05.19.2026

Michael Selig, chairman of the Commodity Futures Trading Commission, is optimistic that that U.S will pass the Clarity Act to provide a market structure framework for digital weeks in the coming weeks.

Selig spoke at City Week 2026, hosted by City & Financial Global, in London on 19 May 2026. He highlighted that the proposed bill has been approved by the Senate banking committee after being passed out of the Senate agricultural committee several months ago.

“We’re at the point where we are expecting a full vote on the floor in the Senate in the coming weeks, and once it passes the Senate we are optimistic ihat it will pass the House,” he added. “A similar version of the bill passed the House a year ago, so that’s something that we’re looking to get on the President’s desk in the next month or two.”

Once the Clarity Act has been enacted into law, the CFTC and its fellow U.S regulator, the Securities and Exchange Commission, will be “very busy” implementing the statute, according to Selig. He said: “The law is going to involve the registration of new exchanges, called digital commodity exchanges, with the CFTC as well as a wide range of different intermediaries.”

Selig expects there will be custodians, centralized exchanges and different types of advisors in the digital asset ecosystem similar to the existing securities and commodity derivatives markets. However, he also predicted the development of new software programs and self-custodial products.

As a result, the CFTC is evaluating how to approach new technologies where there is not necessarily an administrator or person in the middle of transactions. Selig said the regulator is reviewing the activity itself and people engaging in transactions onchain, as opposed to the person who designs the contracts.

He used the analogy of driverless cars, where regulators do not prosecute Tesla for manufacturing the car that somebody uses to rob a bank.

“We’re certainly going to prosecute and bring civil penalties against the robbers, but we’re not necessarily targeting software developers who are building some of these new technologies,” said Selig. “We think it’s very important to have a place for self-custodial wallets and for onchain applications, and the software developers of those products should not be regulated like an intermediary or an exchange.”

In addition, the CFTC is “excited” to facilitate onchain derivatives and onchain margin trading for crypto assets. The regulator is working to accommodate the use of tokenized collateral by brokers and with clearinghouses to facilitate the movement of tokenized assets, which could include stablecoins, tokenized real world assets, like gold, or native assets like bitcoin or ether.

“That’s a big piece of work and we’re excited to start to see our exchanges utilize crypto as collateral and transact with customers using tokens,” added Selig. “We’re already seeing it in the prediction market space and some of our crypto derivatives platforms.”

The U.S administration passed the Genius Act last year to establish a new regime for payment stablecoins and the CFTC has set standards for their margin and capital treatment, which Selig said is facilitating broader use of stablecoins within derivatives markets.

“We are working closely with prudential regulators to make sure we have the right regime in place for banks and trust companies, so we’re very excited about it,” said Selig.

He predicted that stablecoins are going to be a “massive” use case for blockchain rails, and have a lot of interest from traditional financial institutions in the U.S. who want to transact on 24/7, 365 days a year. In addition, Selig said the CFTC is going to create a space for prediction markets in the U.S and set the gold standard for their regulation.

“We’re just exploring the surface of what’s possible with blockchain technology,” said Selig. “AI can have autonomously transacting program agents to do your bidding on a blockchain trade and that’s really interesting. It also creates a lot of risk, so we’re assessing that as regulators, but we’re excited to be at the kind of the new frontier finance.”

Bank of England

Sarah Breeden, deputy governor for financial stability at the Bank of England, also spoke about regulation of tokenized finance at City Week 2026 on 19 May 2026. She said in a speech that no single firm can build that ecosystem alone, so she is thrilled that Chris Woolard was appointed as the U.K. government’s wholesale digital markets in April this year. Woolard is a partner at EY and former interim chief executive of the Financial Conduct Authority.

Breeden argued that tokenization has real potential to improve retail payments and wholesale finance as shared ledgers, updated near-simultaneously across all parties to a transaction, could make payments and settlement faster and cheaper, with fewer intermediaries, less operational risk, lower cost, and shorter settlement windows. Smart contracts allow greater customisation, conditionality and automation and atomic swaps can extend delivery-versus-payment (DvP) and payment-versus-payment (PvP) settlement to allow a broader range of assets to be monetised easily, including intraday.

“A mid-sized corporate treasury could invest excess cash overnight in tokenized securities for a fraction of a day, then sell them with near real-time settlement the next morning, widening cash management options,” she said. “ Global corporates hedging in derivatives markets could meet margin calls more easily using tokenized collateral, with 24/7 cross-currency transfers to the subsidiary receiving the call, settled in near real time.”

With the U.K. Treasury, the Bank will set out the conclusions of its design phase this year on a retail central bank digital currency, or digital pound. It will publish draft rules for systemic stablecoins next month and finalise them by year-end, in line with the U.S. timeline.

