04.10.2026

Infrastructure Needed to Turn Tokenized Assets into Functioning Markets

04.10.2026

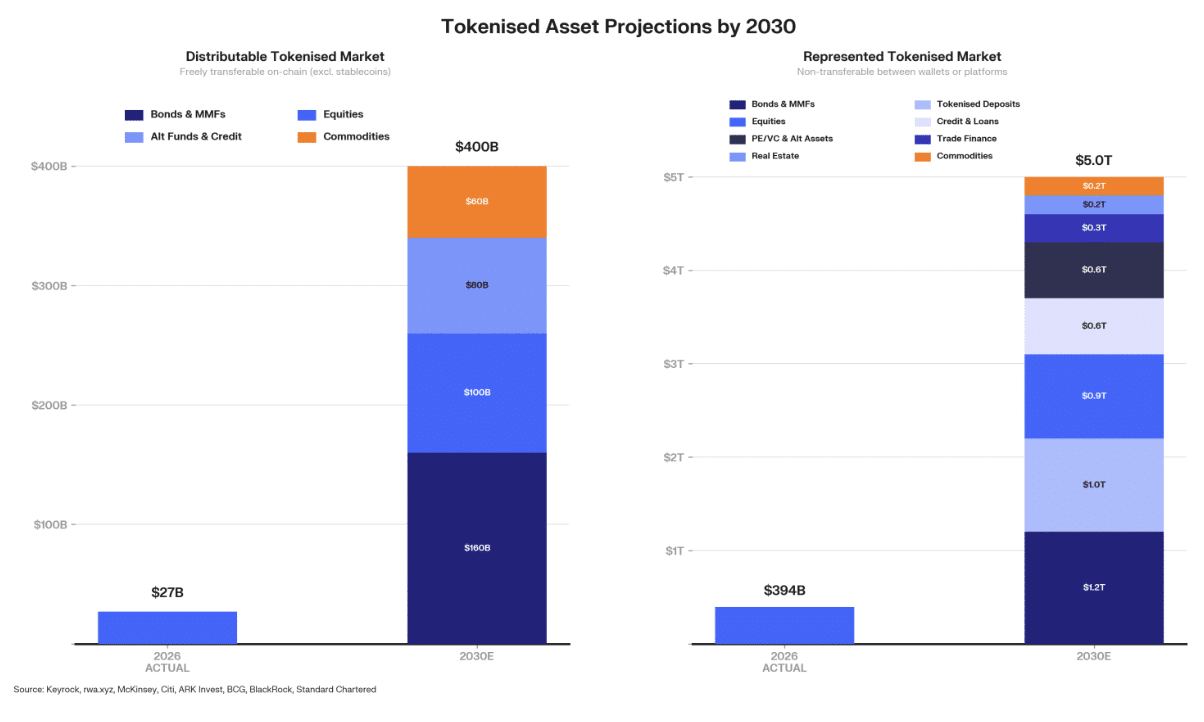

The transferable tokenized real world asset (RWA) market is predicted to expanding from $27bn to $400bn by 2030 according to a report from crypto investment firm KeyRock and tokenization platform Securitize. Freely transferable RWA tokens are issued on public blockchains and composable within the broader crypto i.e they can be used in decentralized applications and protocols to seamlessly interact with one another.

Their report, The $400T Future of Tokenised Assets, said that during the same period assets tracked on public blockchains, but not yet freely transferable, will reach $5 trillion.

“The pace of that shift depends on integration into existing financial workflows,” added the report. “Large pools of capital remain constrained by settlement delays, high minimums, geographic limits, and weak secondary liquidity.”

Amir Hajian, researcher at KeyRock, said in report that U.S. Treasuries, private credit, commodities, equities and institutional alternative funds account for more than 90% of distributed value onchain. BlackRock, Apollo, Goldman Sachs, and JPMorgan are among the traditional financial institutions who have committed capital onchain and blockchain infrastructure.

Source: KeyRock

However, he highlighted that penetration against traditional markets remains below 0.1% for every asset class. In addition, four of these five asset classes have more than 89% of value in the top five wallets, which are DeFi protocols and stablecoin reserves, rather than a broad base of participants, so there are few active transactions.

Infrastructure challenge

Carlos Domingo, Securitize

Carlos Domingo, chief executive and founder at Securitize, said in the report that the most significant structural barrier remains liquidity. He added: “Institutional capital allocators need to know they can exit a position without materially moving the market. Solving this is partly a time problem, partly a product design problem, and partly an infrastructure problem.”

