05.06.2026

Apollo Global Management’s total assets under management surpassed the trillion-dollar milestone for the first time as the alternatives manager said it has launched a pilot to value its private asset portfolios on daily basis.

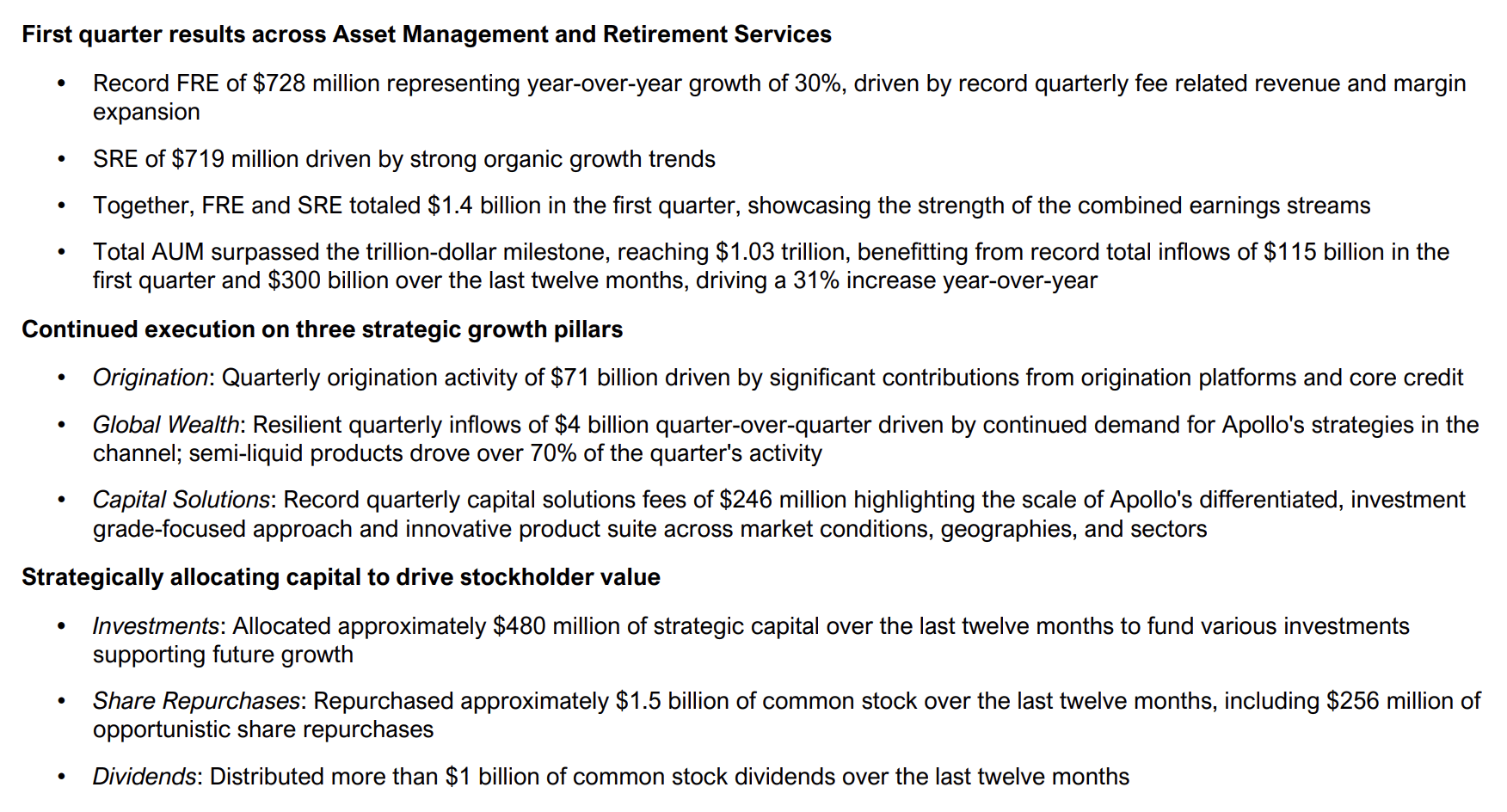

Marc Rowan, chairman and chief executive at Apollo, said on the first quarter results call on 6 May 2026: “Our first quarter results set a strong tone for the year, with record fee-related earnings and assets under management surpassing $1 trillion.”

