06.24.2026

Crypto exchange Kraken has launched crypto perpetual futures in the U.S and is looking to expand the contracts into other asset classes and allow customers to use crypto assets as collateral.

On 29 May 2026 the Commodities and Futures Trading Commission approved the first perpetual futures contract on a U.S. regulated venue – the listing of a contract that references the spot price of bitcoin on KalshiEX. Perpetuals have dominated global crypto trading, with more than $60 trillion in volume in 2025, according to Kraken.

Perpetual futures trade 24/7, matching the 24/7 nature of crypto. In contrast to traditional futures, perpetuals do not have an expiration or delivery date. They track the underlying asset using a funding rate which is a periodic payment between longs and shorts – when the futures price trades above the spot price longs pay shorts, and vice versa.

On 15 June 2026 Kraken said in a statement that eligible U.S clients could begin to trade perpetuals.

John Palmer, global head of derivatives at Kraken, told Markets Media that an onshore perpetuals market is really important. He said: “The U.S. has some of the deepest, most liquid derivative markets and retail customers are significantly involved.”

Palmer said the exchange is continuing to expand access, onboard customers and market makers, and deepen liquidity. He said: “It’s early days for us and that was by design.”

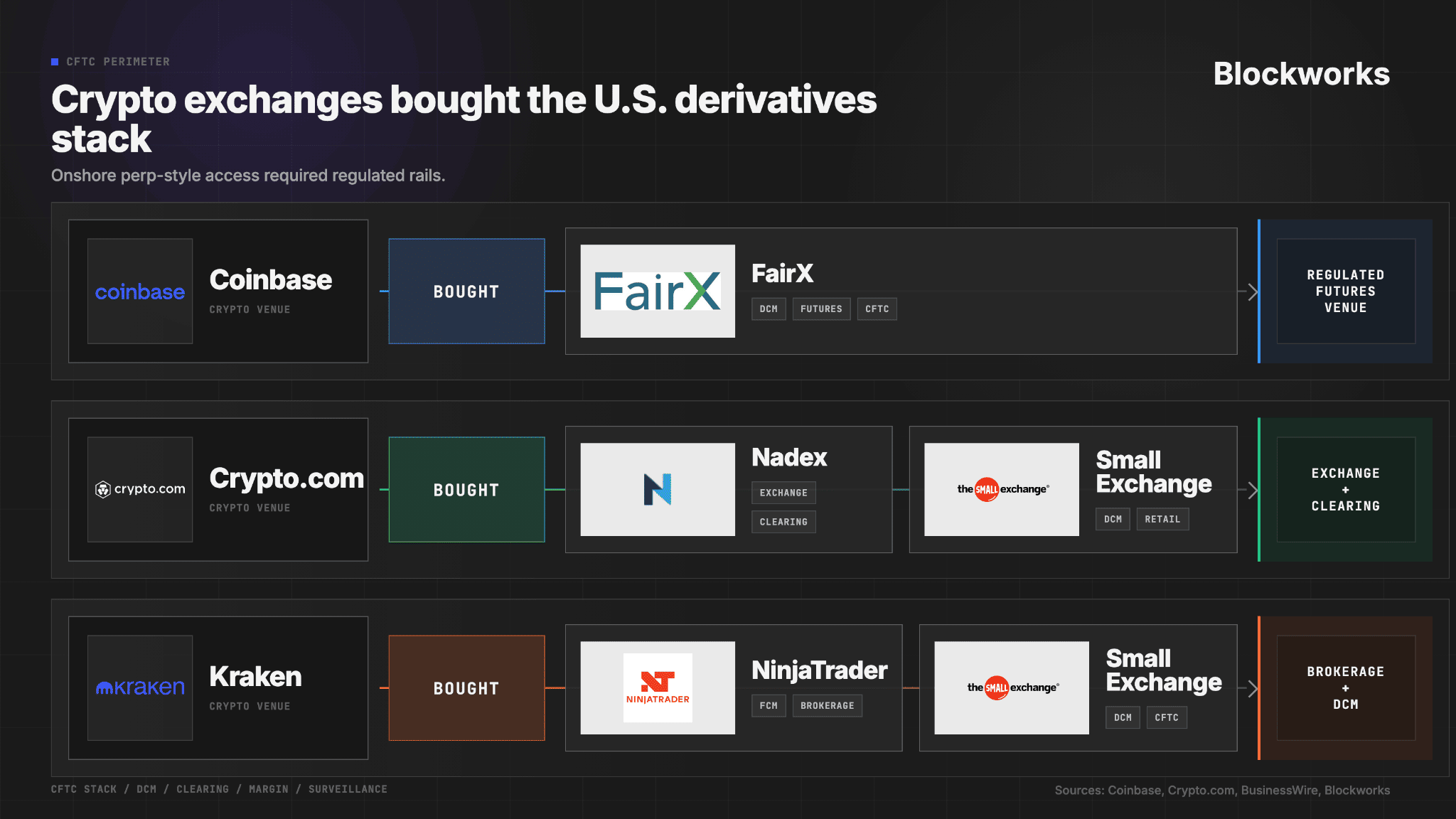

Kraken can launch perpetuals due to its acquisition of Bitnomial, the fully CFTC-licensed derivatives business, in May this year. Bitnomial holds CFTC licenses for a derivatives exchange, clearinghouse, and brokerage.