Haijan argued that simply putting an asset onchain is not enough as the infrastructure required to turn a tokenized asset into a functioning financial instrument, including price discovery, market making, compliant secondary transfers and composable collateral “barely exists at scale.”

Martin Quensel, co-founder at tokenization infrastructure provider Centrifuge, said in the report that just creating a token is not good enough as the token needs to be exchangeable into stablecoins, reusable in other protocols, available on public blockchains and transferable into other ecosystems.

“That sounds simple because for us it’s a given,” Quensel added. “For traditional finance institutions, it’s not.”

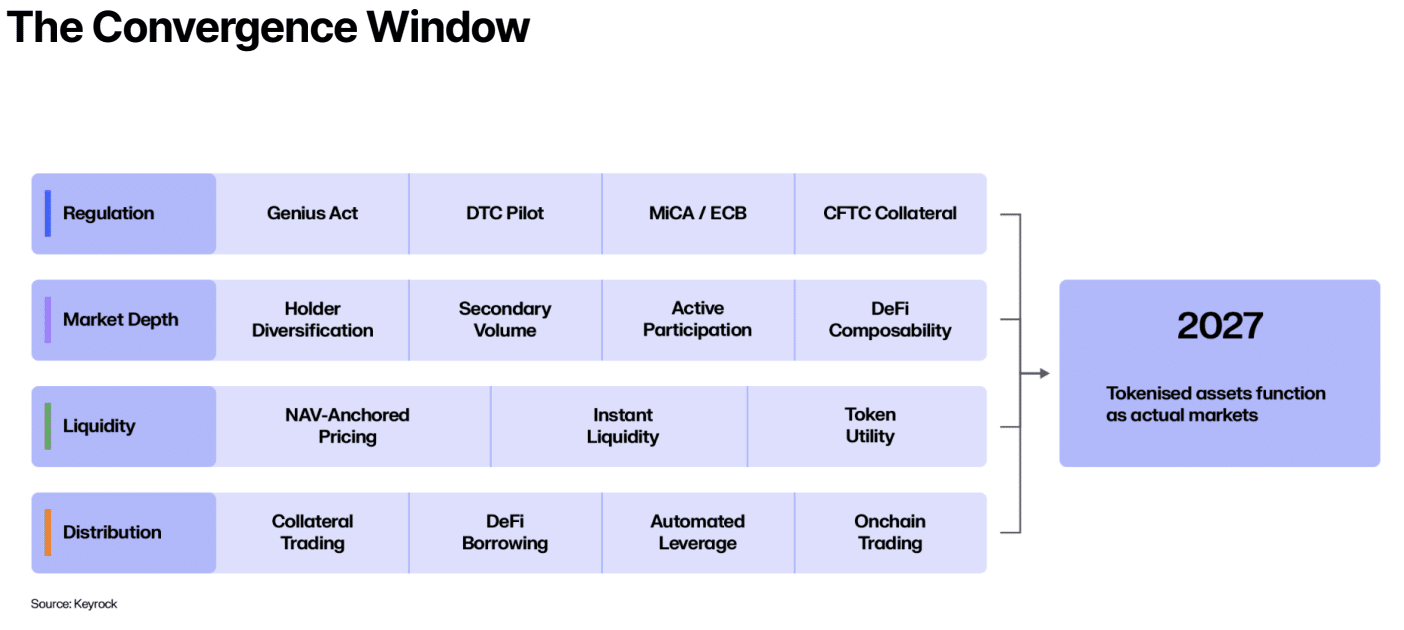

The report predicted that the required infrastructure is now reaching production and should arrive over the next eighteen months, as four forces are converging. For example regulatory frameworks are being put in place around the globe, and distribution channels are expanding and liquidity infrastructure is being built to make secondary markets economically viable.

Source: KeyRock

“2027 is the first period where regulation, market depth, liquidity infrastructure, and distribution mature together,” added the report. “The sequential dependencies that constrained the market are beginning to break.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

Treasuries, gold and S&P 500 are growing fastest onchain.

-

This enables transfers amongst Schroders’ clients and unlocks use cases such as collateralisation.

-

Onchain capability enables corporate and commercial clients to move, program, and settle funds 24/7/365.

-

Through a partnership with Circle, U.S. investors can buy and sell stocks in self-custody wallets using USDC.

-

Share classes of existing money market funds were tokenised on the Kinexys by J.P. Morgan platform.