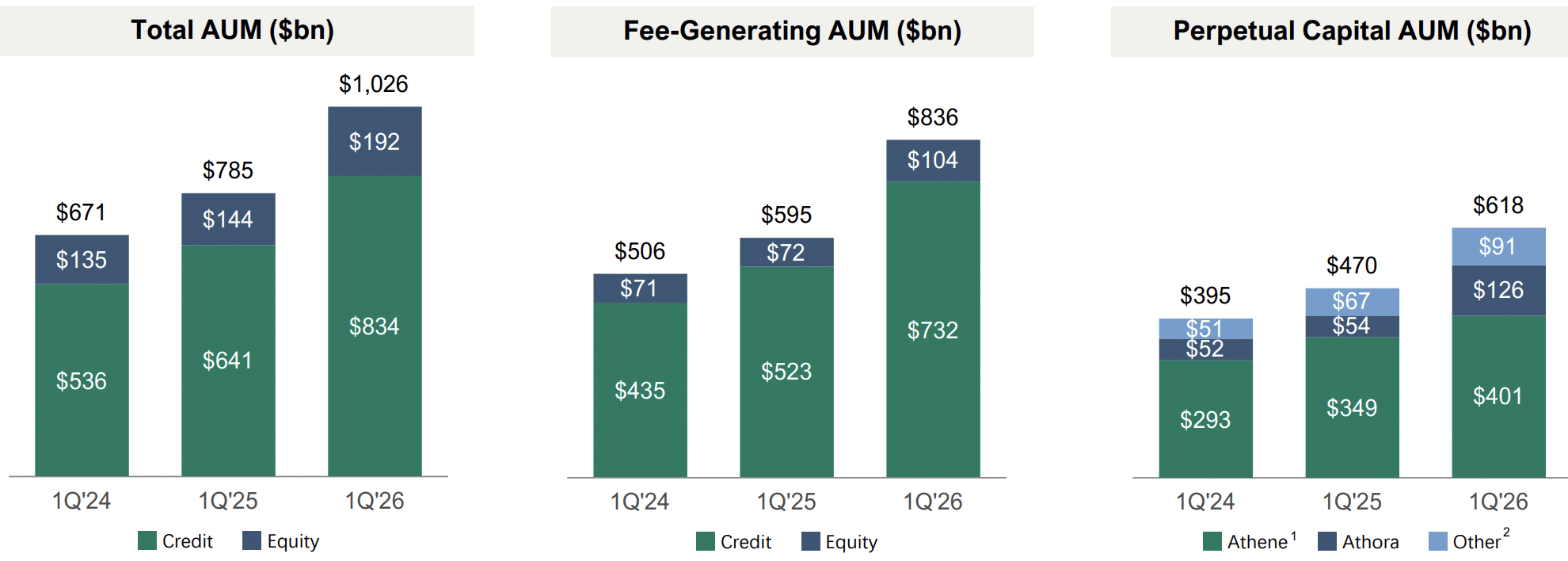

Apollo reported record total inflows of $115bn in the first quarter and $300bn over the last twelve months, driving a 31% increase year-over-yearin assets under management to $1.03 trillion on 31 March 2026.

Inflows of $95bn from the asset management business were driven by Athora’s acquisition of the Pension Insurance Corporation (PIC) in the UK by Athora, a European savings and retirement services subsidiary, at the end of March as well as strong third-party institutional inflows and global wealth inflows into credit-focused strategies and the final closing of Hybrid Value Fund III. The retirement services business contributed $20bn in the first quarter due to solid activity across retail, flow reinsurance, and funding agreements.

Daily pricing

On 6 May 2026, The Financial Stability Board published a Report on Vulnerabilities in Private Credit. The report said activity has grown rapidly, and can bring benefits in the form of tailored finance for companies and diversification for investors, but also embeds several vulnerabilities. These include deepening interconnections between asset managers, banks, insurers and private equity firms; valuation opacity, reliance on private credit ratings from lesser-known providers; data gaps and concentration risks due to significant exposure to sectors such as technology, healthcare, and services.

There have also been press reports about potential losses in private credit but Rowan argued that the media is fixated on a small $2 trillion slice of the private credit market, which should be called leveraged lending. In comparison the investment grade private credit market, which is being driven by the global industrial renaissance, is a $38 trillion market, according to Rowan.

“Most of the financial press treats this as if it is the entire story of what is happening in private markets, and it is far from it,” Rowan added. “Private credit is just credit so if you underwrite well it performs, but if you underwrite poorly it doesn’t.”

