablecoins outside of the bank, or if a bank were compelled to raise its funding cost as a result of stablecoin pricing competition, negative rating actions could follow,” added S&P.

Tokenized deposits

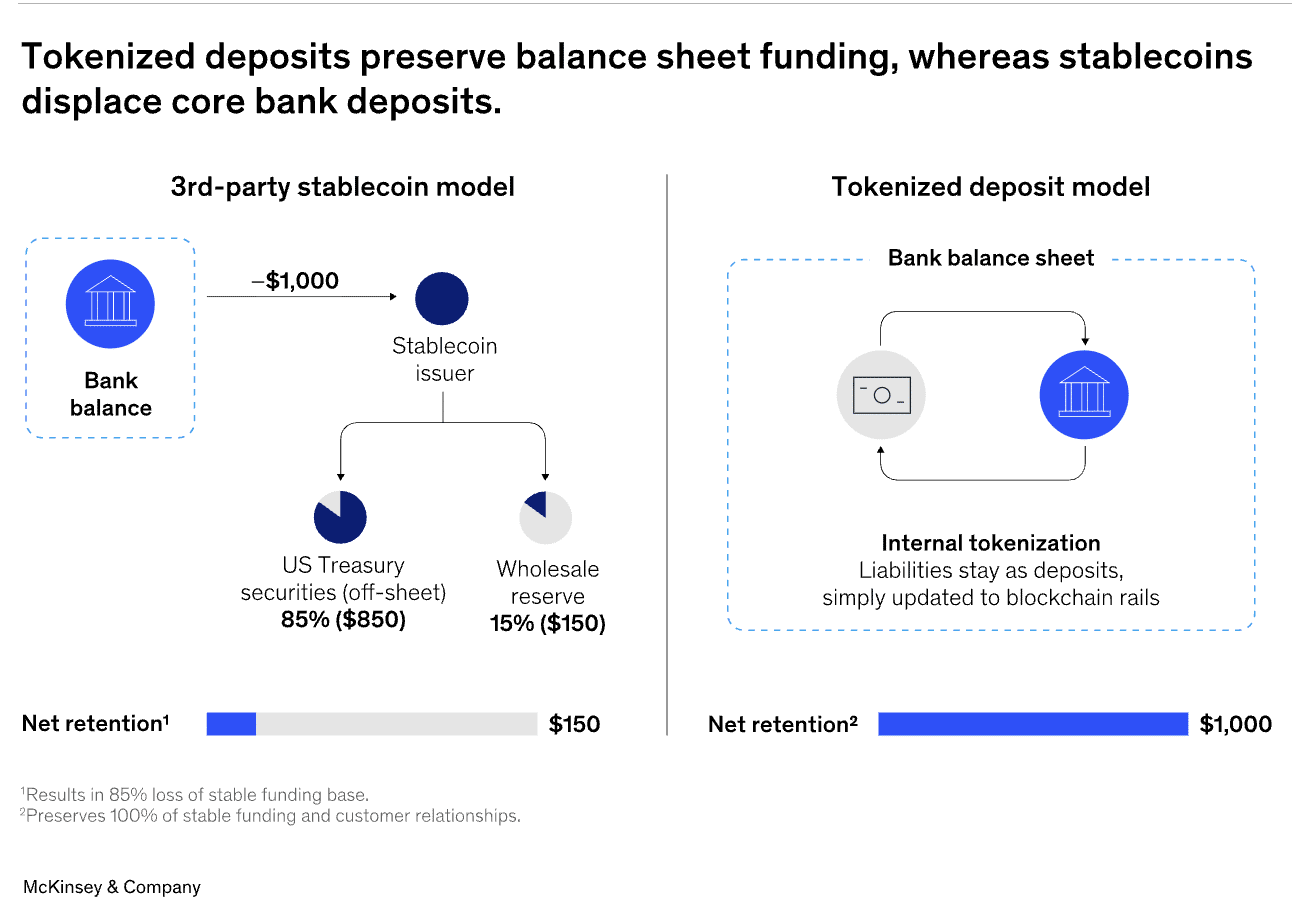

Consultancy McKinsey & Company highlighted in a report that stablecoins are forecast to reach $4 trillion in adoption by 2030. In contrast, tokenized deposit infrastructure flows are estimated at more than $4 trillion annually, and are embedded directly into existing institutional payment, liquidity, and treasury workflows.

“JPMorgan’s Kinexys alone is estimated to facilitate more than $1 trillion in tokenized deposit transfers annually, supporting internal treasury movements, intercompany payments, and institutional settlements,” added McKinsey. “It is likely that other large banks are supporting similar volumes, especially those that historically maintained a meaningful cross-border payments business.”

The consultancy explained that the fundamental difference between stablecoins and tokenized deposits is their effect on bank balance sheets. Stablecoins are issued by third-party private institutions and McKinsey estimated that for every $1,000 converted into a third-party stablecoin, only 15% typically returns to the banking system as wholesale reserves. In contrast, tokenized deposits keep the full $1,000 on the balance sheet and banks gain programmability, faster settlement, and operational efficiencies.

However, tokenized deposits are not interoperable because coordination across banks is slow, complex, and commercially sensitive, according to McKinsey. The consultancy highlighted that the regulatory landscape favors bank-issued assets as they are treated in the same way as traditional deposits.

“Tokenization changes the form factor—issuing deposits on a blockchain and making them programmable and divisible—but not the legal nature of the liability, nor its LCR treatment or funding stability,” said McKinsey. “This distinction is attractive for yield-sensitive corporates and institutions managing large balances because banks can continue to pay interest on deposits.”

The consultancy concluded that current trends suggest that 2026 will be a pivotal year as competing consortiums and interoperability projects test which models can solve the long-standing frictions of global money movement.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

Shared infrastructure can unlock value for individual institutions and the whole financial system.

-

The European Commission aims to advance a more integrated single market for banking & financial services.

-

They aim to build a bridge between Japan's capital markets and the global tokenized economy.

-

HSBC and LSEG have signed an MoU to develop connectivity to support investor access.

-

First phase of DTCC's tokenization project has gone live.