“One option, also set out in the consultation, would be temporary guardrails on the total amount of a coin that could be issued,” Breeden added. “Reviewed regularly, that approach could achieve the same aim at lower cost to the sector and allow a wider range of high-value payment use cases, including for corporates.”

Banking groups can issue stablecoins from a non-deposit-taking, insolvency-remote group entity, similar to requirements in the U.S. These stablecoins should carry branding distinct from the group’s deposits,to reduce confusion, and the risk of contagion to bank deposits, as stablecoins will not be covered by deposit insurance.

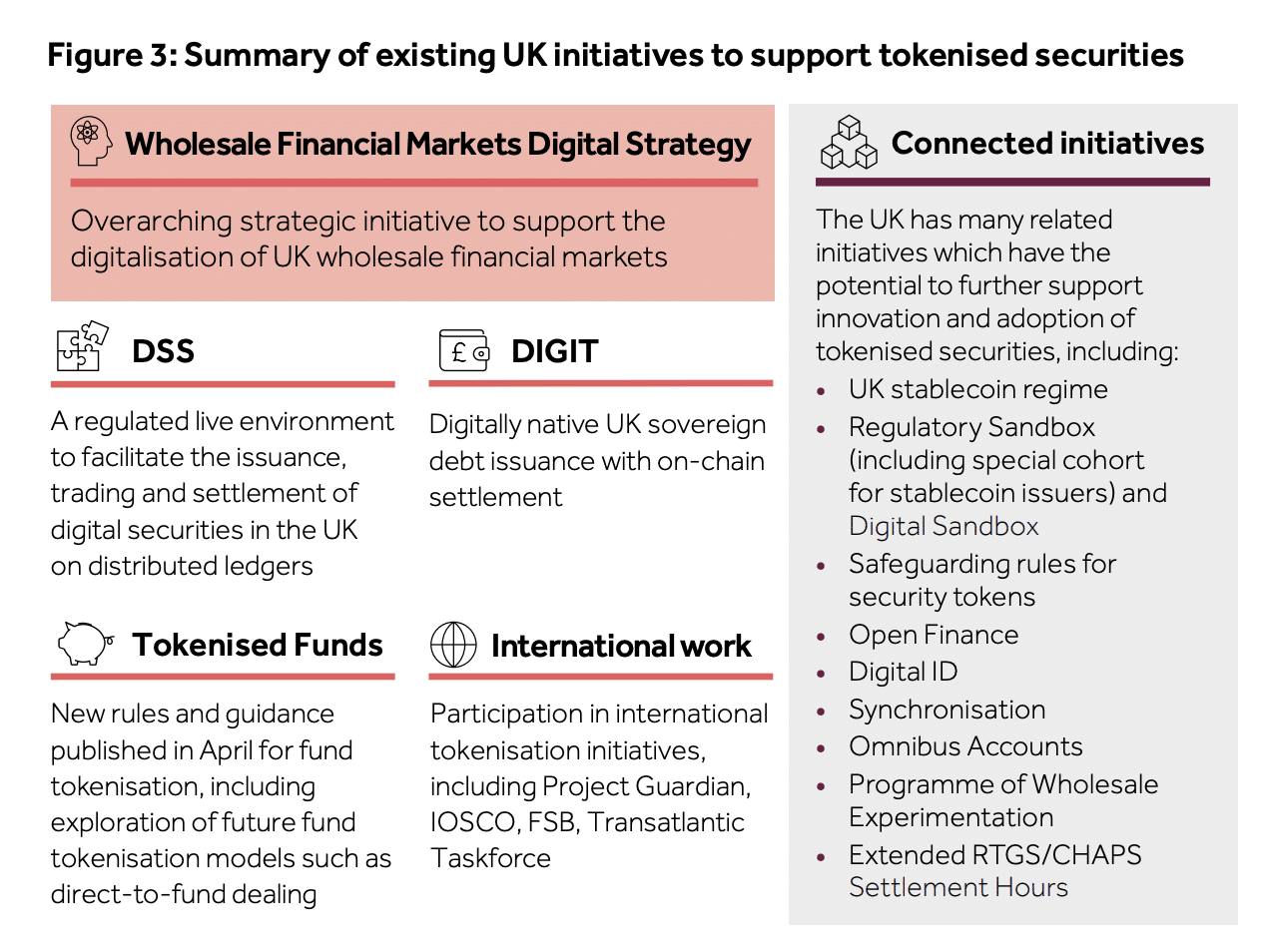

In wholesale payments and digital markets, the Bank is enabling live trading venues and settlement systems for the supply of tokenized assets, including for the U.K. government’s pilot issuance of a digital gilt instrument (DIGIT).