In order to increase trust and transparency for investors around private assets, Apollo launched a pilot last year to produce an estimated daily value for its investment grade fixed income suite of products. By 6.30pm ET investors will have daily pricing for all corporate investment grade fixed income assets, and daily pricing for direct lending and asset backed finance by 9.30pm ET.

Rowan said: “We run a rigorous process with discipline and when public markets reprice, private markets should too.”

For example, in Apollo Debt Solutions (ADS), the $25bn private credit fund, firm will always take the lowest mark to value a position, whether or not it agrees with that mark, because it indicates where the counterparty might sell that position. The entire ADS book is marked to the syndicated loan industry and if any sector falls more than 2.5%, positions are written down.

Market making

Market making is another part of transparency, according to Rowan, due to the continued convergence of public and private assets.

“We have never seen a market where enhanced liquidity and enhanced transparency does not result in tremendous growth for the asset class,” he added. “Last year, we started really pushing on market making in private markets.”

After the financial crisis, large investment banks were encouraged to de-emphasize market making in equity markets, and Rowan said four firms stepped in to provide liquidity led by Jane Street and Citadel. However, this did not happen in fixed income. Trading capital in fixed income is 10% of what it was in 2008 and the market is three times its size, according to Rowan.

“We have already seen wholesale breakdowns in fixed income liquidity during Covid and UK LDI, and I expect that we will see this again,” said Rowan. “The vast majority of issues do not trade and have not traded.”

Therefore, just over a year ago Apollo launched market making as it wanted to support State Street’s ETF that mixed public and private investment grade fixed imcome for the first time, and the firm created a data warehouse that was made available to other dealers as it wants more firms to provide the service. Since the launch of market making, Apollo has traded more than $13bn of private assets, according to Rowan. He said the first quarter of this year was exceptionally strong for market making, as fund managers recognize that Apollo is the leading source of liquidity for private market assets, particularly in credit.

In March this year Apollo was an anchor partner for Intercontinental Exchange’s launch of ICE Private Credit Intelligence. As a result, every private asset in Apollo’s portfolio going forward will have an ICE ID number which Rowan said is the beginning of standardization across the marketplace.

“It also gives us a tremendous amount of information on real-time pricing and helps inform our estimated daily values across our credit portfolio,” added Rowan. “We have got the market going, but ICE IDs, data repositories, standardized data and ultimately, jealousy, are going to cause market making competition.”

Outlook

Rowan described the $71bn origination in the first quarter as “particularly high quality.” Based on Apollo’s pipeline, he expects origination in the second quarter to be stronger, and possibly near to the record $97bn of origination in a quarter.

“Whether we get all the way there or not will depend on how hard the team works, but I think we have a shot at doing something very close to that,” he said.

Based on the first quarter and the pipeline for the year, Apollo reaffirmed its 2026 outlook of 20% fee-related earnings (FRE) growth and 10% SRE growth and is confident of meeting its 2029 targets. Rowan argued that business trends continue to be highly favorable despite geopolitical pressures as employment statistics are good, the capital expenditure cycle is “awesome,” U.S. government policy is accommodative and capital markets are open.

However, the company will continue to be defensive to protect capital and make sure it can ride through cycles if there are corrections. For example, Rowan said that Apollo has zero exposure to software in its equity business, across both private equity and hybrid equity. In credit, the firm has moved more towards investment grade and the business has less than 2% exposure to software.

Jim Zelter, president of Apollo Global Management, said on the call that institutional investors are not pulling back from private credit. In contrast, the volatile backdrop is drawing interest from institutions actively looking to deploy in a variety of structures in credit and the level of global engagement remains high. He argued that there will be dispersion across managers and investors will see who has been managing portfolios prudently for the long term, so there is an opportunity for differentiation.

Rowan added: “Jim and I have each worked more than 40 years and for the vast majority of that time we have seen and managed our business with the notion that 95% of the outcomes will occur on the playing field and not outside the sidelines. Sometimes we like what’s on the playing field, and sometimes we don’t in terms of rates and economic cycle, but we know how to navigate cycles.”

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

The PMAX fund platform has removed the accredited investor requirement & cut minimum investment amounts.

-

The U.S. Department of Labor’s Employee Benefits Security Administration issued the proposed regulation.

-

The joint venture will develop India-focused alternatives capabilities.

-

The alternatives manager said only Leon Black, who left in 2021, had a relationship with Epstein.

-

The alternative asset manager is going to expand origination in Europe and Asia Pacific.