02.19.2021

Nasdaq Sustainable Bond Network Aims For Global Coverage

02.19.2021

The Nasdaq Sustainable Bond Network is aiming to increase coverage in the US and Asia as demand for data grows from investors with environmental, social and governance strategies.

The exchange operator launched the Nasdaq Sustainable Bond Network in December 2019. The network is a global, publicly available web-based platform which aims to improve transparency in the market for green, social and sustainability bonds. Issuers of sustainable bonds can voluntarily publish data on their bonds in a standardized framework allowing investors to find information in a central location and allowing investors to compare instruments.

Anne-Charlotte Eliasson, Nasdaq

Ann-Charlotte Eliasson, head of European fixed income listings at Nasdaq, told Markets Media: “The Nasdaq Sustainable Bond Network is aiming for global data coverage, including the US and Asia Pacific, through both collaborations and outreach for issuers. We have a strong partner in Asia with SGX.”

Since launching more than 300 issuers, including development banks, European banks as well as state and government agency issuers have joined the network. A partnership between Nasdaq and the Singapore Exchange to expand the platform into Asia-Pacific is due to launch this year.

Eliasson said: “We are launching an investor portal for the Nasdaq Sustainable Network in the spring.”

Investors will be able to upload their portfolios and also search for bonds with specific sustainability criteria, such as under the 167 UN Sustainable Development Goals.

“We are also in dialogue with our advisory board on growing the Nasdaq Sustainable Bond Network as collecting the data is just the first step,” added Eliasson. “We want to make reporting much easier and help issuers and investors help find each other.”

Issuance

Nasdaq said in a statement that total listed volumes on the Sustainable Debt Market increased 53% last year from 2019. Last year the Swedish Government’s $2bn issue was the first listing of a Nordic sovereign green bond, and Tornator was the first corporate green bond from Finland on the exchange. Nasdaq Helsinki also had its first listing of a social bond, issued by Finland’s Municipality Finance.

In 2020, @Nasdaq saw another strong year for its European Debt Market.

A high number of issuers have tapped the debt capital markets to raise funds to support #COVID19 pandemic mitigation efforts.

Learn more: https://t.co/vQibgmJFy8 pic.twitter.com/aRQIwuC0oK

— Nasdaq (@Nasdaq) February 5, 2021

“Data from the Nasdaq Sustainable Bond Network shows that the issuers listing bonds at Nasdaq’s Sustainable Debt Market in Europe together saved 9.5 million metric tons of greenhouse gas equivalents through the investments financed by their sustainable bonds, as reported by the issuers in their latest annual reports,” added the exchange. “The emissions saved are equivalent to the greenhouse gas emissions for the population of Stockholm.”

Eliasson continued that Covid-19 has led to the issuance of more social bonds as authorities combat the impact of the pandemic through programs such as job retention schemes and investing in healthcare.

“We follow the ICMA principles with the exception that social bonds need a second opinion or independent third party review,” added Eliasson. “It is important that investors can follow up on the impact of social bonds.”

The International Capital Market Association updated the social bond principles last year to include COVID-19 bond guidance.

She added that green bond issuance has been made more difficult due to delays to the proposed European Union taxonomy as there is more caution on what qualifies as green. Last month the European Commission was due to publish the implementing rules on the region’s sustainable finance taxonomy, which included a list of green activities, but this has been put off due to the number of comments received during the consultation period.

“This year we expect to see transition and sustainability-linked bonds,” said Eliasson.

.@LSEplc will this week become the first exchange to launch a dedicated Transition Bond Segment. Part of our #SBM, it will display debt instruments from issuers with a corporate strategy or transition framework aligned to the Paris Agreement https://t.co/sdkGIx3kpd pic.twitter.com/0l3ZidWnZA

— LSEG – (London Stock Exchange Group) (@LSEGplc) February 16, 2021

London Stock Exchange this week said it will launch a dedicated transition bond segment. Green bonds exclude many industries and companies that do not have sufficient green assets.

Transition bonds allow these carbon-intensive sectors, such as oil and gas or transportation, to use the proceeds to help reduce their carbon footprint.

There is no agreed definition of transition but LSE said the segment will display debt instruments from issuers who have a corporate strategy or transition framework that is aligned to the Paris Agreement, including approved targets to achieve net zero, and discloses, manages and addresses climate-related risks in line with global standards such as the Climate Transition Finance Handbook, the CBI Transition Certification Framework and the Transition Pathway Initiative.

Forecast

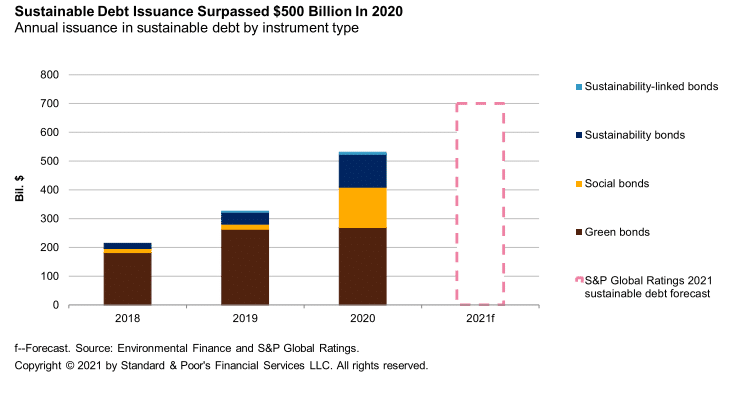

S&P Global Ratings said in report that it expects issuance of sustainable debt, including green, social, sustainability, and sustainability-linked bonds, to surpass $700bn this year. This will take cumulative issuance to more than the $2 trillion milestone, from $1.3 trillion at the end of last year.

Sustainable debt issuance exceeded $530bn last year according to the ratings agency, up 63% from 2019. Social bonds were the fastest growing segment of the market, growing eightfold in 2020, while green bond volume reached a record $270bn.

Source: S&P Ratings.

S&P estimated that green-labeled bond issuance could exceed $400bn this year.

“We also believe the green use-of-proceeds model will expand to include transition finance, aiding high-carbon-emitting sectors to finance their transition into net-zero emissions business activities,” added S&P. “We expect to see rapid growth of sustainability bonds, which target both social and environmental objectives, as well as greater interest in sustainability-linked instruments.”

The ratings agency continued that regulations and principles have played a key role in advancing the best practices for use of proceeds and impact reporting and it expects the EU Taxonomy and other similar frameworks to promote the growth of the sustainable debt market .

“While significant progress surrounding transparency and reporting has been made, there is room for improvement, particularly with the newer categories of bonds (i.e., social and transition), for which impact assessment is less standardized,” added S&P. “In our opinion, robust disclosure practices, ongoing standardization, and the use of qualified third-party reviews could mitigate some of these risks.”

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

As Technology Evolves, Asset Managers Adapt and Innovate

Citi Changes Organizational Structure

SEC Charges Virtu for Disclosures Relating to Information Barriers

ICE Futures Singapore Partners with CoinDesk Indices

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

Marlborough says bond markets will be closely watching employment data this week.

-

This is the first native digital bond by a Germany-based issuer in Switzerland.

-

Addition of India further expands MarketAxess’ emerging markets offering.

-

This reduces the pressure asset managers face on pricing days.

-

Net proceeds may be used to finance the acquisition of Aquis Exchange.