“We are ensuring no unwarranted frictions to demand for tokenized assets through their prudential treatment and collateral eligibility,” she said. “We are providing infrastructure for the cash leg to settle in central bank money, in our modernisation of the Bank’s own payments infrastructure.”

The Bank is upgrading its internal systems in 2027 to connect directly to tokenized asset ledgers. In order to enable tokenized wholesale transactions to settle in central bank money the Bank is developing new functionality in its newly upgraded Real-Time Gross Settlement (RTGS) infrastructure, RT2.

Breeden said she often describes RT2 as a “parked Ferrari” as it makes it possible to settle tokenized transactions directly in sterling central bank money. The Bank has confirmed its commitment to delivering its synchronisation service in 2028. This will enable the conditional movement of a wider set of assets and transaction types, including on DLT, against movements in central bank money held in RTGS accounts. A report later this month will showcase the prototype and set out next steps.

“We are testing this with 18 firms in our Synchronisation Lab, which went live earlier this month, across use cases including settlement of house purchases, tokenized securities and FX,” added Breeden. “So that Ferrari is out on a test drive now, and will be racing round the City very soon.”

A consultation has also been published on extending RTGS’s settlement hours towards near-24/7 operation. The Bank is on track next year to extend RTGS settlement hours from 12 to 16½ hours each working day, according to Breeden.

“We are now seeking feedback on moving after that to Sunday and some bank-holiday settlement, and to 22 hours a day, by early next decade,” she added. “We are also seeking views on going further in the longer term, to 22×7 or near-continuous 23.5×7 operation.”

Bank-FCA Digital Securities Sandbox

Breeden argued that the central part of the work on tokenized assets is the Bank-FCA Digital Securities Sandbox (DSS), which launched in 2024 and runs until January 2029 . This lets firms operate under a modified legislative and regulatory framework for trading and settlement, to remove legal barriers that might otherwise hinder the use of new technologies. The DSS also includes issuance limits for key digital securities markets, set high enough to allow meaningful activity while safeguarding financial stability.establish live U.K

Later this year 16 firms are preparing to launch from the sandbox with a route to permanent operation, including Euroclear, HSBC and the London Stock Exchange Group, according to Breeden,

“We think the DSS offers greater certainty, competition and innovation than narrower alternatives that grant targeted, temporary legal relief to individual firms for specific initiatives and support a broader range of business models and use cases,” she said. “It also gives firms and authorities a way to learn how best to enable the responsible adoption of distributed ledger technology (DLT) in financial markets and embed those lessons in permanent operations and regulation.”

In the Bank’s own lending operations, it will also consider whether tokenized assets should be eligible as collateral in the Sterling Monetary Framework (SMF), which Breeden said would backstop the ability to monetise them in private markets.

The Bank of England prudentially regulates and supervises financial services firms through the Prudential Regulation Authority. The PRA has clarified that the prudential treatment of UK banks’ exposures to tokenized assets will be the same as for their non-tokenized equivalents where the legal rights are identical and the underlying risks are comparable.

Breeden said: “For collateral eligible at central counterparties, our aim is likewise to support eligibility of tokenised versions of assets already accepted as collateral. We will engage with industry on the detail through a discussion paper later this year.”

NEWSLETTER SIGN UP

And receive exclusive articles on securities markets

🏆 The 2026 Global Markets Choice Awards are here! 🌍 Nominations are officially OPEN for the celebration of excellence in global capital markets trading & technology. Nominate below:

https://www.jotform.com/form/260086385121150

Delaware Life Insurance Company is becoming the first insurance carrier to offer an index that contains cryptocurrency, adding the BlackRock U.S. Equity Bitcoin Balanced Risk 12% Index to its fixed index annuity (FIA) portfolio.

As the digital assets industry pushes toward

Franklin Templeton is expanding its tokenized fund suite, signaling growing institutional demand for blockchain-based fund infrastructure and regulated investment products moving onchain. Read the full article below:

$50 billion in active ETF inflows helped fuel a record year for @BlackRock 's iShares business, as investors continue to lean into active strategies.

Shanny Basar

Senior writer

A Senior Writer at Markets Media who became a financial journalist in 2000 after working in banking for over a decade....

More about this authorRelated articles

-

Trusted market infrastructure will serve as a critical foundation for institutional adoption.

-

The market maker aims to be the 24/7 liquidity provider of choice across traditional & digital assets.

-

The pilot shows how institutional access to digital asset credit intermediation could evolve.

-

The lines between traditional finance and digital assets are dissolving.

-

This is one of the first high yield bond offerings available onchain.