Source: Blockworks

“While we are a crypto-native firm, we have done it via the pathways that regulators have provided to us,” said Palmer. “We are really excited about pairing those licenses, infrastructure and teams with our global presence.”

Palmer highlighted that Kraken has bought perpetuals to the U.S. under the same intermediated structure that is used by institutions. He added: “We’ll see how that develops as U.S institutions can now trade perpetuals in the same way as any other future through an FCM [futures commission market].”

Collateral

Arjun Sethi, co-chief executive of Payward and Kraken, said in a statement: “Spot, margin, futures and now perpetuals all live in the same account at Kraken, with perpetuals and futures backed by the same collateral so capital isn’t stranded across half a dozen venues.”

Palmer said customers can cross-margin between the CME-listed futures, perpetuals, and spot crypto in U.S. dollars. However, Kraken wants customers to be able to use crypto as collateral for cross-margining.

“If the market is trading 24/7 then customers should be able to use collateral 24/7,” said Palmer.

Kraken has been able to offer this to customers outside the U.S. for a long time, according to Palmer. He highlighted that Bitnomial’s CFTC-licensed clearing house has regulatory approval to use crypto as collateral for margin.

John Palmer, Kraken

“We need to finish the puzzle and finalize the plumbing,” said Palmer. “I think that is a fantastic story for our customers.”

He believes the industry is becoming more comfortable with onchain collateral as financial market infrastructures such as the DTCC in the U.S. have announced that they will begin accepting tokenized assets as collateral.

“Kraken wants to focus on providing our customers with the proper experience, using crypto as collateral, capital efficiencies, and providing strong global liquidity,” Palmer added.

Convergence

Palmer joined Kraken at the beginning of 2026. His previous roles include head of options at IEX, head of options at Cboe Global Markets and president of Cboe Digital, which was formed when Cboe acquired Eris Digital Holdings (ErisX), an operator of a U.S.-based digital asset spot market, a regulated futures exchange and a regulated clearinghouse.

When Palmer started working in finance he was attracted to using technology to make markets more efficient as they were being electronified. He thought he had missed the boat on making an impact in market structure, but sees blockchain as the next electronification of markets. Palmer added: “It is a big complex puzzle and I love puzzles.”

He believes blockchain will be the financial rails of the future as customers want to trade multiple asset classes from one point of access. Institutions want to trade and hold crypto next to their ETFs and listed futures, on the same regulatory footing, and use the same clearing and margining infrastructure.

“I was pretty excited to join and be part of this team to build and help convergence really happen,” added Palmer.

He said Kraken is looking to expand its perpetual suite outside crypto so that U.S. customers have parity with international clients. For example, outside the U.S. Kraken offers perpetuals in foreign exchange and oil.

”We have a substantial roadmap of product launches and experiences that we want to bring to our customers over the next 12 months,” added Palmer.

Lawsuit

However in the U.S., CME Group has filed a lawsuit against the CFTC for authorizing perpetual futures, arguing that futures are defined as having an expiry date. Palmer argued that perpetuals are just another future on the curve, no different from three-month, six-month contracts or zero day to expiry (0DTE) contracts.

Zach Pandl, Greyscale

OxResearch, a Blockworks newsletter, said the longer-term signal is constructive as the CFTC is showing willingness to adapt existing rules around crypto-native market structure. The newsletter said: “Optimistically, that flexibility eventually extends beyond traditional DCMs and clearinghouses, with the framework widening to include programmatic exchange layers like Hyperliquid.”

Zach Pandl, head of research at digital asset fund manager Grayscale, said in a report that the CFTC approval was a positive step for regulated U.S.-based platforms like Kalshi and Polymarket. Pandl added it is a step toward a future in which decentralized finance (DeFi) platforms specializing in perpetual futures, such as Hyperliquid, are available to U.S. users as well.

Unified infrastructure

Palmer told Markets Media he had been a fan of Kraken for many years and he was very aligned with where they wanted to take the business. He said: “The concept of the access layer and the infrastructure layer fits very well with where I think financial markets are going.”

In a blog Sethi has described the company transforming from a single-product exchange into a financial platform that includes trading, custody, payments, yield, lending, and market data across both digital and traditional assets.

Arjun Sethi, Kraken

“Kraken is no longer a single-brand company,” added Sethi. “It is part of a broader financial organization built on one unified infrastructure layer.”

Since 2025, the parent entity Payward has taken on a more explicit role as the infrastructure layer that powers multiple product surfaces and interfaces including Kraken and a family of products, including NinjaTrader, Breakout and xStocks. Sethi compared Payward to Alphabet which evolved by separating core infrastructure from product expression. As a result Google Search, YouTube, Android, and Cloud all run on shared data, compute, and identity layers, which he said allows innovation at the edge without fragmentation at the core.

“Rather than forcing all users into a single ‘Frankenstein’ interface, Payward allows each product to be designed for a specific customer segment, regulatory regime, and use case,” added Sethi.

However, all the products share one global liquidity pool, one risk and margin engine, one collateral and settlement system and one compliance and licensing framework.

Sethi argued that this approach is cleaner from a product standpoint and mathematically superior.

“Once the infrastructure is built, the marginal cost of launching and operating additional products approaches zero relative to the value they add“ Sethi said. “Each new surface increases total throughput, assets on platform, and liquidity depth without duplicating risk, capital, or regulatory effort.”

Source: Kraken

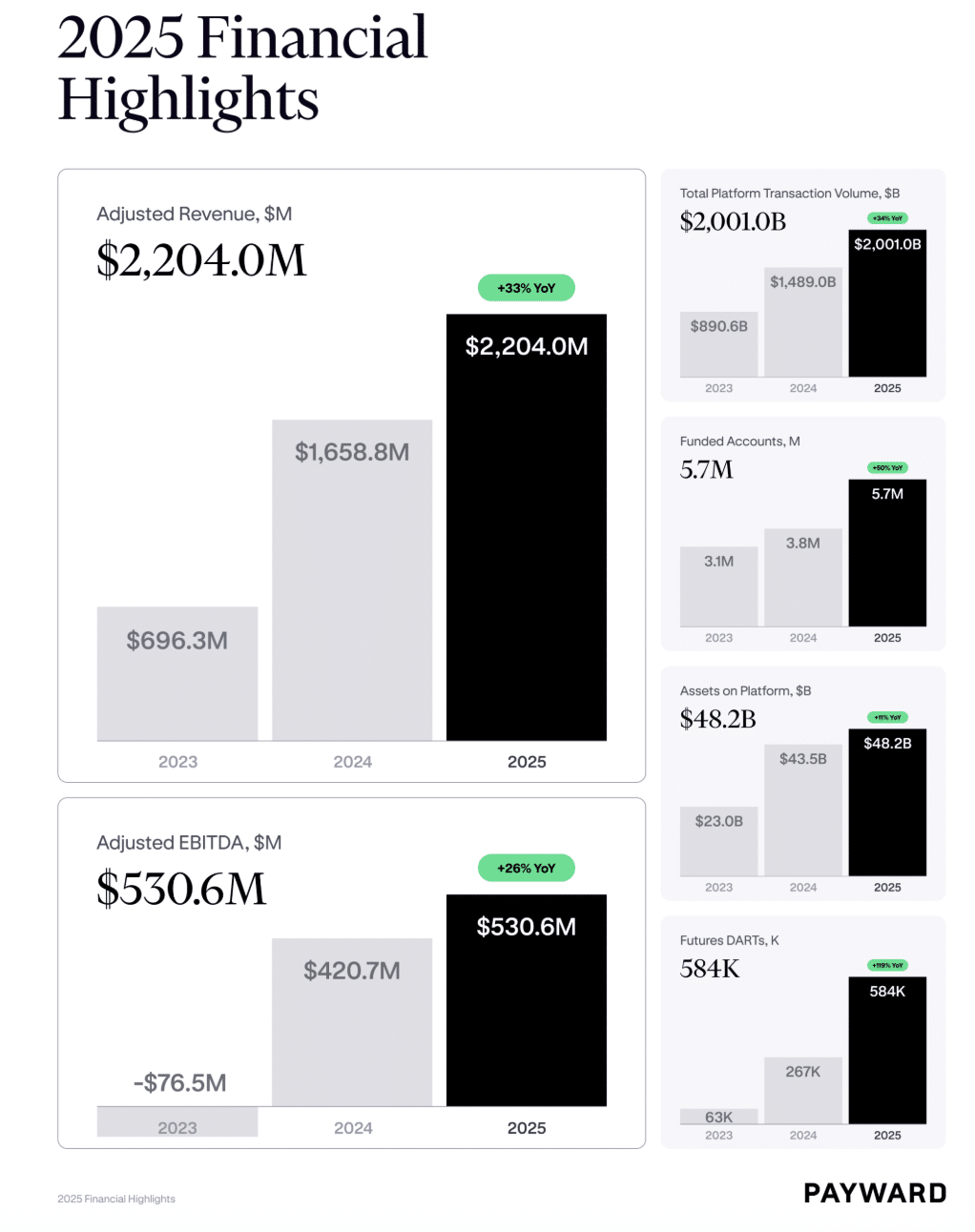

In 2025 Payward’s adjusted revenue reached $2.2bn, representing 33% year-over-year growth, which the firm said was driven by broad-based performance across trading and asset-based businesses. Total platform transaction volume reached $2 trillion, up 34% year-over-year.

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

The exercise will run from the second half of 2026 to the first half of 2027.

-

The closing auction is a critical market infrastructure element in all major asset classes.

-

Robinhood Chain unlocks possibilities beyond what traditional finance can offer.

-

The regulator has the regime to include simpler capital requirements for stablecoin firms and trading rules.

-

Bitcoin depositary receipts can be integrated into existing institutional workflows.